SMM, July 15:

In H1 2026, China's prebaked anode market saw its price center shift significantly higher, driven by both strong cost push and rigid demand lock-in, while industry profitability underwent a recovery marked by early weakness followed by strength. On the supply side, capacity expanded mildly, with production growth mainly attributable to newly commissioned projects in 2025 reaching full production in a concentrated manner and new projects gradually ramping up. On the demand side, domestic aluminum reached the compliance capacity ceiling, with high operating rates providing rigid support. Exports showed a structural divergence of “Southeast Asia growth, Middle East contraction, and Russia plunge.” Looking ahead to H2, supply-demand fundamentals are expected to remain in tight balance, and price trends will depend more on the disruptive pace of raw material (petroleum coke, coal tar pitch) markets and downstream purchasing and restocking cycles. Meanwhile, sudden supply-side shocks such as environmental protection-driven production restrictions need to be watched.

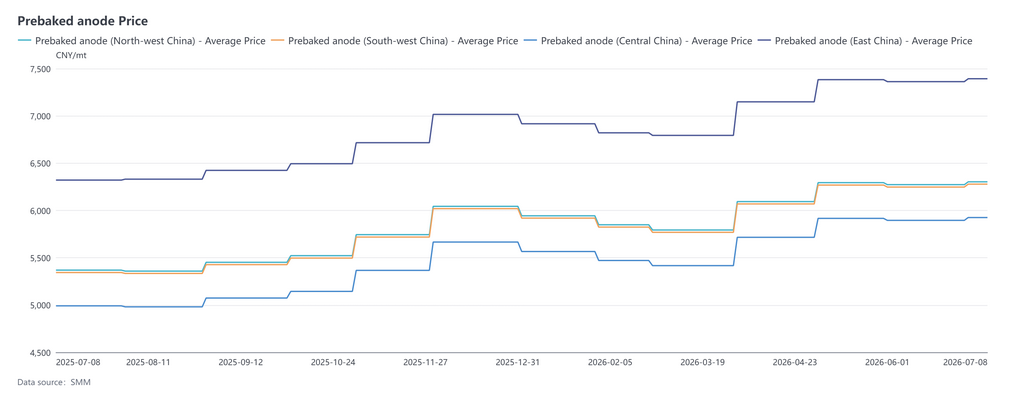

1.Domestic Spot Prices: Consolidating at Lows in Q1, Surging in Q2, Prebaked Anode Price Center Shifted Significantly Higher in H1 2026

In H1 2026, China’s prebaked anode market overall traced a path of Q1 pullback and consolidation at lows, followed by a sharp Q2 surge and subsequent narrow sideways movement at highs. Price trends across East China, Northwest China, Southwest China, and Central China were highly correlated, while regional price spreads remained stable. After extending the year-end 2025 rally into early 2026, the market was affected by the winding down of downstream aluminum stockpiling around the Chinese New Year and production resumptions that lagged expectations. This led to a stronger desire among aluminum smelters to bargain down prices, causing anode prices in all regions to retreat from highs and hit their H1 low in March. A large aluminum smelter in Shandong saw its March procurement benchmark price drop to 5,174 yuan/mt. After the Chinese New Year, propelled by surging petroleum coke prices and supported by stable aluminum demand and incremental export orders from outside China, prebaked anodes entered multiple rounds of stepwise price increases. The procurement prices at the large Shandong smelter were raised by 300 yuan/mt in April and 200 yuan/mt in May. Towards the end of Q2, raw material prices began to ease, with petroleum coke pulling back from highs in a consolidating manner. Downstream aluminum producers showed resistance to high raw material prices, upward momentum faded, and quotations across all regions entered a phase of consolidating at highs. As of June, SMM’s average prebaked anode price stood at 6,445 yuan/mt, up 4.17% from December 2025. The overall H1 price center moved markedly higher compared with 2025, with the industry’s pricing logic heavily dependent on supply-demand dynamics for petroleum coke.

