In H1 2026, the nickel ore market in Indonesia and the Philippines entered a new stage of structural adjustment. Unlike previous years, when market attention focused more on downstream capacity expansion, immediate ore availability, and short-term price fluctuations, the core issue in H1 2026 gradually shifted from “supply growth” to “resource value revaluation, refined quota management, long-term ore grade decline, and regional supply reallocation.”

From SMM’s perspective, Indonesia’s nickel ore market in H1 2026 was not driven by a simple supply shortage, but by a systematic adjustment led by policy, resource, and cost factors. On one hand, tighter RKAB approvals have pushed Indonesian ore supply away from a relatively extensive production-release model toward a framework that places greater emphasis on compliance, resource reserves, actual production capability, and matching with downstream demand. On the other hand, the adjustment of the nickel ore HPM pricing formula has gradually shifted the official benchmark price from a single nickel-content-based mechanism toward a new pricing system that also reflects the value of associated elements such as cobalt, iron, and chromium.

At the same time, the Philippines has become increasingly important in Indonesia’s nickel ore balance. Philippine ore is no longer only a short-term substitute during periods of domestic tightness. It is gradually becoming a swing supply source for Indonesia, especially when RKAB approvals, rainy season disruptions, and domestic ore pricing create procurement pressure for Indonesian RKEF smelters.

More importantly, the long-term decline in Indonesia’s saprolite ore grade is becoming a core variable affecting the future nickel ore cost curve. As high-grade saprolite resources are gradually depleted, the furnace inlet grade at RKEF smelters continues to decline. This will significantly increase ore consumption per unit of nickel metal, push up NPI production costs, and reshape the pricing structure across different nickel ore grades.

Overall, the main theme of the Indonesia and Philippines nickel ore market in H1 2026 can be summarized as follows: policy is redefining Indonesia’s supply boundary, HPM is redefining resource value, ore grade decline is redefining the long-term cost floor, and Philippine ore is increasingly acting as the marginal balancing source.

1. H1 Market Review: Indonesia Nickel Ore Shifted from “Supply Expansion” to “Policy Revaluation”

Since the beginning of 2026, Indonesia’s nickel ore market has continued to digest the impact of RKAB system adjustments. As Indonesia’s mining management gradually moves toward a stricter annual approval mechanism, mine-side supply is no longer determined only by mining capacity. Instead, it is increasingly affected by government approval pace, mine compliance, downstream smelting demand, and long-term resource sustainability.

According to SMM’s calculation, Indonesia’s theoretical nickel ore supply in 2026 is estimated at around 297 million wmt, including initial RKAB quotas, supplementary quotas, and Philippine imports. However, considering rainy season disruptions, RKAB approval pace, actual mine production capability, and logistics execution, actual production is expected to be lower than theoretical supply. On the demand side, Indonesia’s nickel ore demand in 2026 is estimated at around 293 million wmt, after considering heavy production cuts in MHP and NPI compared to our initial expectation, indicating that the overall market remains in a tight balance.

This means that Indonesia’s nickel ore market in H1 2026 was not completely short of ore. Rather, nickel ore resources that are “tradable, deliverable, and stable” became more scarce. Mines with stable RKAB approvals, complete compliance procedures, and strong delivery capability saw stronger bargaining power. Meanwhile, smelters without captive mines and those relying on external procurement faced rising raw material procurement uncertainty.

2. RKAB Quotas: The Core Driver of Indonesia Nickel Ore Market Sentiment in H1

In H1 2026, RKAB remained the most critical policy variable in Indonesia’s nickel ore market. The market had previously expected Indonesia to significantly loosen nickel ore production quotas in order to ease raw material tightness for downstream smelters. However, judging from the actual policy direction, the Indonesian government has been more inclined to maintain disciplined quota management rather than simply release large-scale additional supply.

SMM believes that the core issue of the 2026 RKAB policy is not “whether there will be additional volume,” but “how the additional volume will be allocated.” Under the new regulatory framework, supplementary quotas are expected to be approved more on a case-by-case basis. Approval will likely depend on each mining company’s compliance status, reserve conditions, historical production performance, downstream supply relationship, and actual demand, rather than a unified percentage increase across the industry.

