June Price Review:

The monthly average spot price of grain-oriented silicon steel continued its earlier rebound in June, with the price center rising further. Despite relatively high supply pressure, the earlier price bottom recovery trend persisted, as the monthly average spot price rose steadily, reflecting good market expectations for price recovery. However, the oversupply pattern suppressed upside room, and the price rise pace was relatively mild, without a significant surge.

Fundamental Analysis:

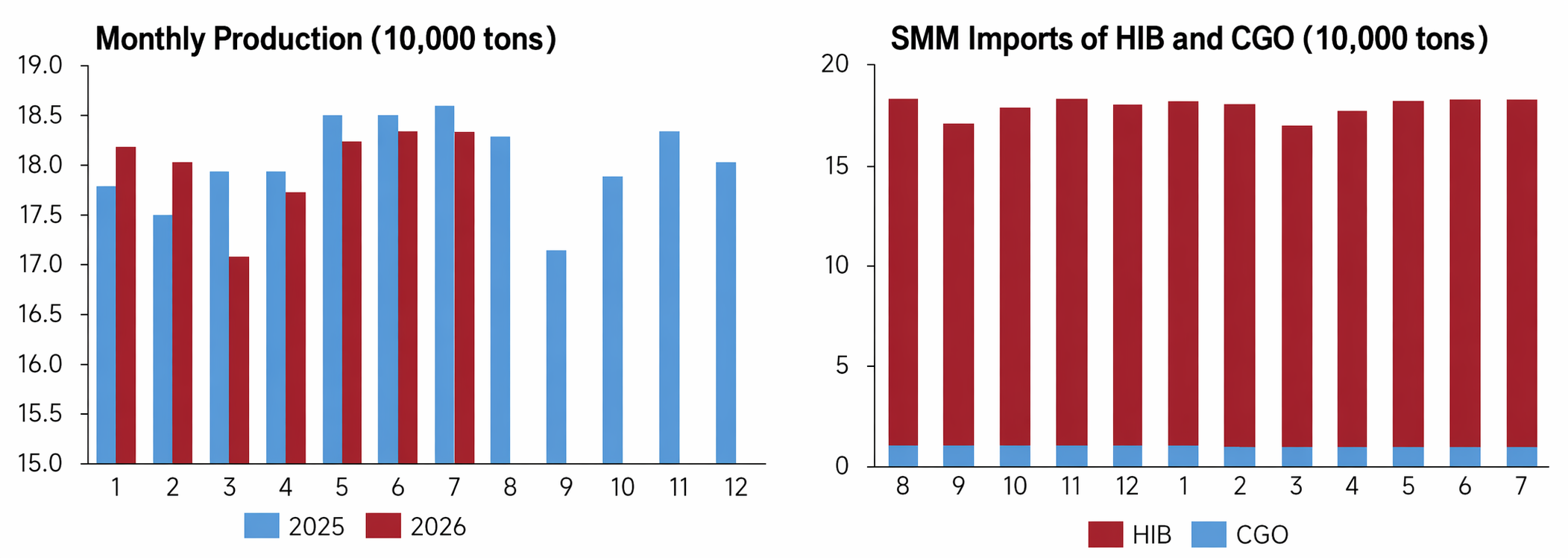

In July, grain-oriented silicon steel production stayed high. By product type, HIB and CGO output remained stable. High-grade HIB still accounted for the vast majority of production, while CGO output remained in a small stable range, with no significant adjustments in the product mix. Compared with historical production schedules, the July 2026 schedule remained at a high level, with overall supply release being stable, and total supply of grain-oriented silicon steel staying relatively sufficient. The persistently high output was also one of the core factors capping the upside room for this round of grain-oriented silicon steel price rises and maintaining a loose supply-demand balance.