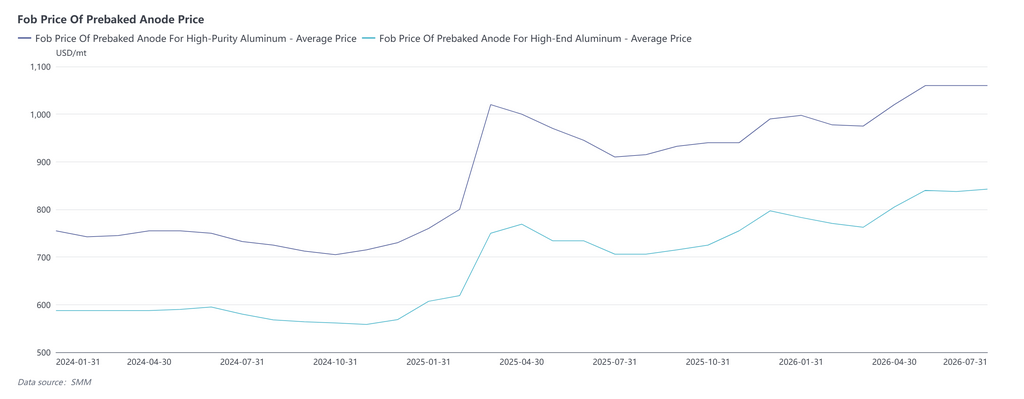

2. Export FOB Price: Driven by Both Raw Material Costs and Overseas Just-in-Time Procurement, Export FOB Price Drifted Higher in H1

In H1 2026, export FOB prices of prebaked anodes for high-purity aluminum and high-end aluminum extended their overall uptrend, moving in tandem with China’s spot prices. Prices in Q1 first fell then rose. At the start of the year, the average FOB price of prebaked anode for high-purity aluminum was around $998/mt, while that for high-end aluminum was near $783/mt. Affected by the Chinese New Year, cost-side support weakened and the overseas procurement pace slowed, causing a concurrent pullback in export prices. Prices stabilized at low levels in March, and starting in April, supported by rising domestic raw material costs and procurement demand from new aluminum capacity outside China, prices stopped falling and rebounded, entering an upward drifting channel. Entering Q2, tighter supply of domestic petroleum coke pushed up anode production costs, coupled with increased stockpiling orders from aluminum smelters in Indonesia, Central Asia and other overseas regions, driving FOB quotes for both products continuously higher. As of end-June, the average FOB price of prebaked anode for high-purity aluminum was about $1,060/mt, and that for high-end aluminum about $838/mt. During this period, geopolitical conflicts in the Middle East disrupted shipping, causing procurement demand to stall, while local anode capacity gradually came online, diverting some traditional export orders. This slowed the pace of price increases, leading to a phase of slight adjustments at elevated levels. Overall, the H1 export FOB price center shifted notably higher compared with the same period in 2025, with pricing largely tracking fluctuations in domestic raw material costs and overseas just-in-time procurement intensity.