This change has had a significant impact on the market. For mines, approved quotas have become more valuable, especially during rainy seasons, logistics disruptions, or periods of regional supply tightness. Miners may show stronger reluctance to sell and a stronger willingness to hold firm offers. For smelters, procurement difficulty does not only come from insufficient total volume, but also from structural differences in available resources. Integrated companies with captive mines and long-term supply agreements have stronger risk resistance, while independent smelters are more exposed to quota approval pace, miner offers, and regional supply volatility.

Therefore, the impact of RKAB should not be assessed only based on nominal quota volume. The more important point is whether approved quotas can be smoothly converted into actual production and market circulation. H1 market conditions showed that even when theoretical quotas existed, physical supply release still lagged due to system verification, mine production schedules, rainy season disruptions, and logistics constraints.

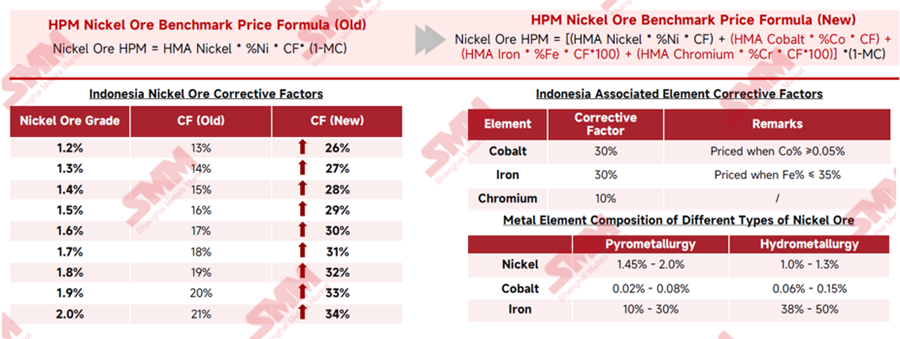

3. HPM Adjustment: Indonesia Nickel Ore Enters a Resource Value Revaluation Stage

In H1 2026, the HPM formula adjustment was one of the most important pricing events in Indonesia’s nickel ore market.

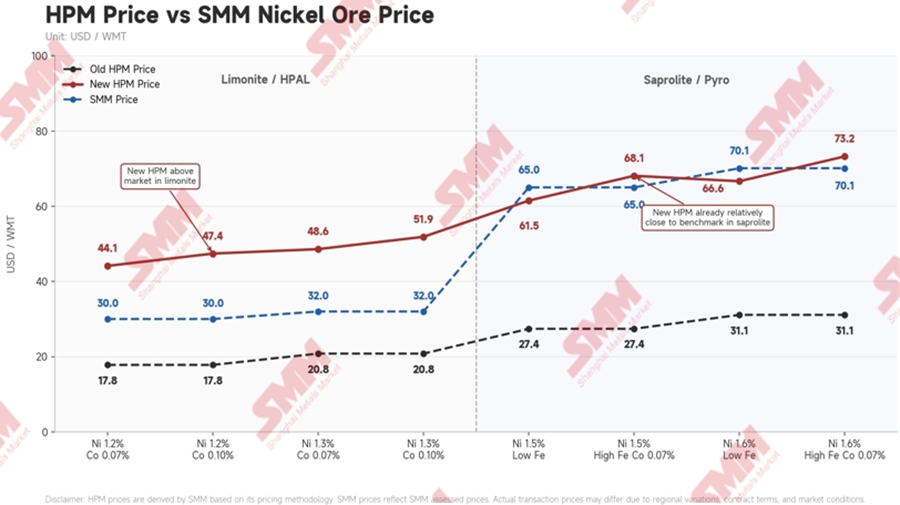

Previously, Indonesia’s nickel ore HPM was mainly calculated based on nickel price, nickel content, correction factor, and moisture content. Under the new formula, the value of associated elements such as cobalt, iron, and chromium is further incorporated, while nickel correction factors for different ore grades have also increased significantly. According to SMM’s analysis, the correction factor for 1.6% nickel ore increased from 17% to 30%, while the correction factor for 1.8% nickel ore increased from 19% to 32%. This means that even before considering associated elements, the benchmark price itself has already risen notably.

