SMM July 10:

1. H1 Market Review

Supply Side: Operating Rate Lower YoY, Extended Chinese New Year Holiday Curbed Capacity Release

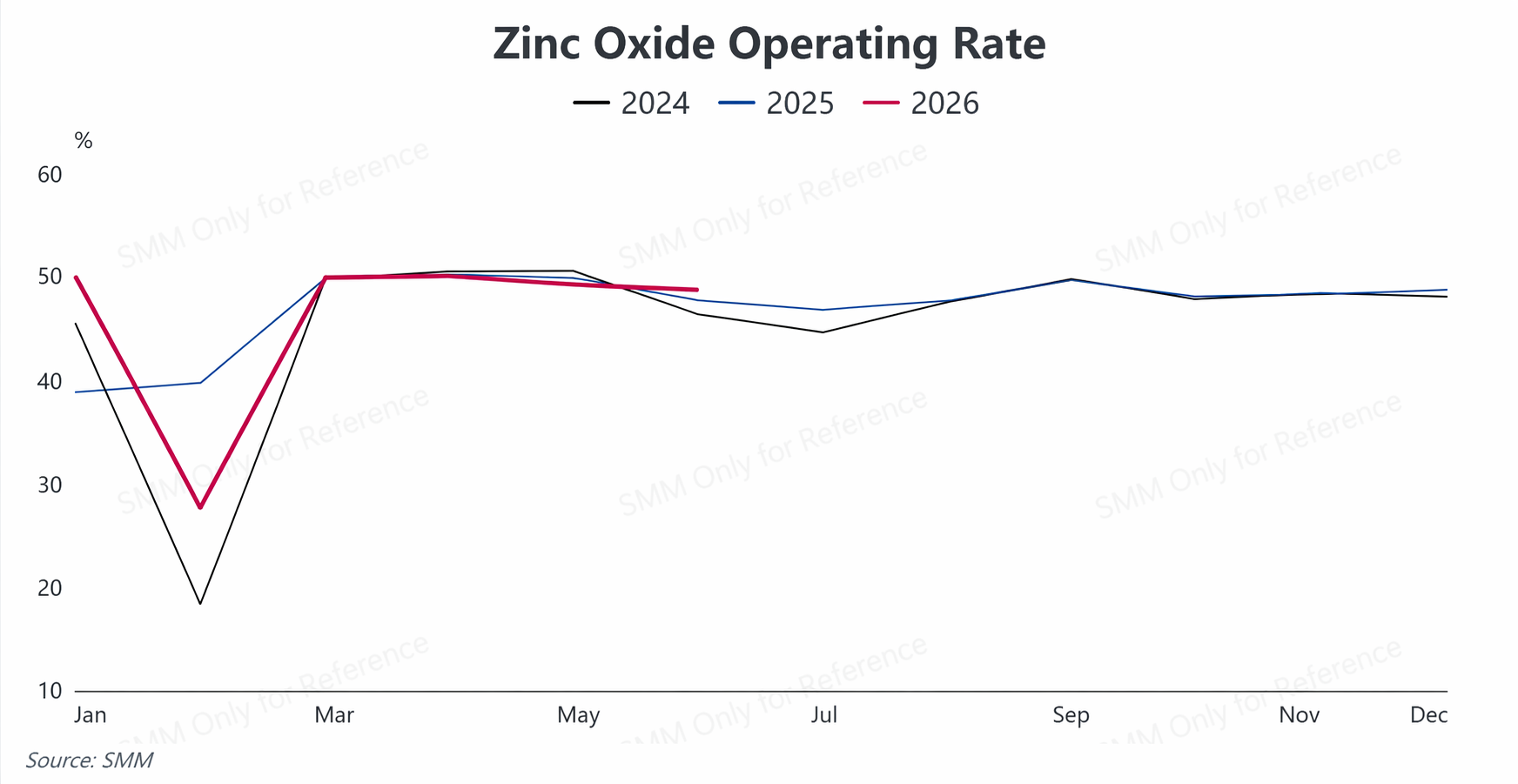

In H1 2026, the supply of the zinc oxide industry showed an overall feature of “production contraction and weakening operating rate.” Before and after Chinese New Year, zinc prices surged beyond expectations, prompting downstream end-users to stand on the sidelines and resist high prices. The average holiday duration for the industry reached 21.35 days, an increase of 1.25 days compared to the same period last year, dragging down capacity release early in the year. After the holiday, the pace of production resumptions remained slow. In March, the industry operating rate briefly rebounded to above 50.43%. Entering the traditional consumption off-season in Q2, coupled with persistently high raw material costs that continued to suppress production margins, the operating rate gradually pulled back from 49.95% in April to 47.96% in June.Overall, H1 operating performance followed a pattern of “plunging low during Chinese New Year – staged recovery after the holiday – weakening again in the off-season.” The industry average operating rate in H1 was down 0.11 percentage points YoY.

Demand Side: Terminal Demand "Uneven", Downstream Sectors Diverge Significantly

In H1, end-use demand for zinc oxide was structurally polarized significantly, with the overall market mediocre and only a few bright spots in niche segments.

Rubber-grade zinc oxide, as the core consumer product in the industry, faced demand pressure. In H1, domestic automobile production and sales declined YoY, and the dealer inventory coefficient rose simultaneously; coupled with Middle East geopolitical conflicts driving up rubber raw material prices, downstream tire enterprises controlled procurement, impacting purchasing demand for rubber-grade zinc oxide. Feed-grade zinc oxide was dragged down by the persistently sluggish pig industry, with orders performing weakly. Ceramic-grade zinc oxide was constrained by the downturn in the property sector, with limited growth in new orders. Only electronic-grade zinc oxide demand showed strong resilience, but the overall market volume of this category was relatively small, insufficient to offset the weak demand across the entire industry.

