I. Key Points

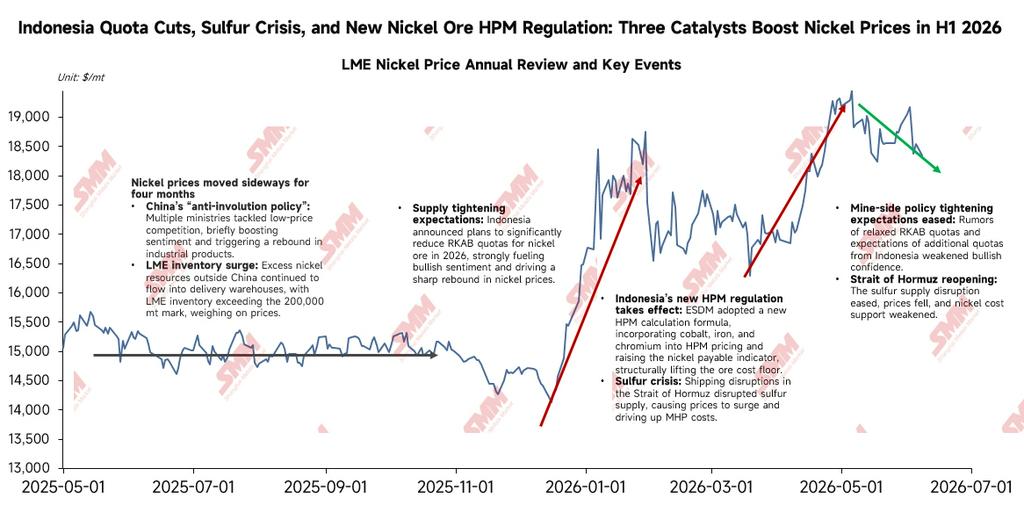

In H1 2026, nickel prices exhibited wide fluctuations characterized by a “rebound from lows—consolidation at highs—pullback and consolidation” pattern. The most-traded LME nickel contract surged from $14,000/mt at the beginning of the year to near $20,000 in May, before pulling back to $16,000-17,000 in July; the most-traded SHFE nickel contract climbed from 110,000 yuan/mt to above 150,000 yuan/mt, and then retreated to 125,000-130,000 yuan/mt. The driving logic of this market move was the intertwined resonance of three main themes: a shift in Indonesia’s resource policies, repeated fluctuations in global macro liquidity expectations, and the impact of geopolitical conflicts on raw material costs. The center of nickel prices did rise compared to 2025, but the “shadow of surplus” has not dissipated.

In H2 2026, the key variables for tracking nickel prices are as follows: First, the approval results of Indonesia’s RKAB quota revision in July. A significant increase in the quota would substantially narrow the supply deficit and weigh on nickel prices. Second, the Fed’s policy path — whether the hawkish signal from the June dot plot will persist — which affects the US dollar index and the valuation center of commodities. Third, sulphur supply and the situation in the Strait of Hormuz, which determines the cost support strength along the MHP–nickel sulphate–refined nickel chain. Fourth, demand from stainless steel and NEV ternary power batteries. Fifth, the pace of global visible inventory destocking. Sustained destocking would serve as a real support signal, while high inventories would limit price elasticity. Under a neutral scenario, LME nickel prices are expected to trade in the range of $15,500-17,500/mt in H2.

II. Macro Environment – Reversal of Liquidity Expectations, Substantial Impact of Geopolitical Costs, and the ‘Dual Strength’ Pattern of the RMB

1. Fed Policy Path: ‘From Dovish to Hawkish’

At the beginning of the year, the market widely expected 50-100 bp of rate cuts in H1 2026, and the US dollar index fell below 97 at one point, creating a relatively loose liquidity environment. However, mid-year, new Fed Chair Kevin Warsh’s hawkish stance surprised the market. The June meeting kept rates unchanged and the dot plot signaled a bias toward rate hikes, leading to a systematic revision of the previously priced “dovish delivery” logic. This directly weighed on the valuation of industrial metals such as nickel, serving as a key macro trigger for the nickel price decline in June.