The new HPM formula aims to bring Indonesia’s official benchmark closer to actual market prices by incorporating associated-element value. Its impact differs by ore type: limonite may see a stronger price uplift due to cobalt inclusion, increasing costs for HPAL and MHP producers, while saprolite premiums may compress because its previous transaction prices already included high premiums. Overall, nickel ore pricing is shifting toward a more chemistry-based valuation rather than all ore prices rising uniformly.

4. Saprolite Market: Short-Term Premiums May Compress, but Long-Term Ore Grade Depletion Will Continue to Lift the Cost Floor

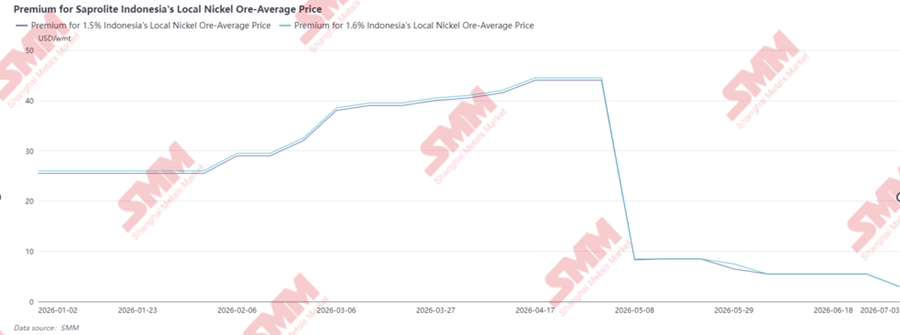

In H1 2026, the saprolite ore market was still supported by RKEF smelting demand, tight tradable supply, and long-term ore grade decline. Indonesia saprolite premiums rose steadily from January to April before dropping sharply in May. Premiums for 1.5% and 1.6% local saprolite stayed around $25–26/wmt, then climbed rapidly to around $40–45/wmt by early April. This increase reflected tight tradable ore supply under slower RKAB approvals, rainy-season disruptions, and stronger miner bargaining power, while the old HPM benchmark remained below actual transaction levels. However, after the new HPM formula was implemented, the premium was quickly reset lower, falling to below $10/wmt in May and continuing to soften into June–July.

Previously, saprolite transactions relied more on the “old HPM plus premium” pricing model. Since the old HPM was clearly below actual market transaction levels, premiums became an important component reflecting supply-demand tightness and resource scarcity. After the new HPM increased, the benchmark price itself moved higher, theoretically compressing market premium space.Therefore, saprolite price trends in H2 may not appear as a one-way sharp increase. Instead, the market may show a process of “benchmark price uplift, premium redistribution, and limited final transaction price adjustment.” If NPI prices remain weak, smelters will find it more difficult to fully accept mine-side cost pass-through, and the upside space for miner premiums may be limited. If NPI prices recover in stages and smelters’ restocking demand improves, saprolite prices will still have support.

Indonesia’s high-grade saprolite resources are undergoing structural depletion. SMM estimates that the average saprolite grade could decline from around 1.66% Ni in 2024 to approximately 1.4% Ni by 2030. Lower ore grades would require smelters to consume more ore to produce the same amount of NPI, while also increasing energy use, slag volumes, and overall processing costs.

In the short term, any increase in saprolite prices may still be constrained by weak NPI margins and smelters’ limited ability to absorb higher raw material costs. Over the longer term, however, continued ore-grade decline is expected to raise the structural cost floor of both saprolite ore and NPI production.