Cost Side: Multiple Pressures Overlap, Raw Material Market Remains Tight

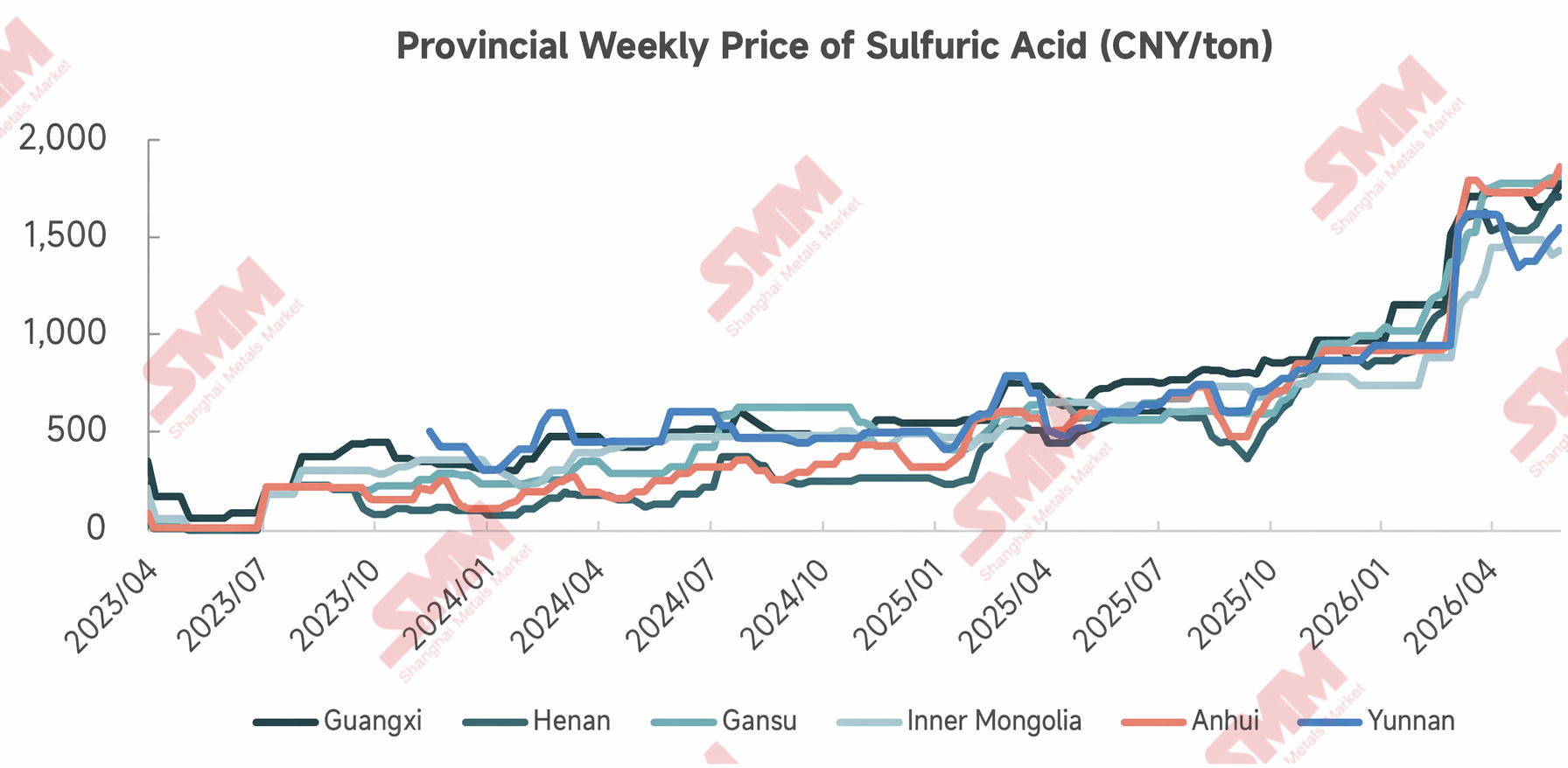

In H1, domestic galvanizing operations weakened YoY, and low-grade zinc oxide production kept declining. Against the backdrop of generally rising prices of raw and auxiliary materials such as zinc slag, low-grade zinc oxide, and sulphuric acid, production costs for some zinc oxide enterprises continued to climb.However, constrained by overcapacity and mediocre end-use demand, product quotations were hard to raise in sync, making it difficult to effectively pass cost pressures downstream, thus continuously squeezing industry profits.