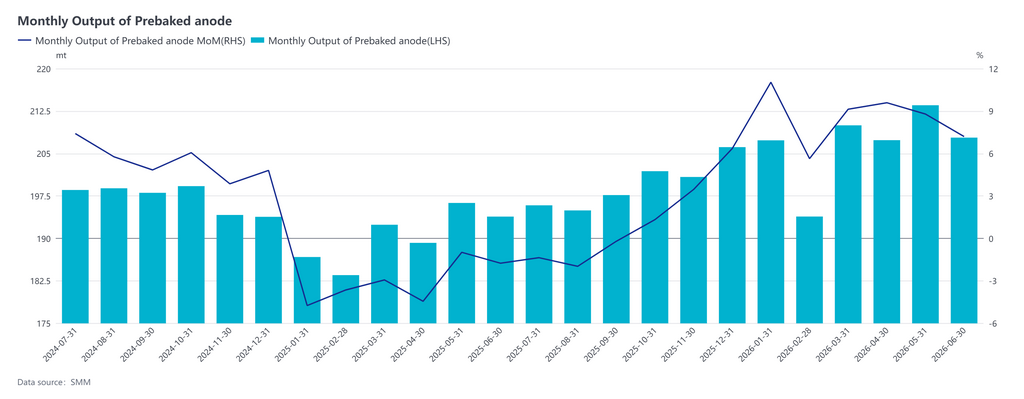

3. Supply Side: Slight Capacity Expansion and Production Ramp-Up of Existing Capacity Driving Output Higher

In H1 2026, capacity in the prebaked anode industry continued to expand, with total compliant capacity rising to 32.635 million mt, edging up 0.62% from the full-year 2025 capacity base. New capacity additions during the year were concentrated in aluminum industry supporting areas such as Northwest China, Guangxi, and Shandong, with new capacity from industry leaders being rolled out in an orderly manner. Meanwhile, the industry continued to phase out scattered and outdated small capacity, keeping overall capacity growth moderate and the industry total supply abundant. On the production side, according to SMM statistics, China’s total prebaked anode production in H1 2026 reached 12.3988 million mt, up 8.57% YoY. The industry’s overall operating rate stayed high in H1, while newly commissioned facilities gradually released capacity. Together with mainstream carbon plants largely maintaining normal production, this drove total output steadily higher.

4.Demand side: domestic rigid demand remains solid, while export markets show uneven performance across regions

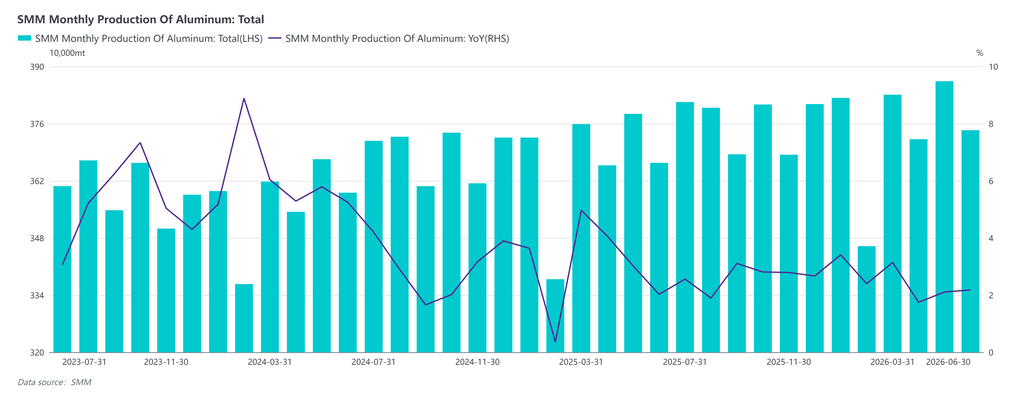

Chinese market: In H1 2026, persistently high industry smelting profits significantly magnified production-side output flexibility. On one hand, the continued strength of aluminum prices maintained attractive per-tonne margins, pushing aluminum enterprises to maximize production willingness. On the other, new projects from year-end 2025 through H1 this year kept entering their ramp-up and commissioning cycles, delivering steady incremental output month by month. The continuous realization of production ramp-up increments from these new projects further supported China’s primary aluminum output scale. Under the combined effect of these two drivers, total domestic aluminum production rose steadily in H1, leaving the market well supplied with raw materials. According to SMM, China’s total aluminum production in January-June 2026 reached 22.444 million mt, up 2.16% YoY. Overall, the supply-side elasticity of aluminum remained relatively weak, with operating rates locked at elevated levels over the long term, and anode procurement demand volumes were largely fixed.