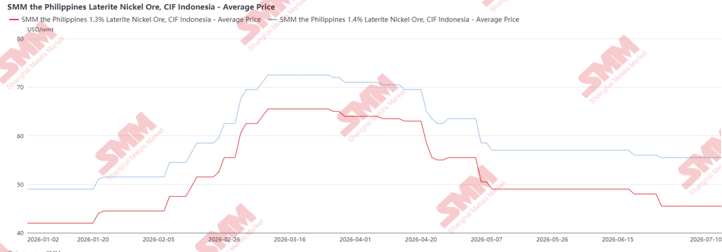

5. Philippine Ore Market: Rainy-Season Tightness Drives Q1 Peak, Dry-Season Supply Pressures Q2 Prices

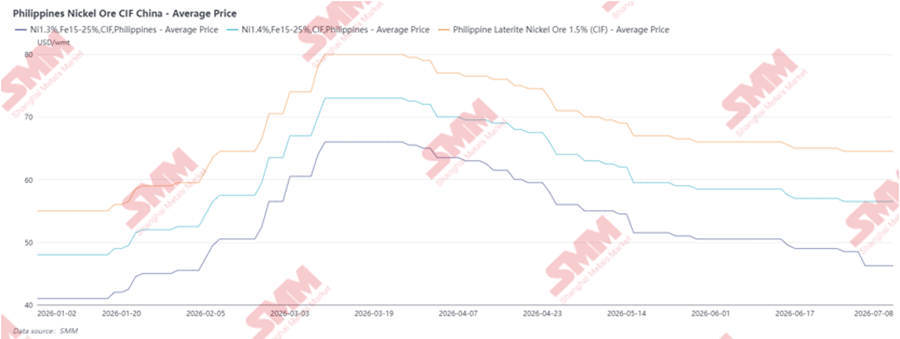

Philippine nickel ore CIF China prices rose significantly in early H1 2026, mainly driven by seasonal supply tightness during the Q1 rainy season. During this period, mining and shipping activities in key producing areas such as Surigao, Dinagat, and Homonhon were disrupted, leaving Zambales as one of the few regions with relatively available export volume. As a result, market liquidity tightened and buyers had to compete for limited cargoes, pushing 1.3%, 1.4%, and 1.5% CIF prices sharply higher. From the chart, prices reached their peak around mid-March, with 1.5% CIF approaching around $80/wmt, while 1.4% and 1.3% also rose to elevated levels.

However, prices began to decline from late March to Q2 as the Philippine dry season started and supply gradually recovered. With more mines resuming production and vessel dispatches increasing, cargo availability improved significantly. At the same time, downstream smelters became more resistant to high ore prices due to weaker NPI margins and started pressuring miners for lower offers. The release of additional Philippine supply, combined with cautious procurement from buyers, pushed CIF prices down through Q2. Therefore, the H1 price trend mainly reflected a seasonal cycle: Q1 prices were lifted by rainy-season supply constraints, while Q2 prices corrected as dry-season supply recovered and smelters gained stronger bargaining power.

From Indonesia's import perspective, Philippine nickel ore CIF to Indonesia prices rose sharply in Q1 2026 due to rainy-season supply tightness, reaching a peak around mid-March, before falling significantly from late March to Q2 as dry-season supply recovered. This price correction made Philippine ore much more attractive to Indonesian smelters. At the same time, Indonesia’s domestic nickel ore prices continued to rise under RKAB constraints, tighter tradable supply, and the new HPM pricing environment, making domestic ore more expensive than imported Philippine ore in some periods. As a result, Indonesian smelters increased Philippine ore imports starting from Q2, not only to supplement domestic fire ore shortages, but also to reduce procurement costs and secure more stable cargo availability.

From SMM’s perspective, Indonesia is absorbing a larger share of incremental Philippine ore supply, with H1 import volumes already rising significantly to meet both blending needs and domestic ore shortages caused by RKAB constraints. Philippine ore has become especially useful for RKEF smelters because it can supplement tight Indonesian saprolite supply while helping adjust furnace feed chemistry. However, this does not mean Indonesia can fully redirect Philippine ore flows away from China. The Philippines will continue serving two major markets: China, which absorbs large volumes of Philippine laterite for its NPI-related chain, and Indonesia, which selectively imports Philippine ore mainly for saprolite supplementation and blending. Therefore, Philippine ore can ease Indonesia’s short-term supply pressure, but it cannot fully solve Indonesia’s structural challenges, including long-term saprolite grade depletion, rising RKEF ore consumption, and tighter domestic resource allocation.

