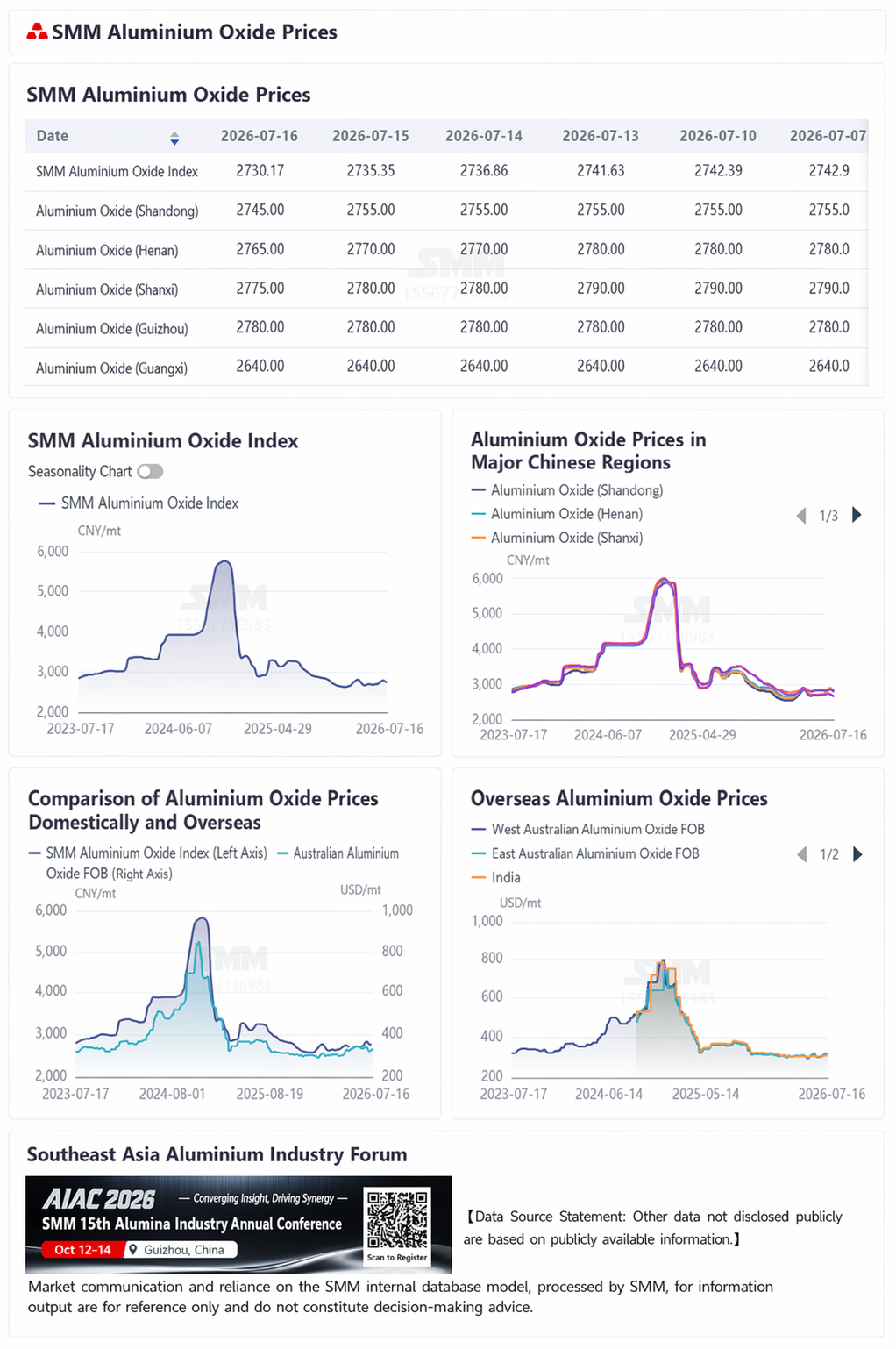

SMM News, July 16:

Price Review: As of this Thursday, the SMM Alumina Index was 2,730.17 yuan/mt, down 12.8 yuan/mt WoW from last Thursday. Among them, Shandong was quoted at 2,710-2,780 yuan/mt, down 10 yuan/mt WoW; Henan at 2,730-2,800 yuan/mt, down 15 yuan/mt WoW; Shanxi at 2,750-2,800 yuan/mt, down 15 yuan/mt WoW; Guangxi at 2,600-2,680 yuan/mt, down 40 yuan/mt WoW; and Guizhou at 2,760-2,800 yuan/mt, basically flat WoW.

Markets Outside China: As of July 9, 2026, FOB Western Australia alumina was $328/mt, the ocean freight rate was $32.35/mt, and the USD/CNY selling rate hovered around 6.78. This translated into an external selling price at China’s mainstream ports of about 2,842.29 yuan/mt, which was 112.12 yuan/mt higher than the alumina index price.

Chinese Market: According to SMM data, as of this Thursday, China’s total installed capacity of metallurgical-grade alumina was 118.42 million mt/year, with total operating capacity at 88.86 million mt/year. The national weekly operating rate of alumina rose 0.66 percentage points WoW to 75.04%. Specifically, Shandong’s weekly operating rate was basically flat WoW at 89.31%; Shanxi’s was basically flat WoW at 63.46%; Henan’s increased 1.17 percentage points WoW to 57.99%; Guangxi’s was basically flat WoW at 78.87%; and Guizhou’s rose 10.71 percentage points WoW to 86%.

Spot Market: One deal was concluded this week. In Xinjiang, a procurement tender was made for 10kt of spot alumina, with delivered prices at around 320 yuan/mt.

As of this Thursday, alumina prices extended their downtrend. Market sentiment was generally pessimistic, futures prices continued to weaken, and the macro front also lacked support, leaving the overall tone bearish. In China, alumina refineries that had previously undergone maintenance gradually resumed production, and supply continued to recover, further intensifying the market’s pressure. From the inventory structure perspective, according to SMM statistics, China’s total alumina inventory fell 63,000 mt MoM this week to 7.004 million mt, indicating an overall destocking pattern. However, the breakdown showed clear divergence: aluminum smelters’ raw material inventory rebounded, mainly because in-transit cargoes from earlier periods arrived at ports in a concentrated manner and were warehoused; alumina refineries’ own inventory was basically flat, edging up 1,000 mt to 1.234 million mt; port inventory plunged 134,000 mt to 779,000 mt, partly because some cargoes were discharged at ports and entered the Chinese market, and partly because a considerable volume was re-exported to markets outside China, resulting in a marked decline in port inventory. Furthermore, affected by the pace of port unloading, platform and in-transit inventories accumulated by 43,000 mt to 1.335 million mt. In terms of production, this week's alumina production increased by 15,000 mt WoW to 1.704 million mt, with the growth mainly coming from the release of resumed production after maintenance in Guizhou and Henan. Overall, although total inventory declined this week, the supply-side production resumption trend is clear. Subsequent arrivals and in-transit cargoes will still face continuous release pressure. The market faces inventory buildup expectations in the short term, and the supply-demand pattern is weak. Alumina prices are expected to continue falling under pressure in the near term.

[Other data beyond publicly available information are based on public information, market communication, and SMM's internal database models, processed by SMM. They are for reference only and do not constitute decision-making advice.]

![The secondary aluminum market moves sideways, and the supply-demand weakness pattern continues during the off-season [Weekly Review of Aluminum Scrap and Secondary Aluminum].](https://imgqn.smm.cn/usercenter/vbcyk20251217171723.jpeg)

![[SMM Aluminum] Middle East Player Resells 90,000 Tons of Alumina Amid Hormuz Tensions](https://imgqn.smm.cn/usercenter/VTjoW20251217171653.jpg)