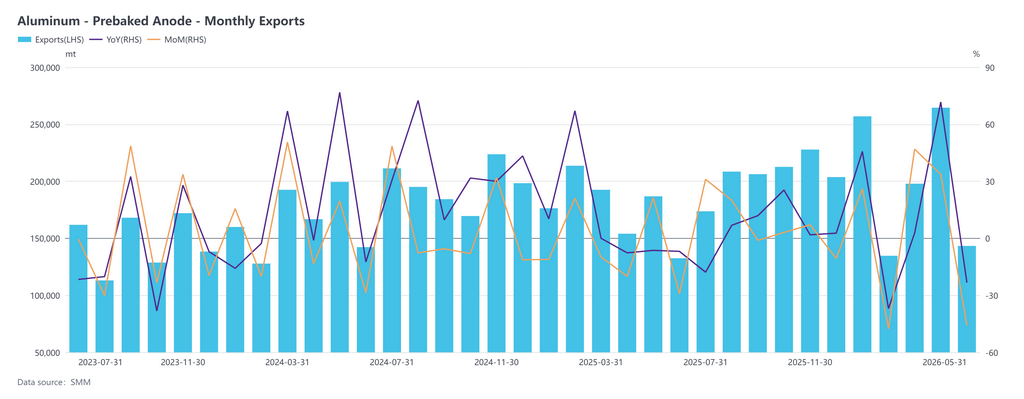

Export market: In January-May 2026, China’s cumulative prebaked anode exports increased 8.01% YoY, maintaining an expansionary trend, but overseas markets showed pronounced divergence. Asia remained the core export destination. Exports to Malaysia, Indonesia, Azerbaijan and other locations surged markedly YoY, benefiting from robust raw-material demand driven by ongoing aluminum capacity expansion in those regions. However, demand in Middle Eastern markets such as the UAE, Saudi Arabia and Oman contracted notably, as aluminum production cuts combined with adjustments in local supply put exports under visible pressure. The European market was a mixed picture. Import demand from Norway, Iceland, Spain and France stayed robust, partly offsetting the gap left by the pullback in exports to Germany and Greece. The Eurasian bloc was dragged down by the Russian Federation, with exports to that market plunging 69.09% YoY, reflecting the far‑reaching impact of geopolitical and trade‑environment shifts that will be hard to reverse in the near term. In North America, Canada maintained slight positive growth and performed relatively steadily. Looking ahead, the continued release of new aluminum capacity in Southeast Asia and Northern Europe is expected to be the main driver of anode export growth.

5. Industry Profitability: Raw Material and Demand Both Drive Profitability, From Stabilized to Weakening and Then Gradual Recovery

A phased review of industry profitability changes:

From January to February 2026, raw material and anode prices passed through smoothly, and the industry maintained a healthy profit range within 200 yuan/mt; from March to April, petroleum coke and coal tar pitch generally consolidated at highs and then pulled back from Q1 highs, while low-sulphur petroleum coke maintained price resilience supported by rigid demand from anode materials. The aluminum industry was constrained by energy consumption, compliance, and capacity controls, leading some aluminum smelters to slow down raw material procurement and production pace, with anode procurement demand weakening marginally. At the same time, enterprises were still digesting high-priced raw material inventories from Q1, and the cost benefits from falling raw material prices could not be easily passed downstream. Inventory impairment further eroded profitability, causing overall industry profits to contract again, and operational pressure on small and medium-sized enterprises intensified significantly. From May to June, cost pressure on the raw material side eased marginally, and the drag on profits from high-priced inventory impairments also eased; downstream demand supported anode selling prices, enabling prices to pass through smoothly in line with raw material fluctuations, with industry profitability returning to positive territory from earlier losses, large and medium-sized anode plants showing stronger recovery, small and medium-sized enterprises reversing losses, the overall profit margin of the industry steadily recovering to a reasonable range of around 100 yuan/mt, the full cost curve edging down from highs, and cost-side pressure weakening marginally.

Looking ahead to H2 2026, the prebaked anode market is expected to seek balance in the tug-of-war between sellers and buyers. Supply side, capacity release coexists with operating rate flexibility. With new projects in Xinjiang, Guangxi, and other regions gradually coming online, the industry's supply capacity is steadily improving. However, constrained by profit margins, enterprises mostly produce based on sales, and the operating rate is expected to consolidate within the 75%-80% range. Demand side shows strong resilience. The operating rate of China's aluminum enterprises stays high, providing solid rigid demand support for prebaked anodes. Meanwhile, the export market shows structural divergence. Although the Russian and Middle Eastern markets are under short-term pressure, Southeast Asia and Northern Europe are seeing continuously climbing import demand, boosted by new aluminum capacity, combined with recovery expectations for demand in the Middle East in H2. This is expected to partially offset the decline in exports elsewhere, with total export volume for the year expected to maintain a slight increase trend. SMM expects China's prebaked anode exports to grow to around 2.45 million mt in 2026, up 6.99% YoY. Cost side, raw material petroleum coke and coal tar pitch prices show structural divergence, but overall cost support remains relatively solid. In summary, the supply-demand fundamentals of the prebaked anode market are expected to remain stable in H2, but against the backdrop of continuously releasing new capacity, industry competition may intensify, and price trends will be more influenced by cost-side fluctuations and downstream procurement pace.

![Cost Support Coupled With Off-Season Demand, ADC12 Price Remains Moving Sideways [ADC12 Price Daily Review]](https://imgqn.smm.cn/usercenter/CkvAg20251217171724.jpg)