Starting from October 2025, new steel mill export schedule data was added. The planned production of rebar and wire rod includes exports, but excludes billet exports.

According to an SMM survey of 56 sample major steel producers:

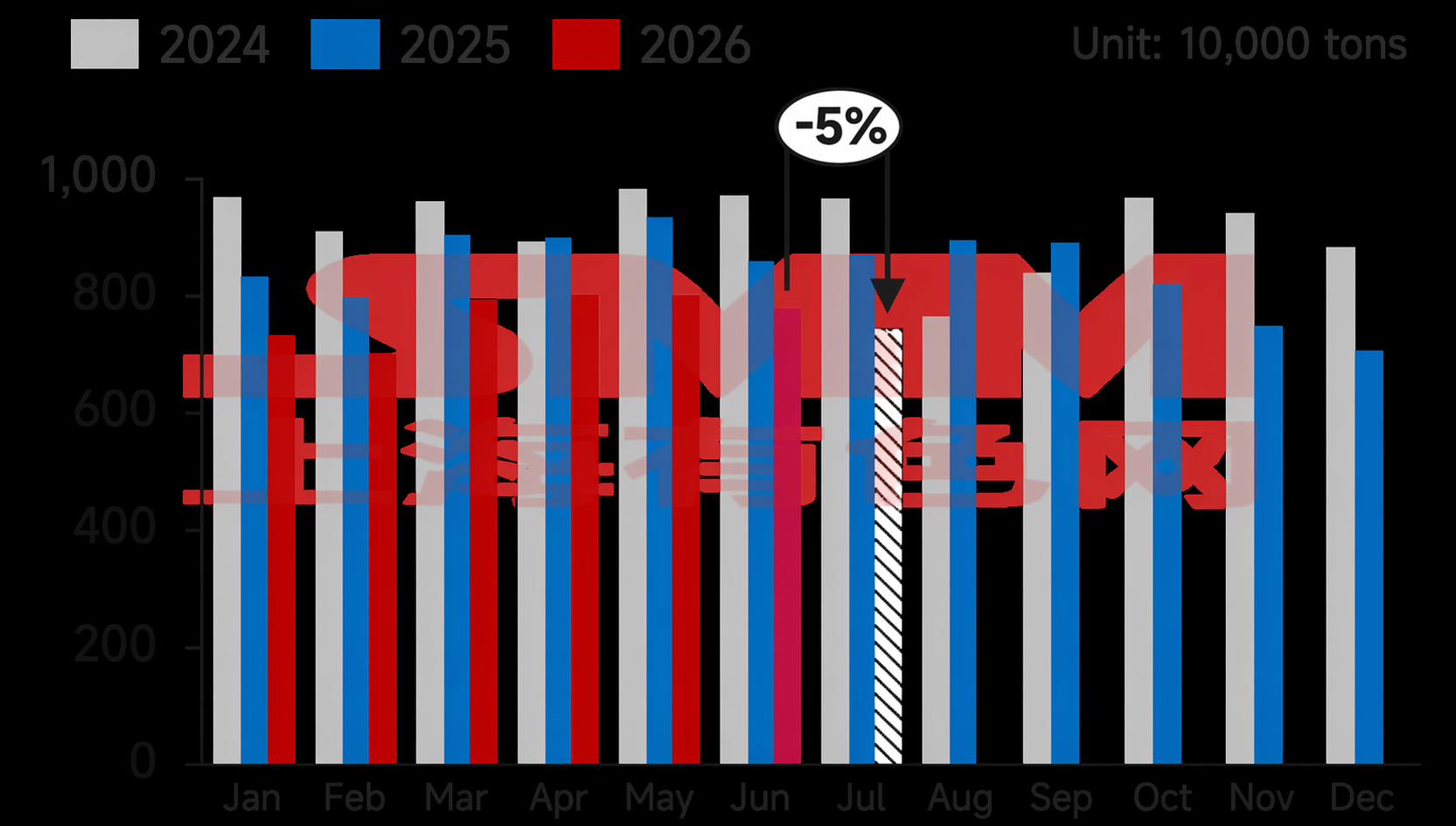

- In July, planned rebar production was 7.428 million mt, down 389,700 mt or 4.98% from June's actual production; daily rebar production in July was 239,600 mt, down 8.05% MoM.