2. Geopolitical Conflicts Expanded from ‘Safe-Haven Trades’ to ‘Real Cost Shocks’

The Middle East situation (tensions among the US, Israel and Iran, and disturbances in the Strait of Hormuz) not only pushed up energy and safe-haven premiums, but also, through the critical link of sulphur supply, directly raised the production cost of Indonesia’s MHP (each mt of MHP in metal content consumes about 10 mt of sulphur), forming the core driver of the pulse-like surge in nickel prices in May. After a ceasefire agreement was reached between the US and Iran in mid-June, energy and safe-haven premiums receded, leading to a peak and subsequent pullback in commodities, confirming the dual impact of geopolitical variables on nickel prices.

3. China’s Macroeconomy and RMB ‘Dual Strength’ Provide a Unique Offset

Against a generally stronger US dollar, the onshore RMB bucked the trend, appreciating from 6.98 to 6.79 (a gain of about 2.9%). The relative strength of the RMB, with the exchange rate declining (USD/CNY fell), caused import costs to drop sharply, opening the import window and generating arbitrage profits. However, as large volumes of imported nickel flowed into the domestic market, the spot supply of nickel plates in China increased, accelerating the pace of inventory buildup and weighing on domestic prices. At the same time, LME nickel inventories decreased, leading to a repair of the SHFE/LME nickel price ratio, and the import window closed again in May.

III. Indonesia's Industrial Policy—Systemic Transformation from "Expanding Capacity" to "Controlling the Chain to Raise Prices"

In H1 2026, Indonesia's nickel industry policy completed a strategic shift, systematically deploying a policy package centered on "controlling supply, stabilizing prices, and enhancing resource added value," which became the core fundamental variable driving wide fluctuations in nickel prices.

1. Significant tightening of total RKAB quotas and tilted allocation structure

At the beginning of the year, Indonesia's ESDM announced that the 2026 nickel ore quota would be drastically cut from 379 million wmt in 2025 to 270 million wmt. The world's largest single nickel mine project, WBN, saw its 2026 quota suffer a "cliff-like" reduction; its quota was exhausted in May, leading to full-scale production cuts and shutdowns, stoking persistent concerns over tight supply in H1. The Indonesian authorities have clarified that July 1 to 31, 2026 will be the mid-year application period for supplementary RKAB quotas, prioritizing compliant miners with integrated domestic downstream smelting capacity (such as supporting NPI or HPAL projects). The mid-year policy game over RKAB quotas is intensifying.

2. HPM pricing formula reform shifts from single nickel pricing to multi-element comprehensive pricing

The new formula effective April 15 incorporates associated elements such as iron, cobalt, and chromium into the value component for the first time. Indonesia sought to recapture the undervalued value of associated resources into the pricing system, raising benchmark prices for nickel ore and intermediate products across the cost side. However, this reform met strong opposition from the domestic smelting industry, which argued that it would further squeeze smelting profits amid already surging sulfur and energy costs.

3. Indonesian government officially releases new export control regulations for ferronickel (FeNi) and NPI

In July, Indonesia further strengthened export supervision of high-value-added nickel products under Finance Minister Regulation (KMK) No.32/MK/BC/2026 (implementing Trade Minister Regulation No.17/2026). The new regulation targets products under HS Code Ex.7202.60.00, including ferronickel (FeNi) ingots and lumps with nickel content ≥8%, sponge ferronickel (Sponge FeNi) and granular ferronickel (Nugget FeNi) with nickel content ≥4%, as well as low-grade ferronickel products with 2% ≤ Ni <4% and iron content ≥75% (covering some NPI products). Export requires a surveyor's report (LS) and relevant export licenses; from January 1, 2027, export will generally only be allowed through state-owned export enterprises (BUMN Ekspor), with exemptions under specific circumstances.