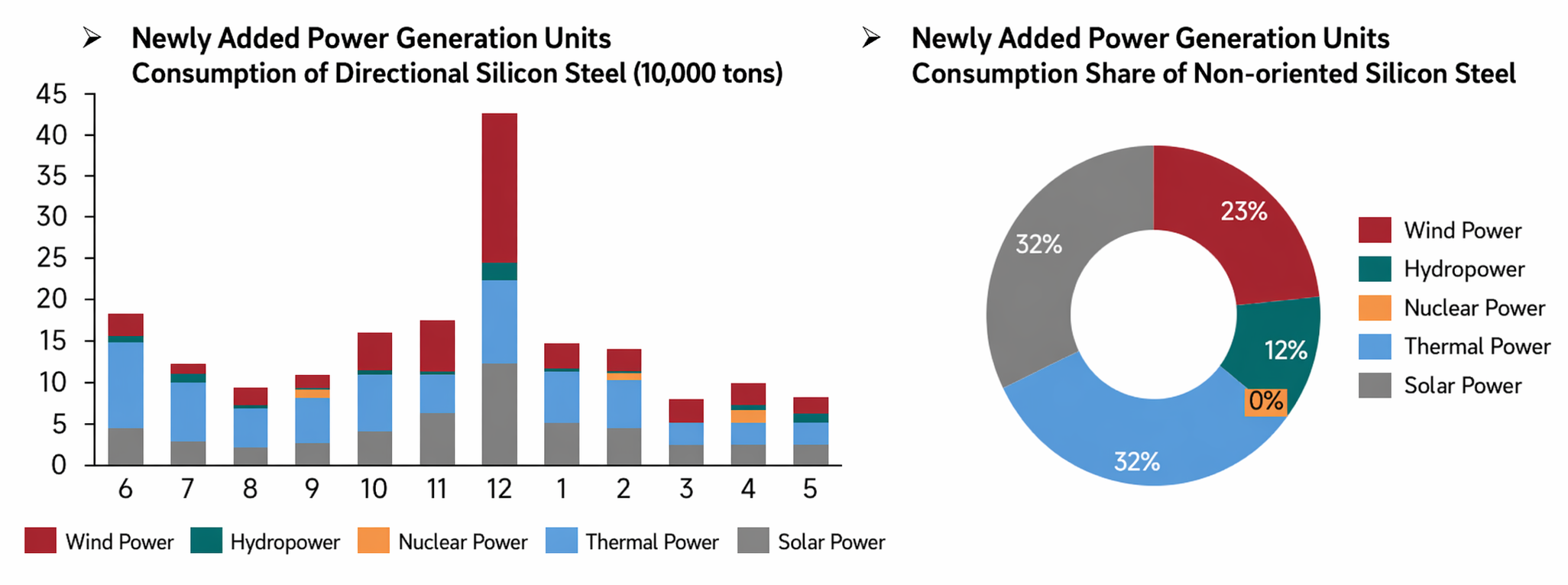

In May, the consumption of grain-oriented silicon steel driven by new power grid installations was at a relatively low level for the year. By structure, thermal power and solar energy remained the main consumption sources, with wind power and hydropower providing supplementary demand, while nuclear power's share stayed low. Compared with the consumption structure of non-oriented silicon steel, thermal and solar power together accounted for 60%, clearly defining the demand structure on the power supply side. In May, the pace of new end-user installations slowed down, transformer company order growth was limited, and direct demand for grain-oriented silicon steel was released slowly. Coupled with continuous high production at steel mills, supply-side pressure was difficult to digest, which suppressed silicon steel prices. In the short term, it is hard to rely on power grid installations to provide a strong demand boost.

July Price Outlook:

Looking ahead to July 2026, supply side, China's grain-oriented silicon steel supply is expected to remain basically stable. Production lines at major domestic steel mills are operating stably, with no centralized maintenance plans, and the overall production load is maintaining stability. Meanwhile, mainstream steel mills like Baowu have raised the base price of grain-oriented silicon steel by 300 yuan/mt in their July product pricing policy. Combined with production profits remaining within a reasonable range, overall production enthusiasm is good, and high-grade resources are being steadily released. Demand side, market positives are continuing to provide support, and overall demand performance is robust. China's "15th Five-Year Plan" ultra-high voltage projects are being intensively started, construction pace is steadily advancing, and demand for transformers supporting new energy grid connection is strong. Additionally, home appliance and NEV energy efficiency upgrades are gradually being implemented, demand for high-efficiency motor retrofits is staying high, and overseas power grid upgrade projects are advancing continuously, with stable procurement demand for high-grade grain-oriented silicon steel. However, India has initiated anti-dumping against China's grain-oriented silicon steel, which may cause some resources to flow back to the domestic market, capping price increases. Cost side, driven by expectations of continued shrinking steel mill profits and normalized local environmental protection-driven production restrictions, hot metal output is expected to decline further; however, with the off-season impact widening, the average price of hot-rolled coil in July is expected to continue to decline MoM from June, with the decline narrowing. Overall, SMM expects the grain-oriented silicon steel price in July 2026 to show a consolidation pattern.

Data Source Statement:

(The data in this report, other than publicly available information, are derived from public information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, National Bureau of Statistics (NBS) data, customs import and export data, and various data released by trade associations and institutions), market communication, and SMM's internal database model. They are obtained through comprehensive analysis and reasonable inference by the research team, and are for reference only, not constituting any decision-making advice.

SMM reserves the final interpretation rights of this statement and the right to adjust and modify the content of this statement according to actual circumstances.

![[SMM Analysis] Futures recover, driving phased transactions and limited arrivals, causing stainless steel inventory to stop rising and pull back.](https://imgqn.smm.cn/usercenter/rUQIB20251217171723.jpeg)