The latest data from CAAM shows that in H1 2026, China's fuel cell vehicle market exhibited a marked pattern of "moving downwards after a higher opening and declines in both supply and demand." After the sprint peak at the end of 2025, H1 production and sales experienced a "cliff-like drop," with the industry entering a period of deep adjustment. But looking beyond the data, this "calm period" is precisely a critical turning point for the industry to squeeze out bubbles and solidify its foundation.

I. H1 Production and Sales Data: Multiple Signals Behind the Sharp Chill

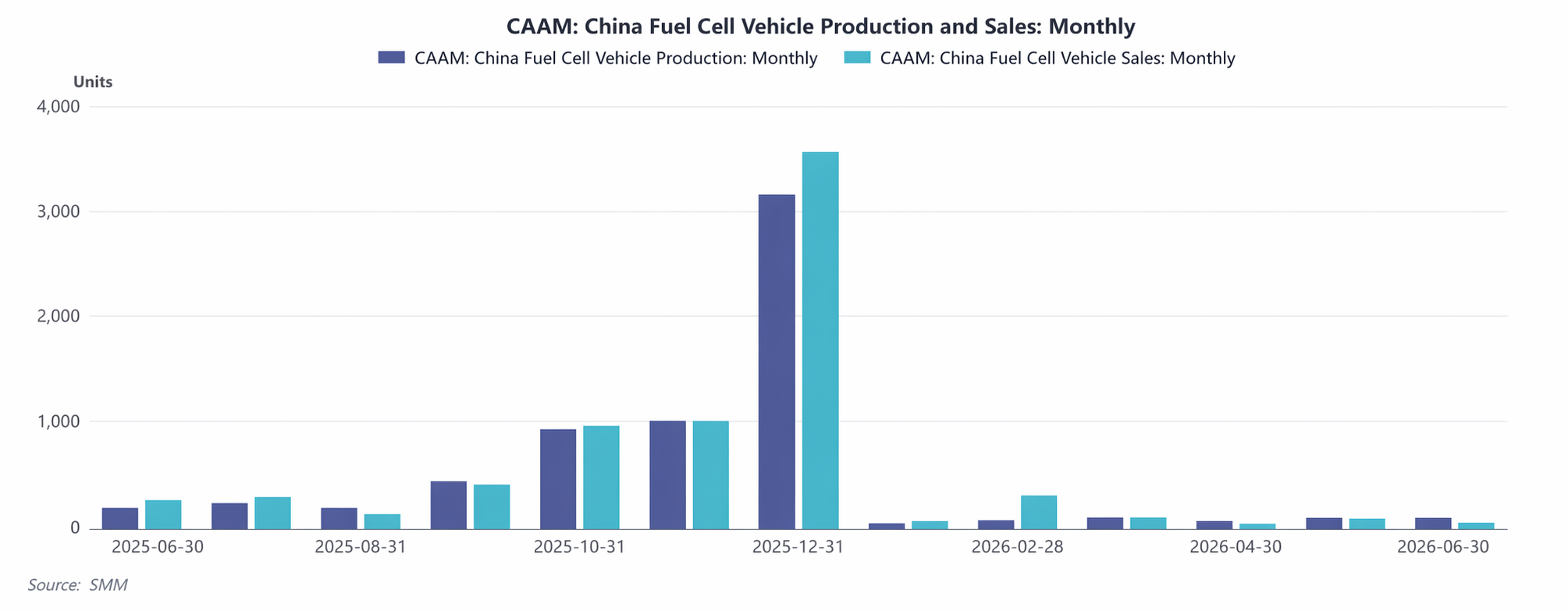

1. Total Volume Plunge: The Real Picture Amid the Harsh Winter

Production side: From January to June 2026, cumulative production was only 401 units, averaging fewer than 70 units per month, a 71.8% YoY plunge compared to the same period of 2025, nearly halving.