Overall, Indonesia is currently tightening quotas, raising taxes and fees, and imposing export controls to elevate resource value, seeking to keep nickel prices within its officially recognized desired range ($19,000-20,000/mt) over the long term. On the other hand, it must balance stability of the industry chain and foreign investor confidence in actual implementation, thus exhibiting a game-like characteristic of "tight first then loose, adjusting while implementing."The extreme policy uncertainty was one of the core reasons behind the wide fluctuations in nickel prices in H1.

IV. Changes in Nickel Intermediate Product Raw Materials: Restructuring of the Cost Transmission Chain

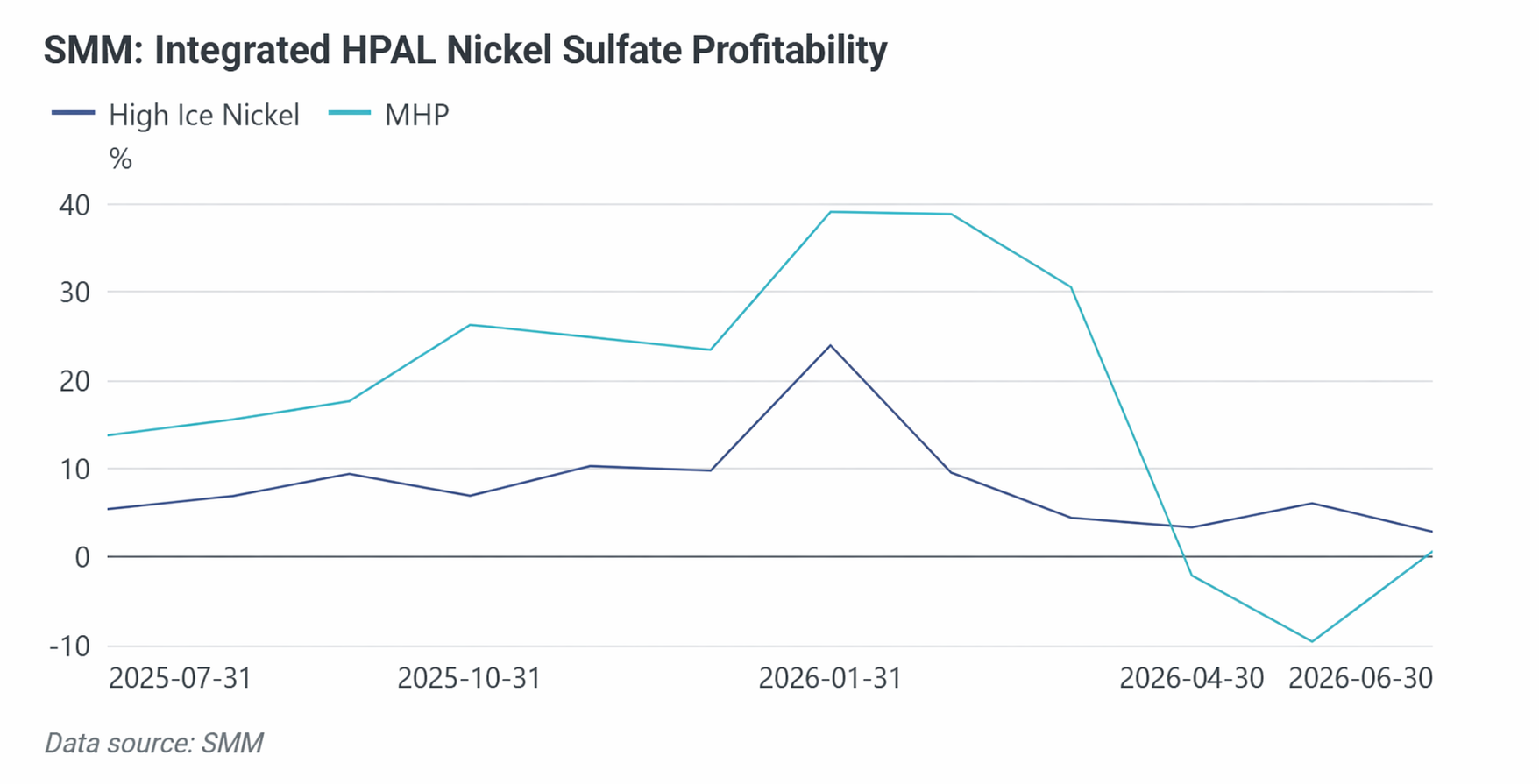

1. MHP and High-Grade Nickel Matte: A Dynamic Game Dominated by "Auxiliary Material Costs"

There are three main production routes for nickel sulphate raw materials: MHP (hydrometallurgy): the dominant route with the largest long-term growth, but highly dependent on sulphur; high-grade nickel matte (pyrometallurgy RKEF conversion / oxygen-enriched side-blowing route): an alternative route with low dependence on sulphur and relatively stable cost elasticity; nickel briquette dissolution: the least economical, feasible only within specific price spread windows.

