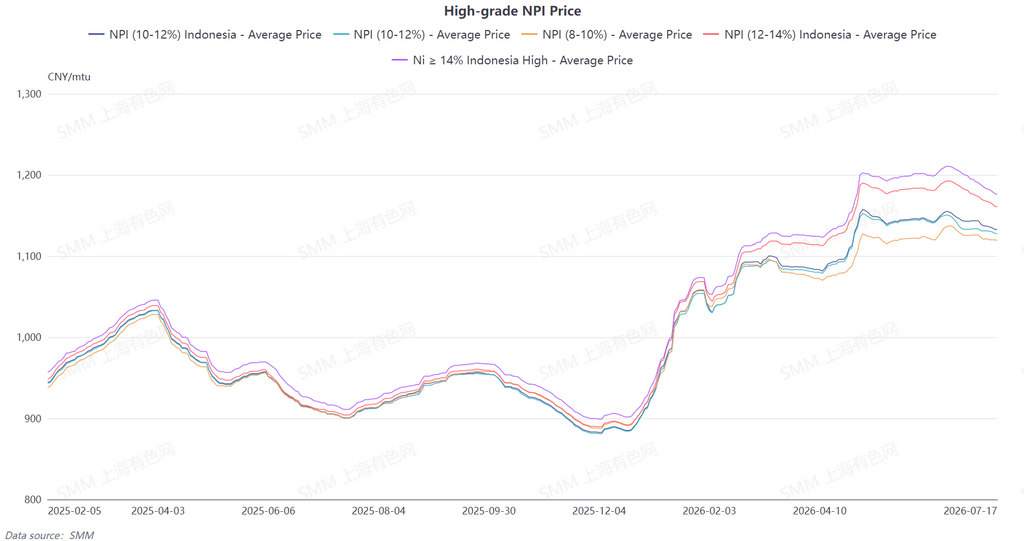

SMM 10-12% high-grade NPI average price dropped WoW by 3.1 yuan/nickel unit to 1,129.4 yuan/nickel unit (ex-factory, tax included), and the average Indonesian NPI FOB index price dropped WoW by $0.47/nickel unit to record $145.76/nickel unit. Throughout the week, the high-grade NPI spot market remained in a state of deep supply-demand struggle, with bullish and bearish expectations diverging further. Overall trading activity was sluggish, and batch fixed-price purchases by steel mills were absent.

The demand side was continuously weighed down by the traditional off-season for stainless steel in July. Weakening end-user product prices directly pressured NPI prices. Meanwhile, multiple cuts in steel scrap prices revived its substitution advantage as a furnace charge, diverting rigid demand for NPI purchases. Downstream players broadly held a bearish outlook, continuously lowering their psychological purchase prices. Most enterprises opted to consume in-house inventories and held off on active buying, with market acceptance of high-priced cargoes extremely low. The supply side exhibited structural divergence, with spot circulating cargoes tightening temporarily in the short term. Coupled with smelting cost support, most suppliers showed strong willingness to hold prices firm, while some merchants adjusted their quotations in line with futures fluctuations.

Meanwhile, most enterprises quoted based on an average price plus premium model, rarely offering fixed prices. Many market participants directly suspended offering quotes amid unclear market trends, resulting in a contraction in effective selling interests. With the recent typhoon impact fading, concentrated arrivals at ports slightly eased the tight spot supply, leading to an increase in low-price inquiries and a slight downward shift in the price center. However, a recovery in futures and the fact that overall production had yet to recover significantly provided bottom support for spot prices, limiting deep declines. Overall, this week saw bullish and bearish factors in check, with the psychological price spread between upstream and downstream remaining hard to narrow. The market continued to exhibit a range-bound, stagnant consolidation pattern with sluggish trading.

It is also worth noting that, according to market sources, the commissioning pace of aluminum smelting in Indonesia may fall short of expectations, which could ease power competition for high-grade NPI in H2 2026.