Sales side: Cumulative sales reached 550 units, down 63.5% YoY. The once high-growth curve abruptly lost momentum, and market enthusiasm cooled significantly.

2. Monthly Fluctuations: A Rhythm of Fire and Ice in Disarray

Starting with a freeze: In January, production and sales plunged to rock bottom, compounded by the Chinese New Year holiday and a wait-and-see sentiment in the market.

February's "abnormal recovery": Sales surged to 300 units, nearly four times the production volume. This may have stemmed from the concentrated delivery of backlog orders from the end of 2025, or from bulk purchases by a certain region/large client, creating a "false prosperity."

From March to June, a continued downturn: Both production and sales fell back to the 100-unit range. In June, production held at 100 units while sales were only 50 units, quietly driving up inventory pressure.

YoY Disparity: The Double Squeeze of High Base and Policy Vacuum. The "carnival" in H2 2025, especially in Q4 when monthly production and sales exceeded 3,000 units, set a high base trap for 2026. Coupled with the phasing-out of policy subsidies and the start of a new assessment cycle for demonstration city clusters with details yet to be clarified, enterprises adopted a more conservative production pace, end-users fell into a wait-and-see mode, and the market fell into a "policy vacuum period."

II. Industry Growing Pains: The Exposure of Multiple Bottlenecks

Policy Cycle and Fiscal Rhythm Bottlenecks. Fuel cell vehicles are highly dependent on policy "blood transfusions." After the installation rush at the end of 2025 overdrew demand, the pace of local subsidy disbursements slowed in 2026, leaving enterprises hesitant to expand production and users holding back for new policies, plunging the market into a strategic standoff.

Hydrogen Infrastructure Lagging: A Weak Link Constraining the Overall System. While vehicle technology is maturing, hydrogen refueling station construction still struggles to match demand. The February sales surge may have been concentrated in the "island" effect of demonstration cities, while non-pilot regions face a deployment deadlock due to "refueling difficulties," reflecting a fragmented market.

Seasonal and Unconventional Disturbances. The Chinese New Year holiday led to capacity contraction in January and February, yet the counter-trend surge in February sales exposed the dominance of unconventional factors, such as massive purchases by large clients. The subsequent return to normal low ebb reveals insufficient sustained demand.

Cost and Economic Viability Constraints. The cost reduction of fuel cell systems has fallen short of expectations, and coupled with hydrogen price fluctuations, B-end users are highly sensitive to operating costs, suppressing their willingness to purchase vehicles and hindering demand release.

III. H2 Outlook: Winter Will Pass, Recovery in Sight. Based on the weak performance in H1 and historical patterns, H2 is expected to show a "low before high, mild recovery" trend.

Q3: A period of digesting inventories and waiting for the right opportunities. Monthly production and sales may remain in the 100-200 unit range, as enterprises wait for policy implementation or the launch of new demonstration projects.

Q4: Traditional peak season combined with a policy window period could bring a "corrective rebound." While it will be difficult to replicate the peak of 3,000 units per month seen in 2025, there is a high probability of monthly production and sales returning to the 500-1,000 unit range, and the industry will regain growth momentum.

SMM believes that the "data winter" of H1 2026 represents the necessary path for the industry to bid farewell to feverish growth and return to rationality. After the bubbles are squeezed out, true competitiveness will be distilled through technological iteration, infrastructure improvement, and scene implementation efficiency. In H2, as policy tailwinds gradually emerge and infrastructure weak links are addressed, the market is expected to stabilize by the end of Q3, with recovery dawning in Q4.

![[SMM survey] Hydrogen Energy Weekly Electrolyzer Industry Review, 20260710-0716](https://imgqn.smm.cn/usercenter/wZUBk20251217171729.jpg)

![[SMM Survey] Weekly Review of the Hydrogen Energy Electrolyzer Industry, Jul 3-9, 2026](https://imgqn.smm.cn/usercenter/fblvS20251217171729.png)