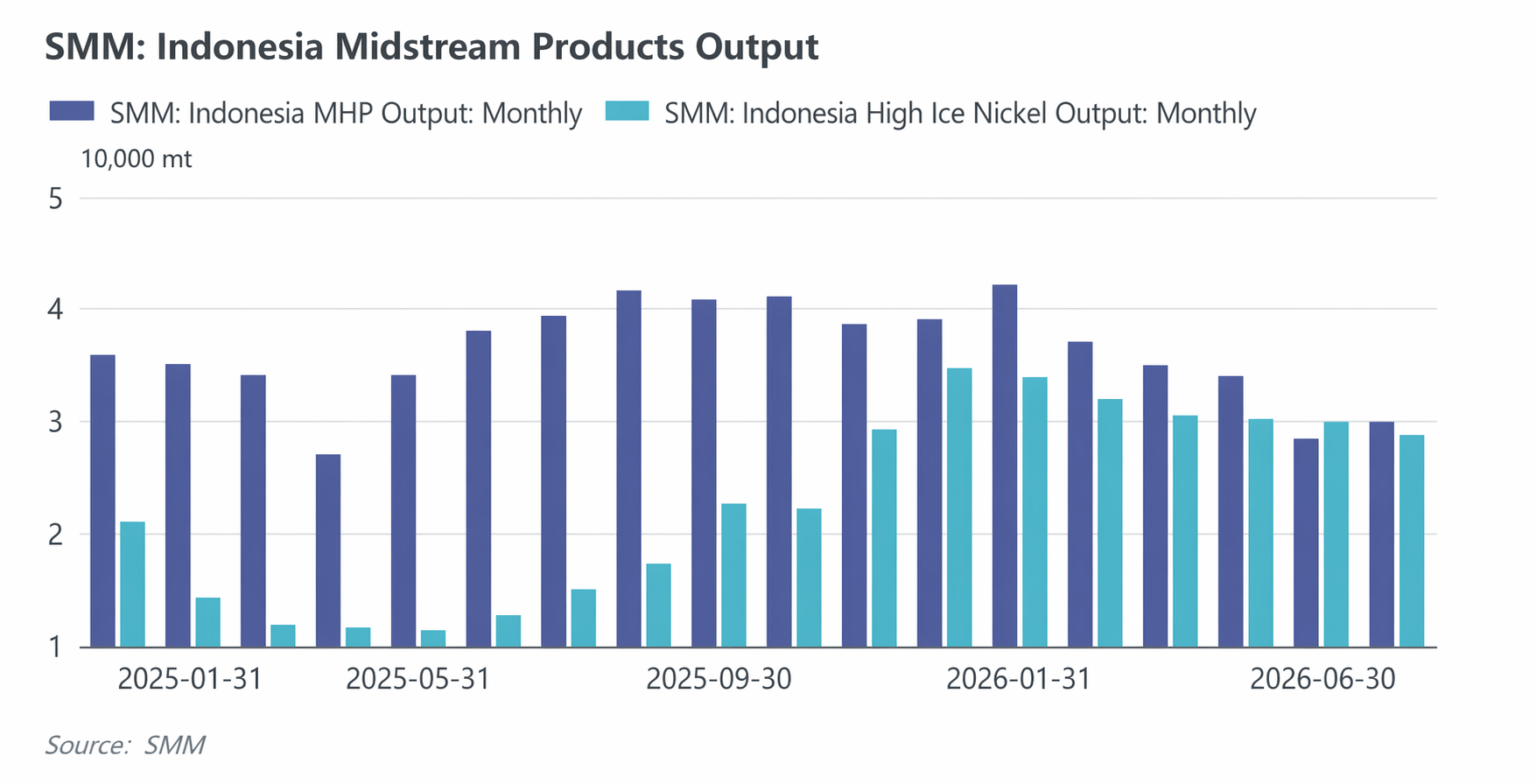

The sharp fluctuations in sulphur prices in H1 reshaped the cost structure of the entire nickel industry chain. Producing one mt in metal content of MHP requires approximately 10 mt of sulphur, while tensions in the Strait of Hormuz disrupted Indonesia’s sulphur import channels, forcing Huayou Cobalt’s Huafei Nickel-Cobalt to cut production on some lines starting in May. Sulphur prices surged, with the SMM sulphur CIF Indonesia price peaking at $1,300/mt, and the cost shock was transmitted step by step along the “sulphur—MHP—nickel sulphate—electrodeposited nickel” chain, becoming one of the core drivers behind the rapid nickel price rise in May. The high-grade nickel matte route, relying on pyrometallurgy, is far less dependent on sulphur than MHP. Consequently, during the sulphur price spike, high-grade nickel matte’s cost advantage over MHP widened significantly, creating direct substitution pressure on MHP’s market share.

In terms of production trends, Indonesia’s MHP production edged up about 0.02% YoY to 206,000 mt in metal content in January-June 2026. Over the same period, high-grade nickel matte posted the most impressive growth, with production up about 123% YoY to 185,000 mt in metal content, strengthening its position in the competition for nickel sulphate raw materials. In the medium and long term, however, once sulphur supply normalizes and MHP costs pull back, the MHP route, with its scale effects and relatively mature cost curve, will reclaim its dominant share of the nickel sulphate raw material market; after all, MHP projects’ capacity base is far larger than that of high-grade nickel matte, and its cobalt by-product also provides a substantial marginal revenue contribution (about $4,500/mt Ni).

