I. H1 Summary: High Prosperity Initially, Stabilizing Later, with Prominent Structural Highlights

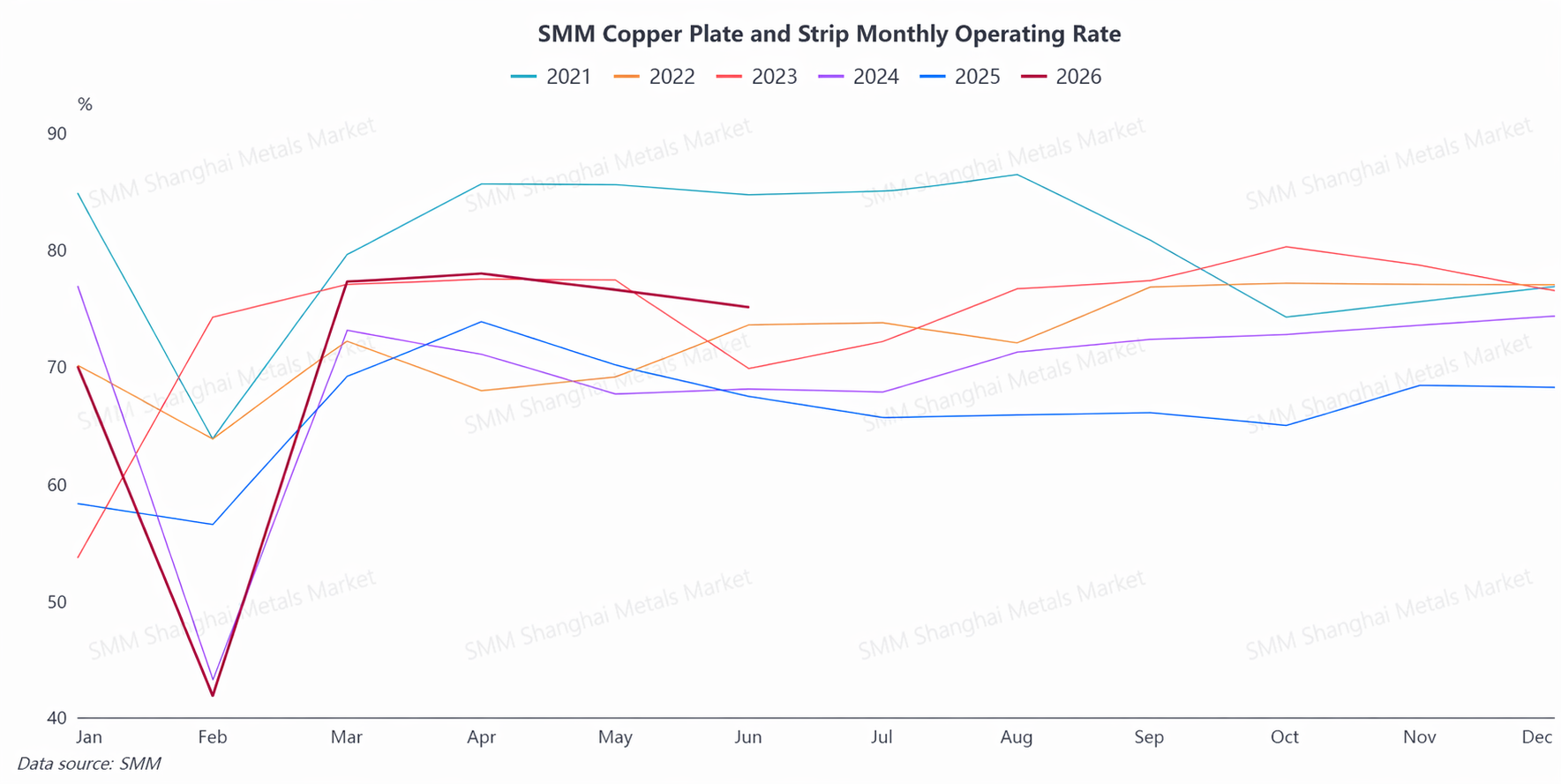

In H1 2026, China's copper plate/sheet and strip industry, after experiencing wild swings in copper prices at the start of the year and the seasonal disruption of Chinese New Year, entered a rapid recovery path from March, showing an overall pace of being under pressure in January-February, surging in March-April, and pulling back mildly in May-June. The industry's average operating rate in H1 was about 73%, significantly higher than the same period in 2025, with the April rate hitting a four-year peak for the same month.