6. Limonite Market: HPM Revaluation and MHP Expansion Strengthen Price Support

Indonesia’s hydrometallurgical ore prices increased in H1 2026, supported partly by RKAB tightness and limited tradable ore availability. However, the increase was less aggressive than pyrometallurgical ore, as hydrometallurgical ore demand was more directly affected by HPAL and MHP operating conditions. Prices rose strongly from late March to April, with 1.2% ore reaching around US$33/wmt and 1.3% ore reaching around US$35/wmt, before easing in Q2. The correction was mainly driven by weaker MHP-side demand, as some producers implemented significant production cuts due to tailings facility constraints and sulfur supply shortages. These issues weighed on HPAL operating rates and reduced near-term hydrometallurgical ore procurement demand. As a result, although RKAB tightness still provided some support, weaker downstream demand limited further upside and caused prices to soften slightly during Q2.

Compared with pyrometallurgical ore, hydrometallurgical ore is more directly affected by the new HPM formula because of its relatively higher cobalt content. After cobalt was included in the pricing mechanism, the theoretical valuation of hydrometallurgical ore increased significantly. Meanwhile, Indonesia’s HPAL and MHP capacity remains in an expansion cycle, meaning hydrometallurgical ore demand still has a solid medium- to long-term growth foundation as projects are gradually commissioned and ramped up.

However, H1 2026 also showed that the HPAL value chain remains exposed to cost risks. Elevated sulfur prices and sulfur supply disruptions had a visible impact on MHP margins. If the new HPM pushes hydrometallurgical ore prices higher while sulfur costs remain elevated, MHP producers will face rising pressure from both raw material and auxiliary material costs. Because of this, HPAL producers have been reluctant to accept the new HPM benchmark as the actual transaction price, and have continued to push for below-benchmark pricing, especially as MHP production cuts weakened short-term ore demand.

At present, most miners are absorbing the additional royalty burden caused by the higher benchmark price, as smelters remain unwilling to fully accept HPM-based pricing. This additional cost is estimated at around US$3–4/wmt, which miners have largely been unable to pass through to downstream buyers. However, further downside room remains limited because more projects are expected to operate in H2. Therefore, SMM expects hydrometallurgical ore prices to remain generally supported in H2, but the pace of any increase will depend on whether MHP project ramp-up brings continuous incremental procurement demand, and whether sulfur prices and MHP margins allow higher raw material costs to be passed downstream.

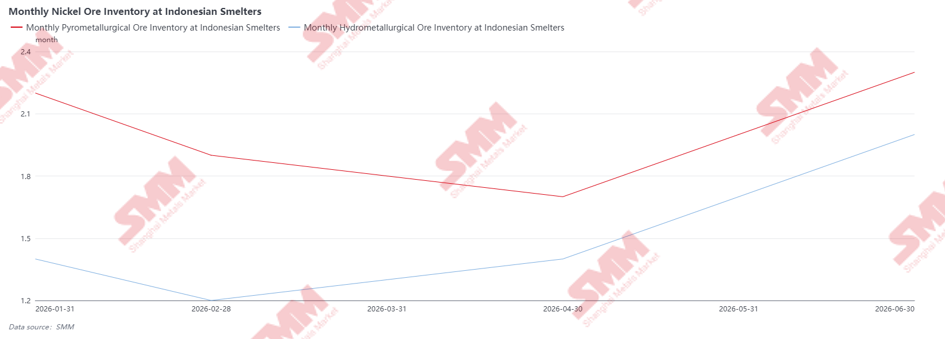

7. Nickel Ore Inventory at Indonesian Smelters: Early-H1 Procurement Constraints Eased Toward June

Nickel ore inventories at Indonesian smelters declined in early H1 2026, mainly because smelters were unable to purchase and receive large volumes smoothly amid rainy-season disruptions, RKAB uncertainty, tighter tradable ore availability, and changing pricing terms. This was especially visible for pyrometallurgical ore, where inventory coverage fell through April as RKEF smelters continued consuming existing stocks while domestic saprolite availability remained constrained.

