Price Review for June:

In June, the monthly average price of non-oriented silicon steel trended downward, probing the bottom. Supply-demand side, the market shifted from a slight balance to a mild undersupply, with fundamentals improving marginally. The oversupply that had been weighing on prices gradually eased, providing support for prices. Spot prices performed stronger than expected, edging down only slightly. As a transitional month between the off-season and peak season, June saw the supply-demand pattern improve.

Fundamentals Analysis:

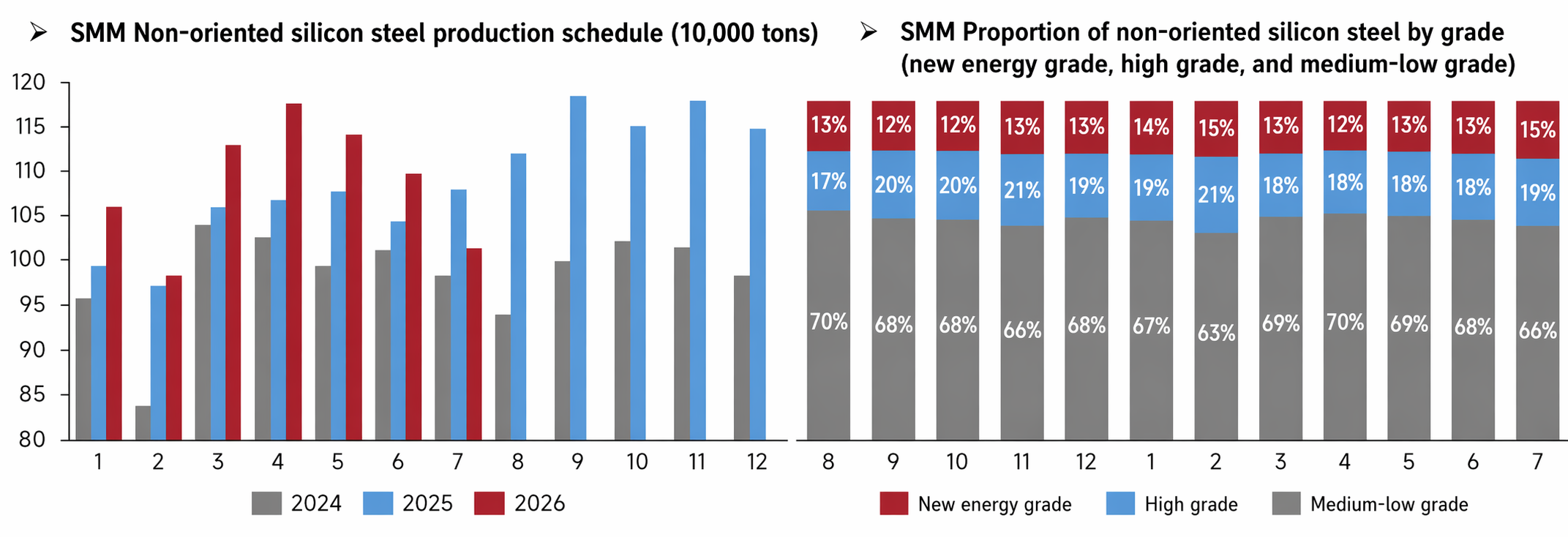

The July production schedule for domestic non-oriented silicon steel is planned to decline further. Compared with the same period in previous years, the July 2026 schedule was lower than that of July 2025. In terms of grade structure, the proportion of NEV grades in the July schedule is expected to rebound to 15%, high grades at 19%, and low and mid-end grades pull back to 66%. Steel mills continue to adjust their product mix, leading to corresponding reductions in low-end conventional grades. Overall scheduled production volume continues to shrink, but supply-side pressure persists. Production levels for NEV and high-grade materials are maintained, while low and mid-end grades are significantly reduced, optimizing the supply structure to some extent and supporting price resilience.