(A) Supply Side: Top-tier players maintained high-load utilization of their capacity, and the entire industry kept a high production pace. However, the tightening of secondary copper-related policies led to a tighter supply of taxed recycled raw materials, and the supply of brass strip billets was tight, periodically constraining production release at some enterprises.

(B) Demand Side: Robust consumption in key downstream sectors such as power transformers, NEVs, energy storage, and semiconductor lead frames continued, becoming the main boost keeping the industry's prosperity high.The industry underwent a full cycle in H1: “copper prices staying high and under pressure → centralized demand release after a phased pullback in copper prices → full order books and tight supply → subsequent mild pullback in new orders.”Entering the mid-to-late Q2, although new orders weakened marginally, the June off-season operating rate still far exceeded market expectations, showing a clear “stronger-than-usual off-season” pattern.

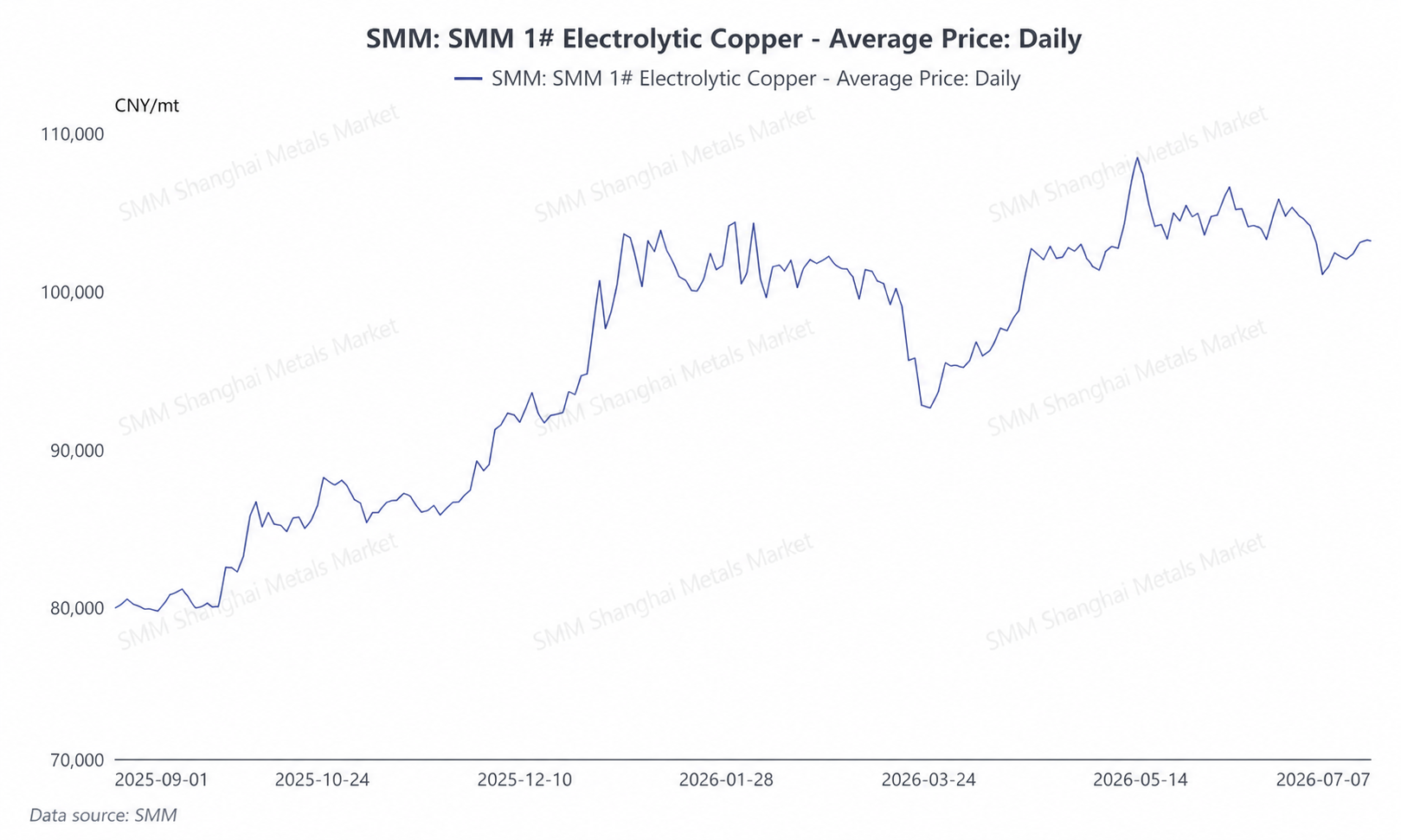

(C) Price Side:Copper prices swung wildly at highs, forming a clear linkage with the operating rate

In H1 2026, the SMM #1 copper cathode price ranged roughly 92,800-108,500 yuan/mt, with an average price of about 101,825 yuan/mt. The copper price trend underwent a complete path: “fluctuating at highs at the start of the year → deep correction to near 93,000 yuan/mt in March → then consolidating and rebounding to a semi-annual high of 108,000 yuan/mt → pulling back in June to fluctuate in the 101,000-106,000 yuan/mt range.”High copper prices had a dual impact on the copper plate/sheet and strip industry: on one hand, they significantly increased raw material procurement costs and capital utilization rates, with downstream acceptance capacity near its limit when copper prices were high at the start of the year; on the other hand, after the phased pullback in copper prices in March, previously pent-up orders were released intensively, directly driving the unexpected rebound in the operating rate in March-April. This transmission logic of “copper price pullback → demand release → operating rate surge” was the most core market driving characteristic in H1.