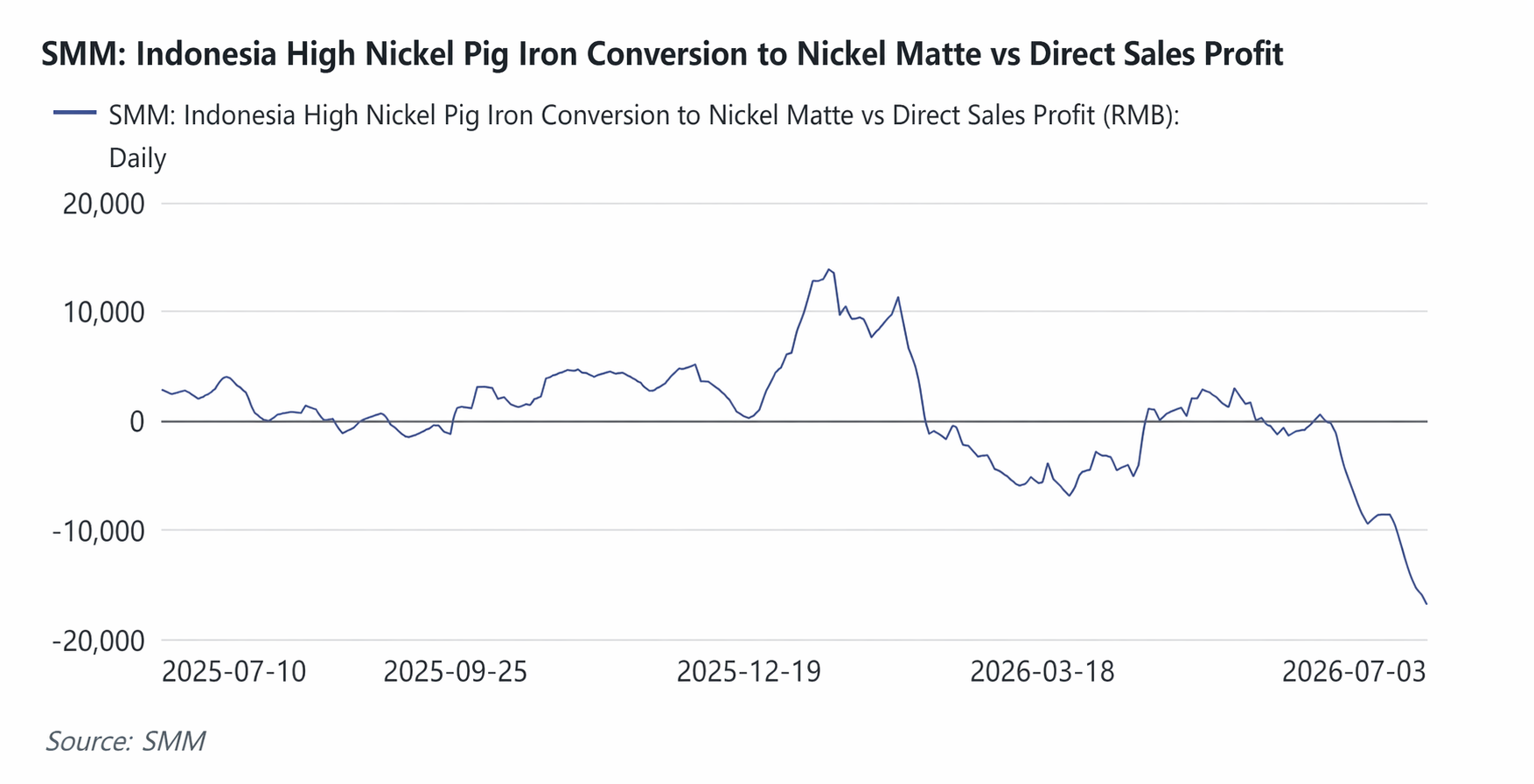

2. Production Capacity Switching Game Between High-Grade Nickel Matte and NPI

High-grade nickel matte and NPI share the same RKEF production lines and laterite nickel ore resources, differing only in whether a sulphidation conversion stage is added at the end. The conversion decision is essentially a profit-maximization problem: when the marginal revenue of high-grade nickel matte relative to NPI covers the additional equipment and process losses of sulphidation conversion, lines switch to high-grade nickel matte; otherwise, they tend toward NPI. The conversion profit chart shows that profit for NPI-to-high-grade-nickel-matte conversion appeared only in April-May. After MHP production cuts in May, the monthly nickel sulphate raw material deficit was about 8,000 mt Ni, theoretically requiring increased high-grade nickel matte production to fill. However, due to RKAB quota constraints and the continued decline in NPI feed grade, integrated enterprises prioritized supplying stainless steel, making it difficult for high-grade nickel matte to offset the MHP raw material shortfall. This was a key reason why nickel sulphate prices remained firm even after refined nickel prices fell sharply in May.