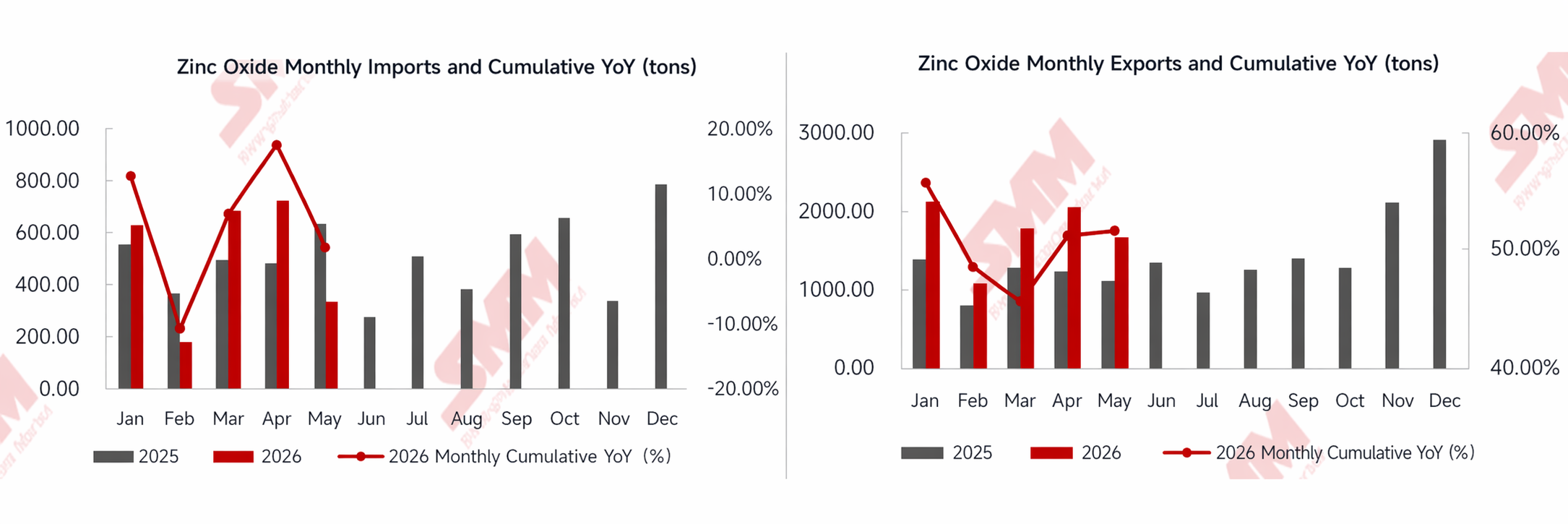

Imports and Exports: Exports Sustain High Growth, Imports Edge Up

In H1 2026, China's zinc oxide trade showed a pattern of “strong exports and mild imports.”From January to May, cumulative domestic zinc oxide exports reached 8,831.86 mt, a cumulative YoY surge of 51.82%. The strong export growth was mainly driven by two factors: first, the SHFE/LME zinc price ratio remained low, giving domestic zinc oxide a noticeable price advantage; second, downstream industries such as tires continued to relocate to Southeast Asia, driving synchronized exports of accompanying zinc oxide. Therefore, overseas exports partially offset the sluggish domestic demand to a certain extent.

On the import side, cumulative imports from January to May reached 2,592.66 mt, edging up 1.70% YoY. Currently, domestic zinc oxide capacity is ample and overseas zinc prices are elevated, so import demand for ordinary industrial-grade zinc oxide should have been suppressed. The slight increase in imports was mainly due to small volumes of high-end, high-purity electronic-grade zinc oxide that still rely on overseas supply supplementation, boosting overall import data marginally.

II. H2 Outlook

Supply-Demand Pattern: Limited Supply Elasticity of Raw Materials, Divergent Recovery in End-Use Demand

On the raw material side, the tight supply of steel dust and electric furnace dust is hard to reverse in the short term. Concentrated maintenance at steel mills and sluggish circulation of invoices in the recycled raw materials market will continue to constrain supply, keeping raw material procurement costs for enterprises high.

On the demand side, June-August is the traditional off-season, while September-October, the September-October peak season, is expected to bring a phased recovery in demand. In specific end-use segments, there are structural positives: the implementation of the State Grid’s 4 trillion yuan investment plan for the 15th Five-Year Plan period, with annual grid investment exceeding 800 billion yuan, is expected to boost demand for electronic-grade zinc oxide; the ongoing implementation of the vehicle trade-in policy, coupled with the steady expansion of NEV production and sales, will provide some support for rubber-grade zinc oxide.

Cost Side: Raw Material Prices and Auxiliary Material Costs Fluctuate at Highs, Limited Room for Profit Recovery

On the low-grade zinc oxide front, persistently rising coal prices directly push up energy costs in the roasting process, while the pass-through of invoice costs will continue to lift the price center. In terms of sulphuric acid prices, SMM expects them to remain in a high-level stalemate from end-June to early July, with the price center likely to shift downward in late July. On the cost side, high sulphur prices provide support, but downstream phosphate fertiliser and titanium dioxide face mounting resistance to high prices, procurement is slowing, and downside correction risks are accumulating.

Overall,

from the perspective of industry development trends, the zinc oxide industry is accelerating its transformation from a "scale dividend" to a "structural dividend." Industry reshuffle amid overcapacity, green and low-carbon technology upgrades, and the strategic shift from "product going global" to "capacity going global" are becoming the main themes of industry development.

(The above information is based on market data collection and comprehensive assessment by the SMM research team and is for reference only. This article does not constitute direct investment advice. Clients should make prudent decisions and not use this as a substitute for independent judgment. Any decisions made by clients are not related to SMM.)