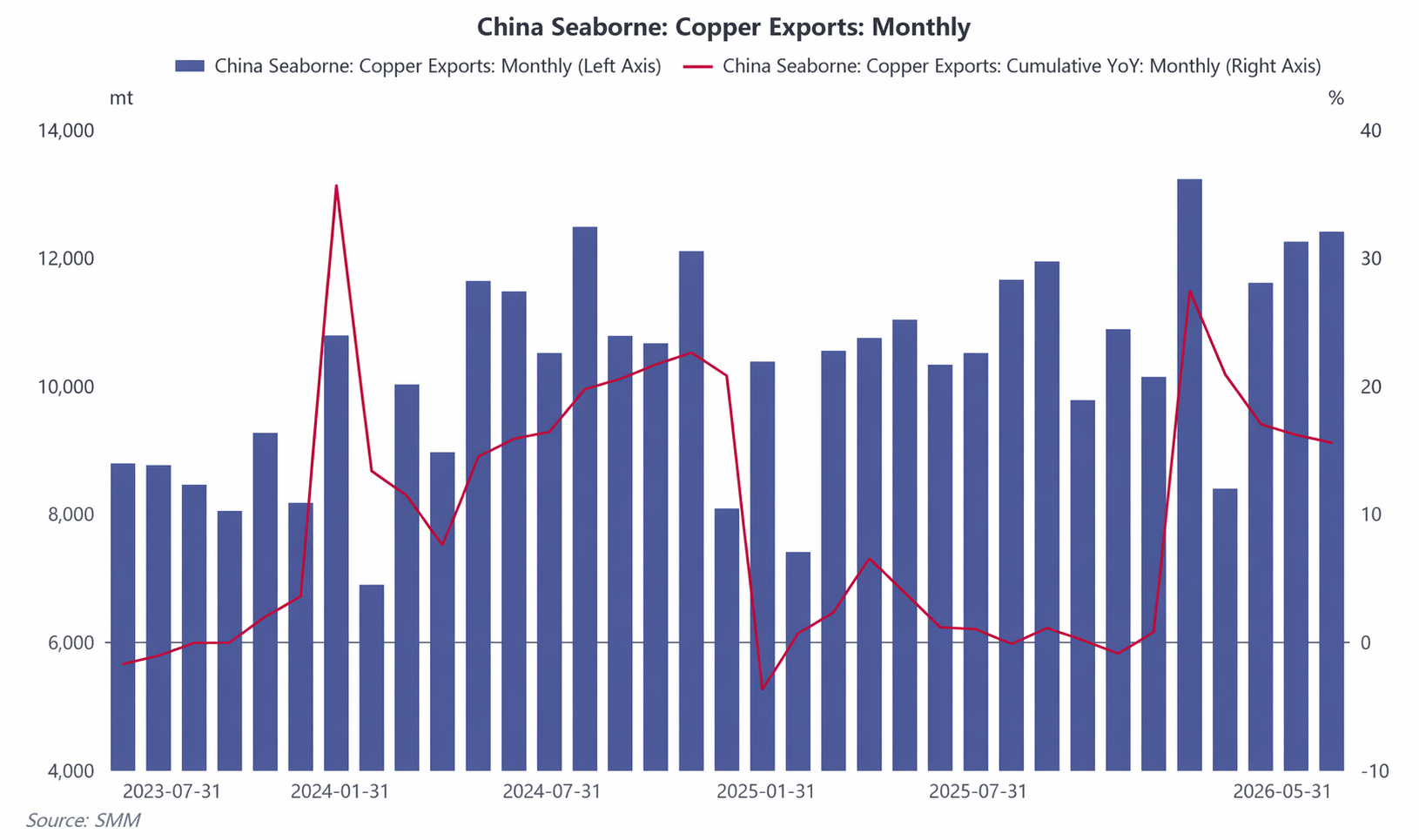

(D) Import and Export Side: Exports continued their high boom, with deepening diversification.

Copper plate/sheet and strip exports performed strongly in H1. China's copper plate/sheet and strip exports totaled approximately 57,893 mt in January-May, up 15.57% YoY, with monthly exports maintaining double-digit YoY growth, extending the high export momentum of the industry.

By destination, South Korea, Vietnam, Taiwan, China, and Japan were core markets for China's copper plate/sheet and strip exports. Among emerging markets, Canada and Mexico showed notably strong performance. By trade mode, the share of processing trade with imported materials stabilized in the 65%-69% range, while the share of Ordinary Trade fell below 10%. The industry export structure has largely completed the shift from Ordinary Trade to processing trade.