5. Refined Nickel Supply-Demand Pattern: High Inventory vs. Structural Tightness Expectations

1. Supply Side: Electrodeposited Nickel Capacity Continues to Expand, Production Hits Repeated Records

The most certain trend on the supply side is the sustained release of electrodeposited nickel capacity and production in China and Indonesia. According to SMM data, from January to June 2026, China’s refined nickel production was 215,000 mt, a YoY growth rate of 9%; Indonesia’s refined nickel production was 56,000 mt, a YoY growth rate of 97%. Meanwhile, at the beginning of 2026, China’s refined nickel trade pattern underwent a temporary reversal. Previously, benefiting from the explosion in electrodeposited nickel capacity, China had once been expanding its net exports of refined nickel. However, entering Q1 2026, as the price spread between Chinese and overseas markets opened up and the import arbitrage window was activated, China turned back into a net importer of refined nickel, with net imports exceeding 80,000 mt in January-April.

2. Demand Side: New Energy Recovery, Stainless Steel Support, and Steady Alloy & Special Steel

In H1 2026, stainless steel, the largest downstream application of nickel, maintained mild growth. Total stainless steel production in China and Indonesia from January to June was approximately 23 million mt, up about 2% YoY. Steel mills maintained relatively high operating rates throughout H1, with stable apparent consumption.

In the new energy (ternary battery) sector, nickel demand saw a strong recovery. From January to June, China’s ternary cathode precursor production was 528,000 mt, up 32% YoY; ternary cathode material production was 493,000 mt, up 40% YoY.

Alloy & special steel and electroplating, although accounting for a relatively low share of total primary nickel consumption, played a critical role in refined nickel demand in H1 due to their irreplaceability. From January to June, China’s total refined nickel demand was approximately 140,000 mt, up 9% YoY. Military and aerospace demand strengthened, while high-end manufacturing demand remained steady with moderate growth.