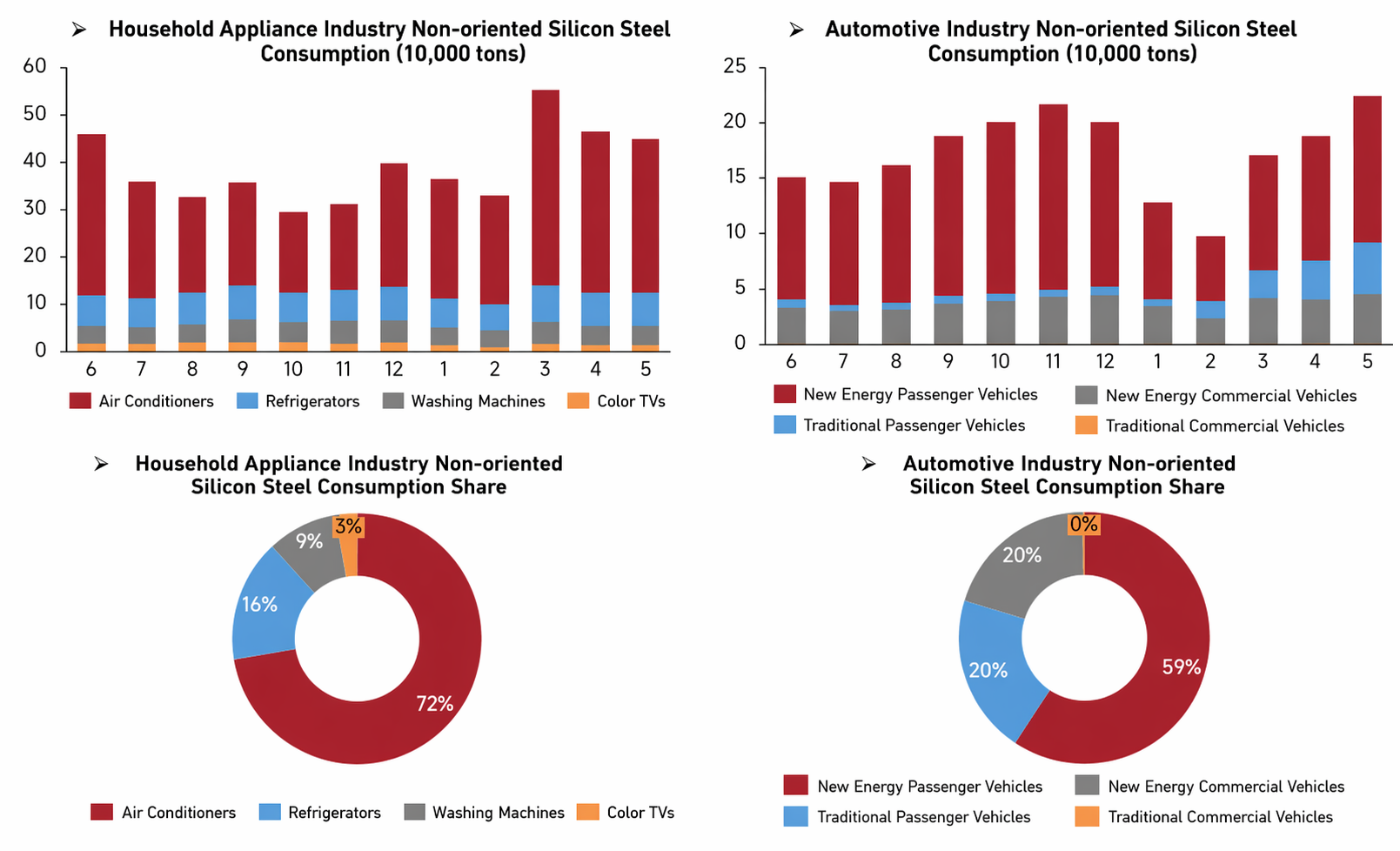

Downstream demand for non-oriented silicon steel in May showed structural divergence. Total silicon steel consumption in the home appliance sector edged down MoM, with air conditioners remaining the core demand driver. The automobile sector demand was strong, with silicon steel consumption climbing to a high for the period. Within this, passenger NEVs were the biggest support for non-oriented silicon steel demand in the auto sector. Overall, traditional home appliance demand weakened marginally, while NEV demand continued to strengthen, gradually shifting the demand center toward the auto track. This structurally benefited high-grade and NEV-grade non-oriented silicon steel.

July Price Outlook:

Looking ahead to July 2026, on the supply side, China's non-oriented silicon steel production schedule is planned to decline further, primarily in low and mid-end grades. On one hand, the off-season impact is becoming more pronounced: downstream demand is weak, purchasing enthusiasm has fallen, weighing on production willingness. On the other hand, leading producers such as Baowu and Shougang kept their July base prices unchanged, prioritizing price stability. However, market sentiment is bearish and prices are more likely to fall than rise. Most producers are operating at a loss and implementing voluntary production cuts. On the demand side, in the home appliance industry, producers slowed their production pace, with orders declining MoM. The "618" shopping festival did not significantly stimulate orders. Affected by low demand, high inventory, and high costs, some enterprises lowered their production schedules ahead of time. Additionally, new energy efficiency standards for certain home appliances were introduced, limiting production due to product iteration. In the automobile industry, automakers mostly maintained normal production pace, with some increasing output this month to meet mid-year targets. However, sales pressure remained due to moderate effects of the "618" promotions and policy support. Breaking it down, NEVs remained the main sales driver this month, while orders for internal combustion engine vehicles did not improve significantly. Exports were mainly directed to Russia, South America, and Southeast Asia. Total annual export volume for the industry is expected to reach 12 million units. Cost side, with steel mill profits continuing to shrink and local environmental protection-driven production restrictions becoming normalized, hot metal production is expected to decline further. However, as the impact of the off-season expands, the July average hot-rolled coil price is expected to decline further MoM from June, with the decrease narrowing. Overall, SMM expects that mid- and low-grade non-oriented silicon steel prices in July 2026 will drift lower as a whole, with room for price declines.

Data Source Statement:

(All data in this report, other than publicly available information, are based on publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, broker reports, NBS data, customs import and export data, and various data released by major associations and institutions), market communication, and SMM's internal database models. The research team has conducted comprehensive analysis and made reasonable inferences, which are for reference only and do not constitute decision-making advice.

SMM reserves the right of final interpretation of the terms of this statement and the right to adjust and modify the content of the statement in accordance with actual conditions.

![[SMM Steel]](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)

![[SMM Steel]](https://imgqn.smm.cn/usercenter/UrrTG20251217171717.jpg)

![[SMM Analysis] Domestic Demand Underpins Market; Overseas Anti-dumping, July GO Silicon Steel Prices to Consolidate](https://imgqn.smm.cn/usercenter/JdqON20251217171718.png)