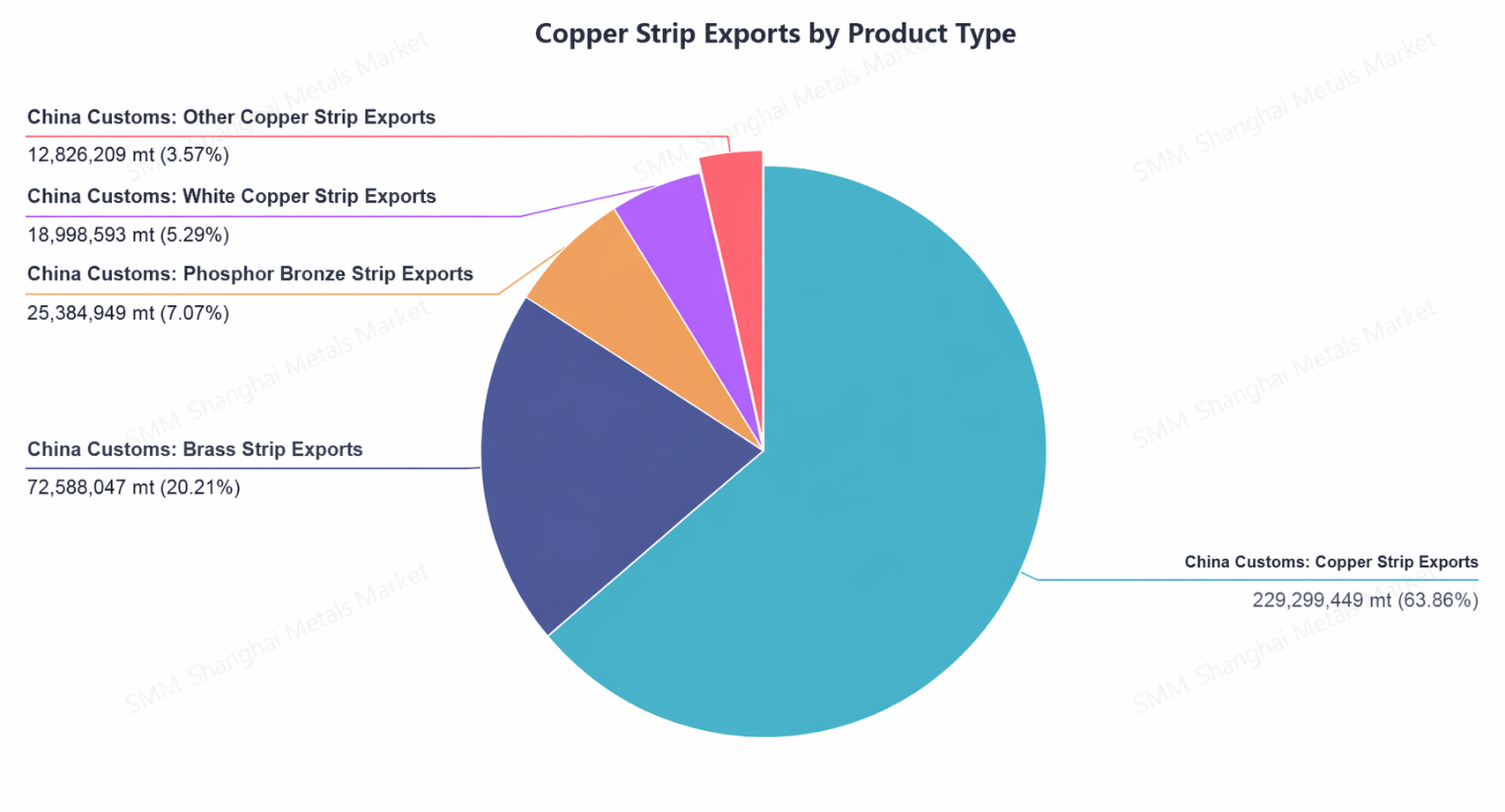

In terms of product mix, copper strip remained the dominant export, accounting for over 60% with steady growth; cupronickel strip posted impressive export growth; brass strip exhibited a diverging pattern of rising copper strip and declining brass strip.

(V) Policy: Secondary copper policies push up costs, external trade environment grows more complex