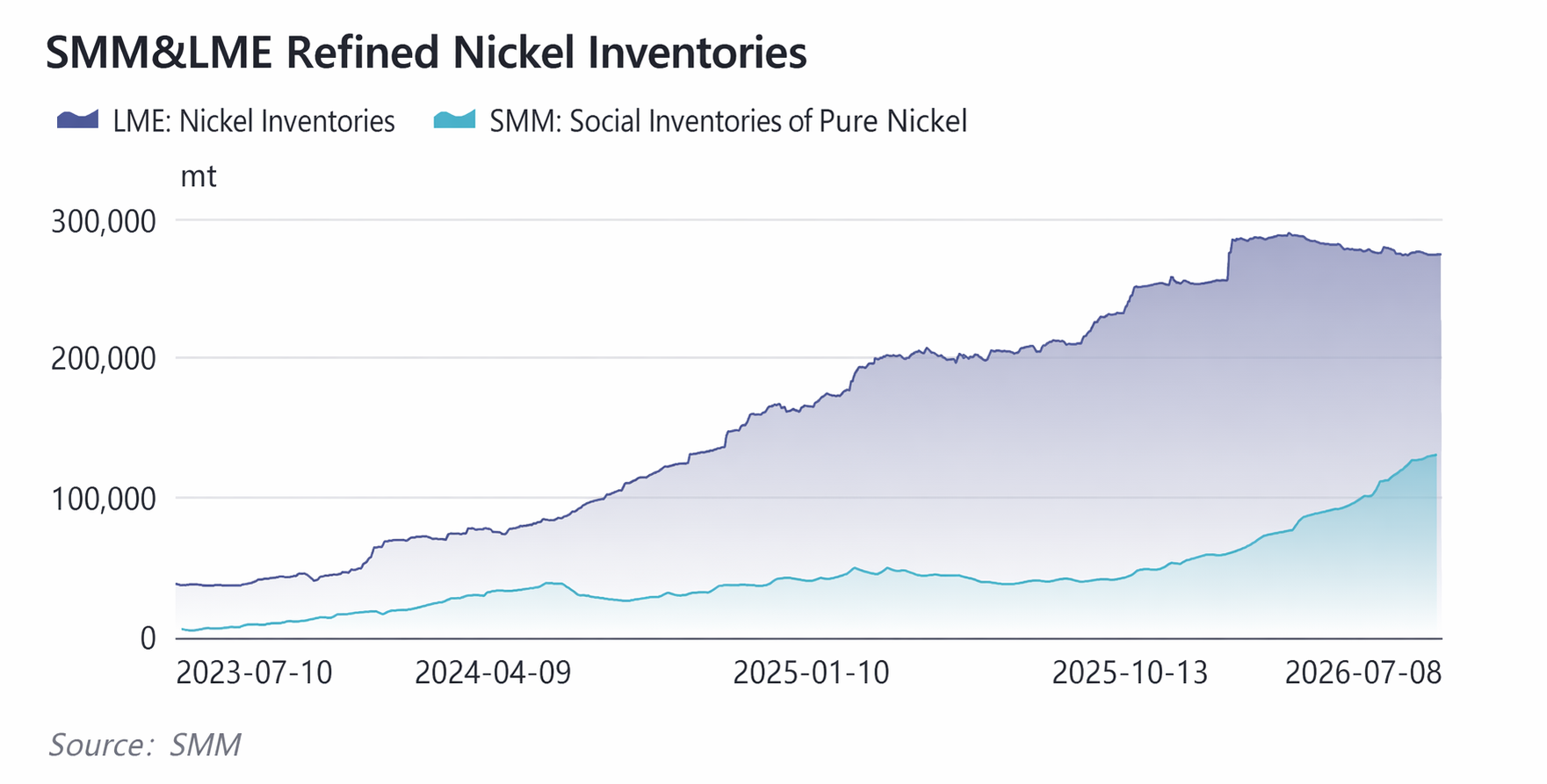

3. Inventory Side: Global Visible Inventory Remains at Historical Highs

Despite wild swings in nickel prices in H1, global visible nickel inventory remained at relatively high historical levels. LME nickel inventory fluctuated in the range of 270,000-280,000 mt for an extended period. China’s social inventory and exchange warrants experienced significant buildup. As of July, SMM refined nickel social inventory reached 130,000 mt, with total global inventory hitting a high of 497,000 mt. High visible inventory posed a significant constraint on nickel price rises. In June, after digesting supply disruption narratives, the market refocused on the fundamental reality of “high inventory and lackluster demand,” and nickel prices pulled back from a temporary high to around $16,100/mt.

6. H2 2026 Risk Alerts and Nickel Price Forecasts

Based on the logic of H1, nickel price trends in H2 are expected to maintain a fundamental pattern dominated by policy gaming, with macro factors amplifying volatility. The following variables merit close monitoring: 1. The final outcome of the RKAB quota revision approval in Indonesia in July; 2. whether the US Fed's policy path in H2 will continue its hawkish stance; 3. whether sulfur supply can substantially return to normal, and whether