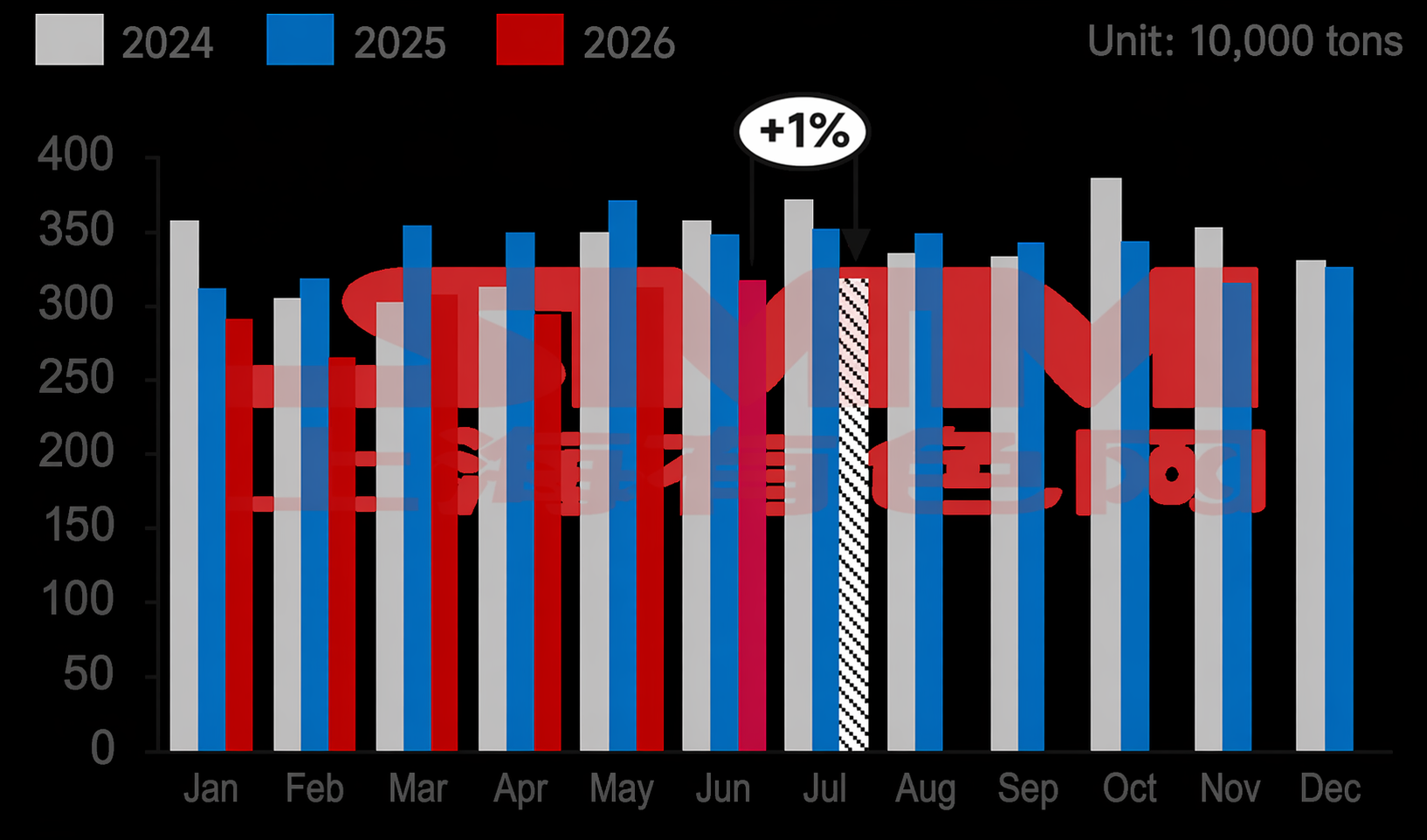

- In July, planned wire rod production was 3.197 million mt, up 18,700 mt or 0.59% from June's actual production; however, daily wire rod production in July was 103,100 mt, down 2.66% MoM.

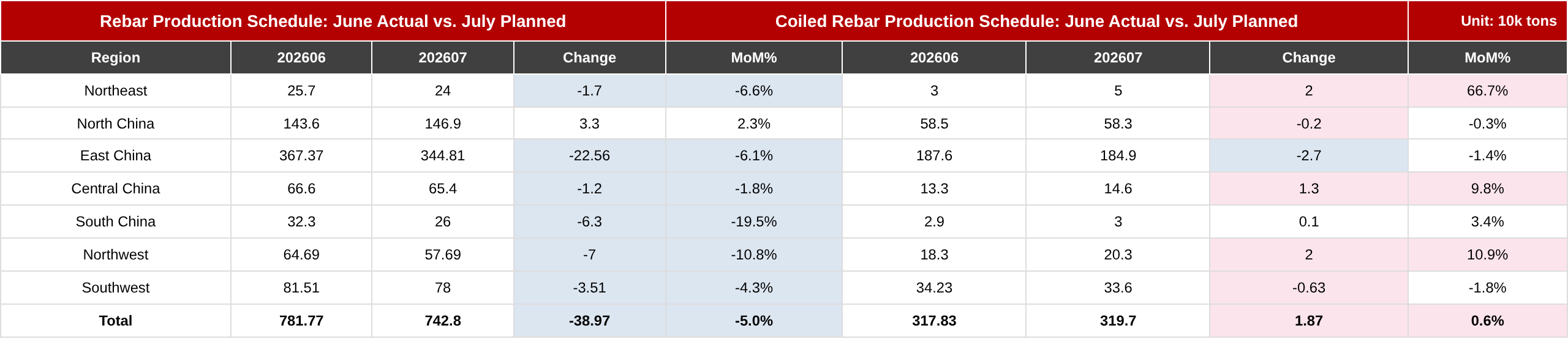

Chart 1-2: Rebar & Wire Rod Production Schedule at Mainstream Construction Steel Mills (56 Mills)