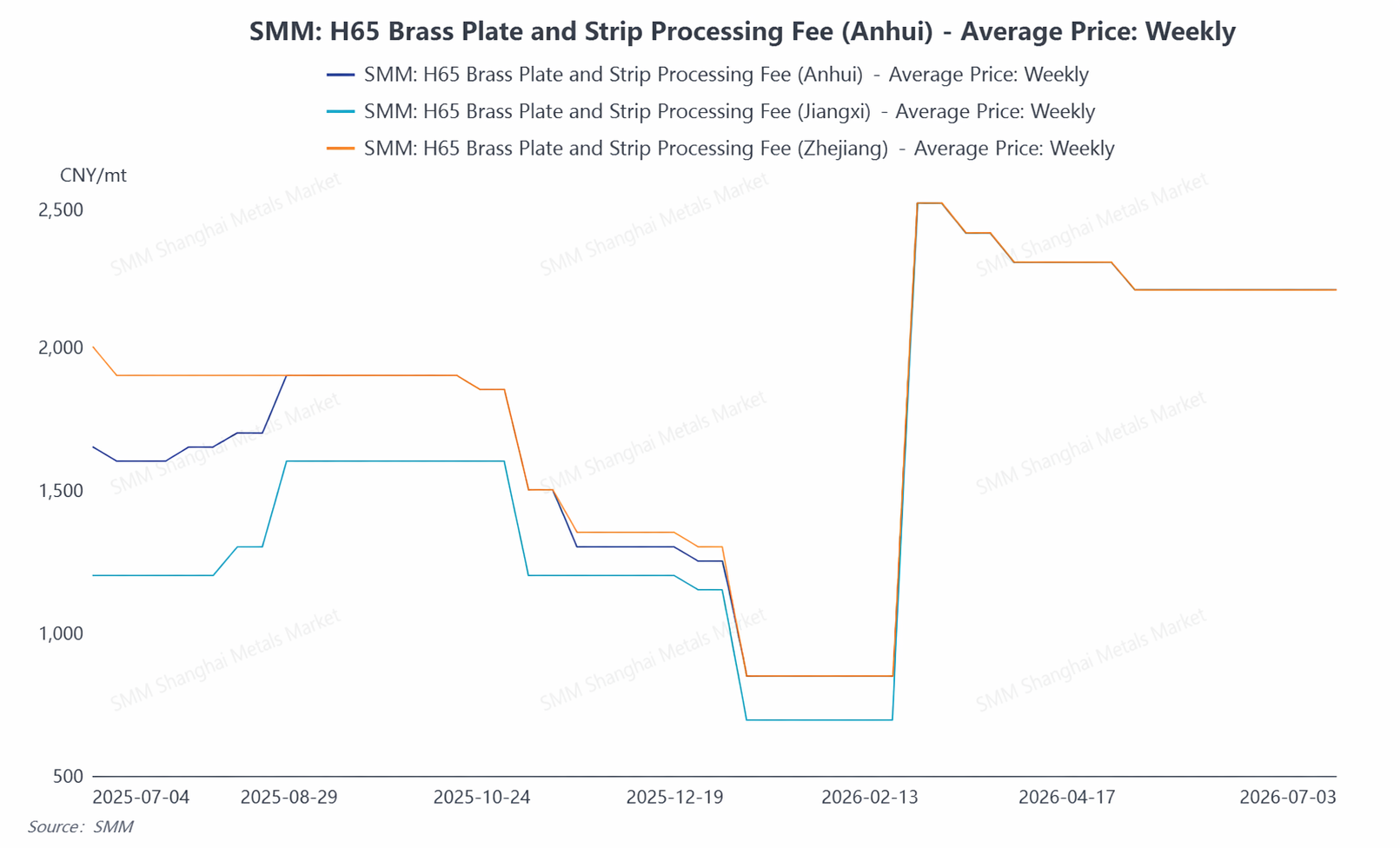

Secondary copper policy was a key variable affecting the industry in H1. Affected by tax policies such as "reverse invoicing," copper plate/sheet and strip enterprises generally faced dual pressures of difficulty in procuring recycled raw materials and sharply climbing production costs. Tin-phosphor bronze strip producers were forced to cut output, some small enterprises in Jiangxi saw reduced production willingness, and brass strip RCs were generally raised to around 2,000 yuan/mt, with regional price spreads largely disappearing.

On the export policy front, the impact of the cancellation of export tax rebates for copper plate/sheet and strip in December 2024 is still being absorbed. The industry has completed the trade mode shift, but enterprise operating costs and compliance requirements have both risen. Internationally, the US maintains a 50% tariff on semi-finished copper products, profoundly affecting global trade flows of semi-finished copper products. The trend in some regions to promote localized processing of critical minerals is also introducing new variables into the long-term export landscape.

II. H2 Outlook: "Stronger-than-usual Off-season" Expected to Persist, Emerging Sectors Become "Ballast"

Looking ahead to H2 2026, the copper plate/sheet and strip industry is expected to maintain an operational pattern of "stable overall volume, structural divergence, and ample resilience." Demand side, traditional sectors (construction, decorative hardware, low-voltage electrical appliances, etc.) will continue to weaken seasonally in H2, but emerging tracks are becoming the "stabilizer" for industry operations: AI computing center construction is accelerating, driving rapid growth in data center copper demand; the energy storage sector continues to expand, boosting incremental use of copper plate/sheet and strip in battery connections, thermal management, etc.; the penetration rate of flat wire motors for NEVs is steadily increasing, keeping demand for high-end copper alloy strip robust; power transformers and UHV construction are entering a concentrated delivery period, which will strongly underpin orders for transformer copper strip and other products. On the export side, the H1 cumulative YoY growth rate of 15.57% set a high base for the full year, and combined with the continuous progress of new energy and power infrastructure outside China, the quality and cost-effectiveness advantages of Chinese copper plate/sheet and strip will continue to open up space in emerging markets. But we need to be vigilant about the potential risks of rising global trade protectionism and a phased demand pullback in some markets.

On the whole, the copper plate/sheet and strip industry in H2 2026 will navigate between strong resilience support from emerging sectors and seasonal pressures. High-growth sectors such as AI computing power, energy storage, and new energy vehicles will serve as the “ballast stone” for the industry’s performance, and the trend of structural upgrading and increasing concentration is expected to accelerate further.

![Copper Prices Pull Back, Secondary Copper Rod Enterprises Mainly Wait and See [SMM Secondary Copper Daily Review]](https://imgqn.smm.cn/usercenter/XTMPt20251217171713.jpeg)