there is a risk of repeated disruptions in the Strait of Hormuz situation; 4. whether end-use demand from stainless steel and new energy sectors can show a substantial improvement; 5. the destocking pace of global visible inventory.

Based on the above price influencing factors, a scenario analysis for nickel prices is conducted:

Bearish scenario (quotas being more accommodative than expected): quota increase ≥30% + sulfur pullback + high inventory pressure → LME nickel $14,000—$16,000/mt.

Neutral scenario (highest probability): quota slightly increased but still tight + sulfur consolidates at highs → LME nickel $15,500—$17,500/mt.

Bullish scenario (tight quotas + secondary cost surge): quotas continue to tighten + export controls + repeated geopolitical tensions push up sulfur → LME nickel $17,000—$19,000/mt.

![[SMM Stainless Steel Flash] European Commission Launches Consultation on Expanding Scope of EU Steel Regulation](https://imgqn.smm.cn/usercenter/VstiG20251217171732.jpeg)

![[SMM Stainless Steel Flash] Aperam's Stainless Steel Earnings Strengthen in Q2 2026 Amid Higher Prices](https://imgqn.smm.cn/usercenter/KFwsY20251217171734.jpg)

![[SMM Stainless Steel Flash] Chinese Taiwan's Tang Eng Raises 304 & 316L Stainless Steel Prices for August](https://imgqn.smm.cn/usercenter/biBGl20251217171733.jpg)