From May to June, inventories recovered noticeably as weather conditions improved, Philippine ore arrivals increased, and smelters rebuilt raw material buffers ahead of potential H2 policy and quota uncertainty. The recovery in pyrometallurgical inventories to above 2 months suggests that some RKEF smelters became more proactive in securing ore once availability improved, especially given concerns over supplementary RKAB approval pace and long-term saprolite grade decline. For hydrometallurgical smelters, nickel ore procurement remained active but was not particularly aggressive. However, significant production cuts in H1, mainly due to high sulfur costs and weaker MHP margins, reduced ore consumption and pushed inventories up to around 2.0 months by end-June.

8. Downstream Impact: Mine-Side Costs Transmit to Intermediates

In H1 2026, the impact of Indonesia’s nickel ore policy revaluation gradually transmitted to the downstream value chain.

For NPI producers, pressure mainly came from two aspects: higher saprolite costs and increased ore consumption due to declining furnace inlet grades. As high-grade nickel ore of 1.6% and above supply decreases, RKEF smelters need to use more low-grade ore or blended ore to maintain production. Ore consumption per unit of nickel metal rises accordingly, lifting the long-term cost curve. For HPAL producers, sulfur prices remain the key cost variable. Although the new HPM formula has lifted limonite’s theoretical value, smelters have not fully accepted higher limonite prices amid weak MHP margins and elevated sulfur costs. As a result, the pass-through into actual transactions remains limited, keeping the immediate impact on HPAL raw material costs relatively moderate.

H2 Outlook

In H2 2026, Indonesia’s nickel ore market is expected to remain in a tight but manageable balance. The key uncertainty lies in supplementary RKAB approvals, which will determine how much additional supply can enter the market and how it is distributed. Even if quotas are released, supply is unlikely to return to previously loose conditions, and tradable resources may remain constrained, especially for independent smelters.

Philippine ore will continue to act as an important swing supply, particularly when Indonesian domestic prices are high or when smelters require blending material. However, its role will remain supplementary rather than substitutive, as imports are limited by ore quality, export capacity, and competing demand from China.

In terms of pricing, pyrometallurgical ore prices may face short-term correction pressure at the beginning of H2 2026, mainly due to price corrections, relatively high ore inventory levels at smelters, weak NPI margins, and possible premium compression after the HPM adjustment. However, toward the end of the year, prices may regain upward momentum as companies gradually consume their approved RKAB quotas and the rainy season approaches, especially in Sulawesi, which could once again disrupt mining and logistics activities. Therefore, pyrometallurgical ore prices may show a pattern of short-term correction followed by renewed support later in H2.

For hydrometallurgical ore, there is limited expectation for a sharp price increase in the short term, as HPAL and MHP producers remain cautious under margin pressure and elevated auxiliary material costs. However, if new HPAL/MHP projects are commissioned and ramp up smoothly in H2, hydrometallurgical ore demand could gradually improve, creating some upside potential for prices.

Further regulatory tightening remains a key risk for H2 2026 and 2027. The market will closely watch the procedure and mechanisms of NPI or ferronickel-related products are formally included under the DSI export framework, as this could centralize export procedures and increase supervision over contracts, pricing, shipment data, and export proceeds. While this would strengthen government control over resource value, it may also increase administrative friction and reduce export flexibility for producers. In addition, further HPM fine-tuning remains possible, especially for limonite. Since the current formula includes cobalt, iron, and chromium, limonite is more directly affected due to its higher cobalt content. If calculated limonite HPM rises too far above HPAL/MHP affordability under weak margins or high sulfur costs, the market may expect clarification or adjustment in the execution mechanism. Therefore, future regulation will remain a key factor shaping limonite pricing, NPI exports, and downstream cost transmission.