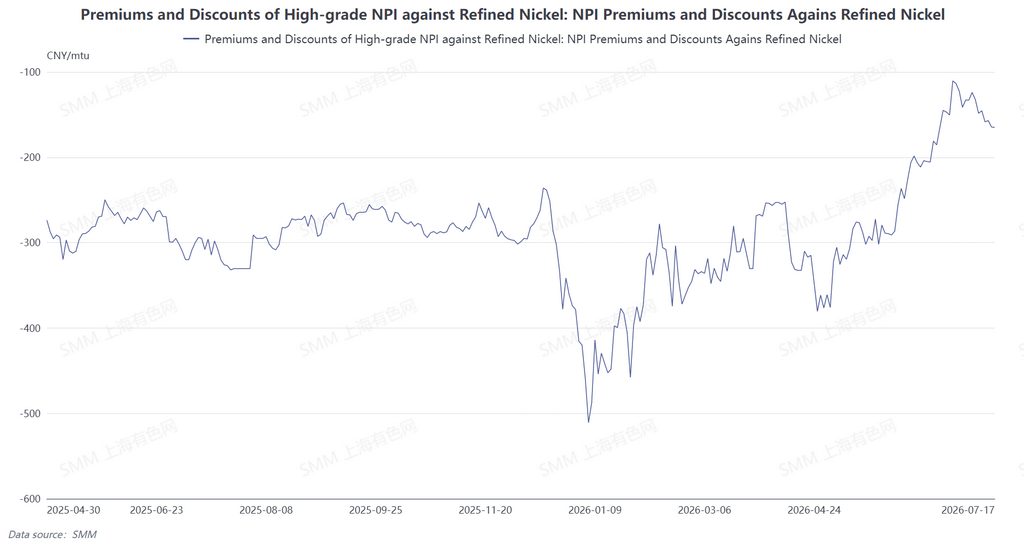

From the perspective of converting NPI to high-grade nickel matte, the discount of high-grade NPI against refined nickel widened slightly this week. The divergence in the price spread was driven by the opposite movements of the two prices: the price center of refined nickel rebounded somewhat this week, while high-grade NPI continued to be weighed down by the traditional off-season for stainless steel, with weak downstream demand and persistent push for lower prices from steel mills keeping its spot price on a downward trend. The spread between the two widened further, with the average discount of high-grade NPI against refined nickel expanding slightly to 158.1 yuan per nickel unit. Although the current discount on high-grade NPI has widened, the price spread is not yet wide enough to cover the costs required for converting NPI to high-grade nickel matte, meaning it is not economically viable to drive a large-scale switch of smelting lines to produce high-grade nickel matte. It is expected that no conversion of high-grade NPI driven by the spread will take place in the short term.

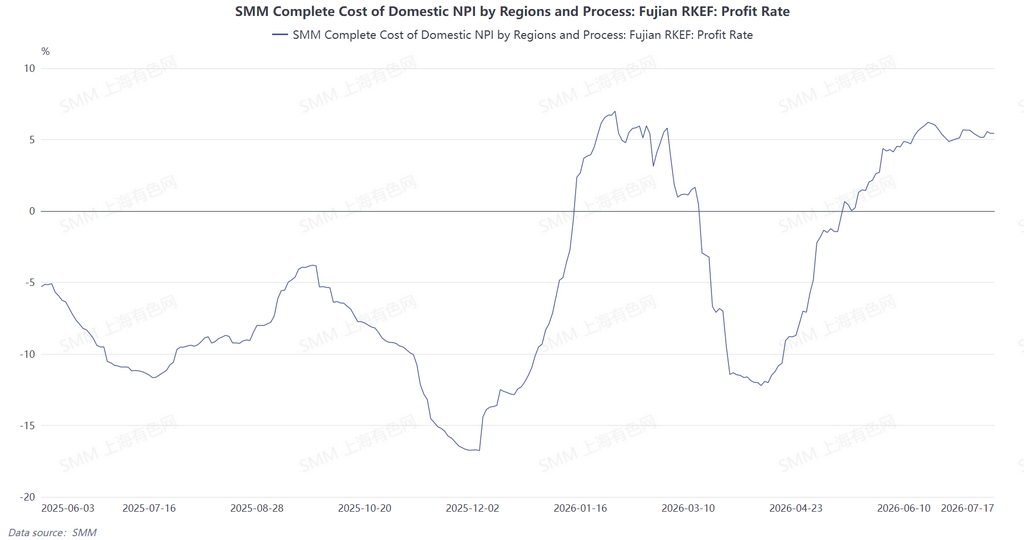

This week, domestic nickel ore purchase prices for smelters remained largely stable, with prices of auxiliary materials such as coking coal and coke only fluctuating slightly, and overall smelting costs were broadly flat. However, under continued pressure from the stainless steel off-season, the market price of high-grade NPI drifted lower this week. Amid largely unchanged production costs, domestic smelters saw their unit profit margins shrink accordingly. In Indonesia, local nickel ore prices pulled back this week, easing cost pressure on the raw material side. The decline in raw material costs led to some recovery in local NPI smelting margins. If ore prices remain in the doldrums going forward, cost pressure in Indonesia may ease further.