This week, iron ore futures consolidated and strengthened. The DCE most-traded contract I2609 closed at 744.5 yuan/mt on Monday, and from Tuesday drifted higher, breaking through the 760 yuan/mt level. The core driver of this round of price strength came more from news-driven disruptions, while fundamental support was relatively limited. On the supply side, the strike at BHP's Port Hedland proceeded as planned, with port shipments suspended for about 8 hours, which is expected to reduce Australia's shipments this week by about 2 million mt. Meanwhile, long-term contract negotiations remained unresolved, SSF port spot cargo pick-up was restricted, and the market circulation of low-grade ore contracted notably, intermittently intensifying supply tightness expectations for certain products. On the demand side, however, performance remained weak. Affected by increased blast furnace maintenance, hot metal output continued to decline, and overall iron ore demand kept weakening, capping the upside room for prices.

Chart: MMI 61% Port Spot Index

Source: SMM

This week, China's iron ore concentrate prices edged up marginally. By region, prices in Tangshan, Qian'an, and Qianxi in Hebei edged up by 1-5 yuan/mt; Chaoyang, Beipiao, and Jianping in western Liaoning raised by 1-5 yuan/mt; east China also saw gains of 1-2 yuan/mt. Iron ore concentrate prices in the Tangshan area of Hebei were relatively stable, with 66% grade dry basis EXW prices including tax at 980-985 yuan/mt; the local area was less affected by rainfall, and production mostly continued as planned. The Chengde area was hit by heavy rainfall, and most mining and beneficiation plants suspended production and shipments—especially in Kuancheng, where the disaster was severe, and overall spot circulation was largely halted. At present, only a few producers in less rain-affected areas could maintain normal operations. Iron ore concentrate supply was also relatively tight in other regions. This week, China's iron ore concentrate prices edged up slightly.

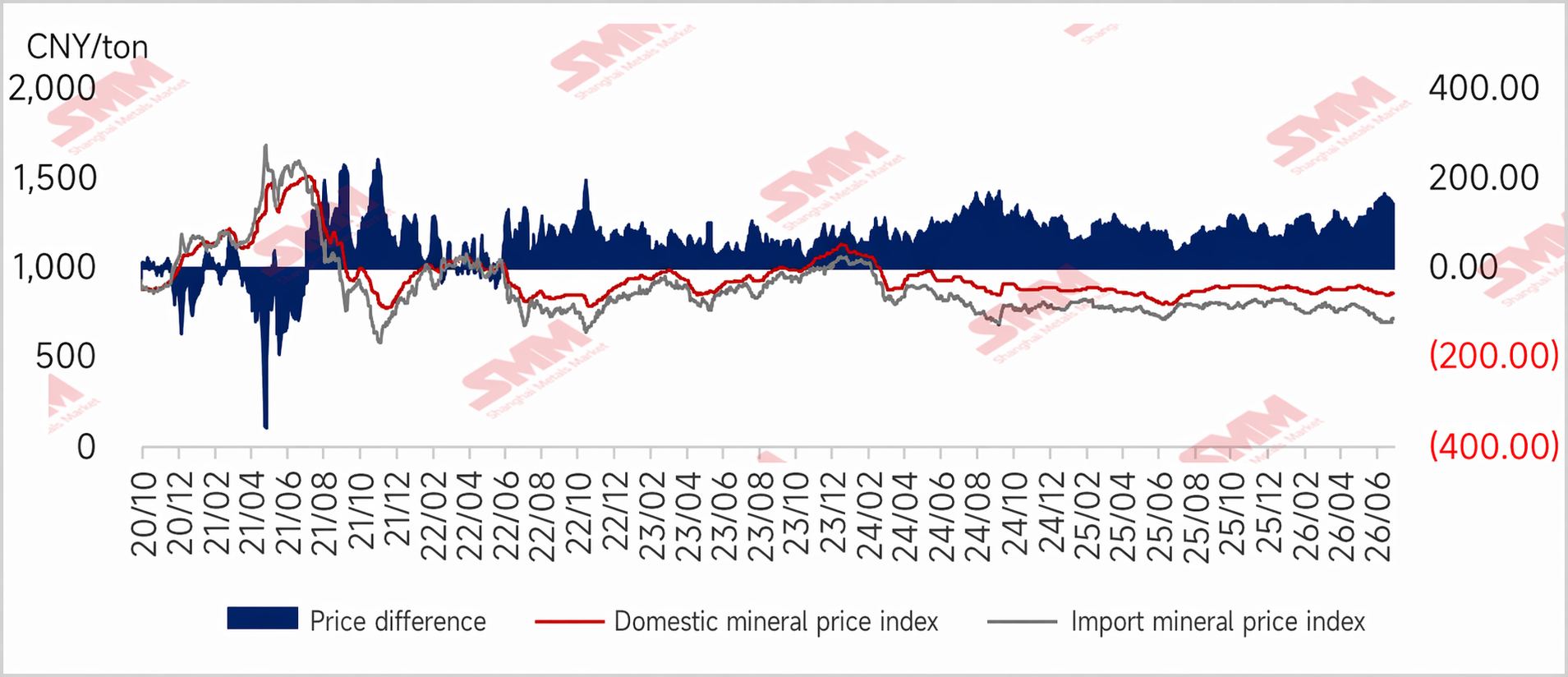

Chart: Imported Ore Prices Strengthened, Domestic-Imported Ore Price Spread Narrowed Slightly

Outlook for Next Week

Imported Ore:

Looking ahead to next week, Tangshan's environmental protection-driven production restrictions have been gradually launched since mid-to-late July, but so far the actual impact on blast furnaces and rolling lines has been relatively limited. If restrictions tighten further next week, some steel mills could arrange temporary blast furnace maintenance, in which case hot metal output would have further room to decline, and iron ore demand may remain under pressure.

However, there is still some support from the supply side and cost side. On the one hand, the SSF port restriction has not eased yet, and low-grade ore circulation remains tight. On the other hand, against the backdrop of the Russia-Ukraine conflict, Ukrainian concentrate supply continues to shrink; coupled with recurring US-Iran geopolitical tensions, these have intermittently lifted the cost floor for iron ore. Overall, the downside room for iron ore prices is limited in the short term, and prices are expected to continue moving sideways within a range. Going forward, close attention should be paid to the enforcement of environmental protection-driven production restrictions, marginal changes in hot metal output, and further disruptions from geopolitical factors to raw material supply.

Domestic Ore: Looking ahead to next week, domestic iron ore concentrate supply is estimated to remain tight. On the demand side, however, hot metal output at local steel mills is expected to decline, and there is a relatively strong desire to push for lower prices for domestic iron ore concentrates. Nevertheless, market sentiment is clearly in favor of sellers at present and local iron ore concentrate prices are expected to remain in the doldrums in the near term.

![[SMM Analysis] Futures recover, driving phased transactions and limited arrivals, causing stainless steel inventory to stop rising and pull back.](https://imgqn.smm.cn/usercenter/rUQIB20251217171723.jpeg)