Source: SMM

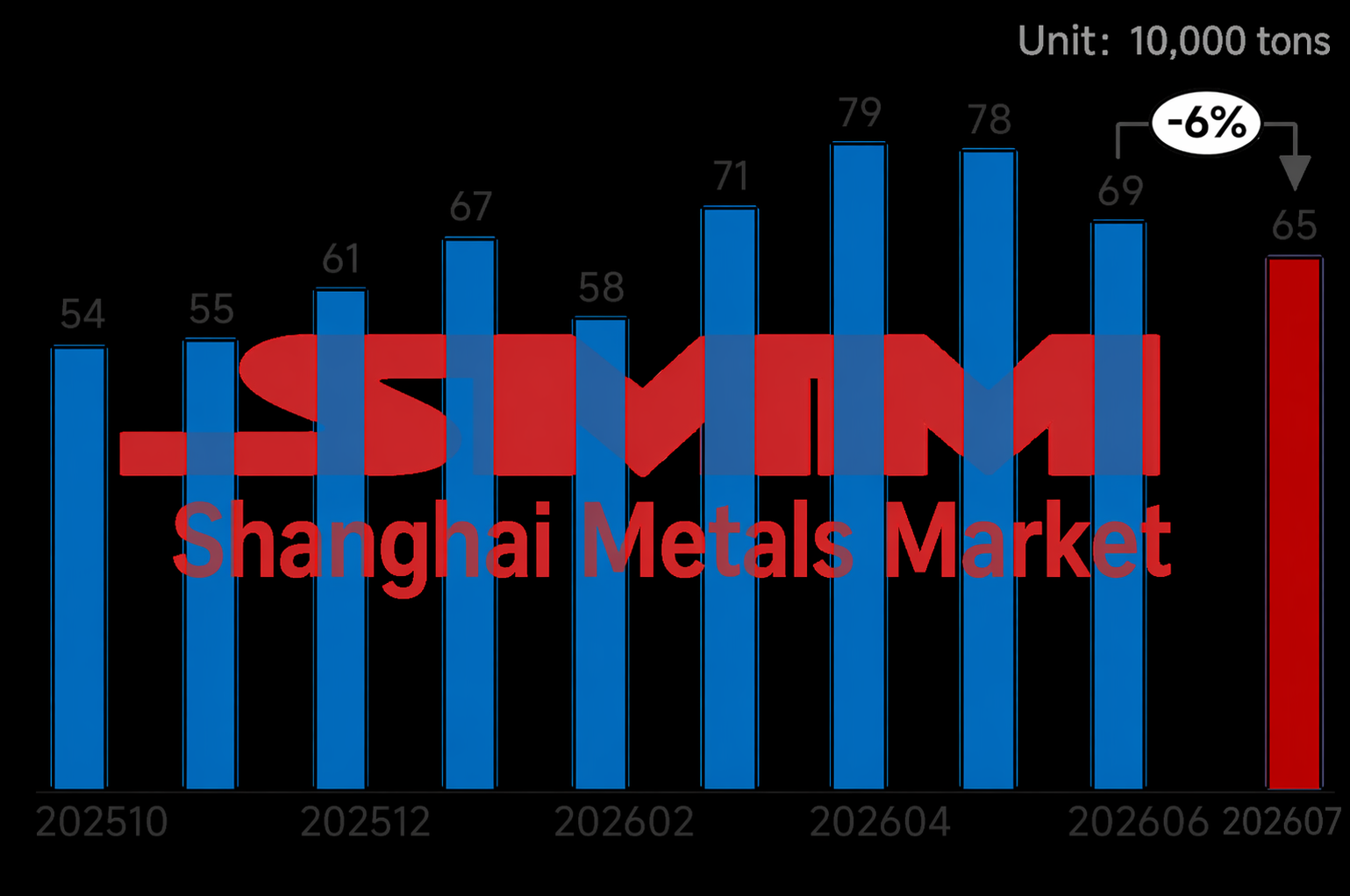

- In July, the export schedule for long products at sample mills was 653,000 mt, down 41,000 mt MoM, with the billet export schedule at 350,000 mt, down 30,000 mt MoM.

Specifically, the decline in July's long product export schedule was still mainly in billet, while order intake for rebar and wire rod edged down. Earlier, the Strait of Hormuz was navigable, and some Middle Eastern buyers adopted a wait-and-see attitude toward Chinese purchases. In addition, price advantages of neighboring countries improved, making Chinese export prices less competitive, which led to a decline in procurement volumes in the Southeast Asian market. By region, mills in the Northeast region, considering that the price advantage of billet exports declined and was inferior to domestic trade transactions, saw further reductions in order intake. Meanwhile, mills in East China had maintenance in July and controlled their July export order intake in advance.

Chart 3: Export Schedule of Long Products at Sample Steel Mills (Including Billet)

Source: SMM

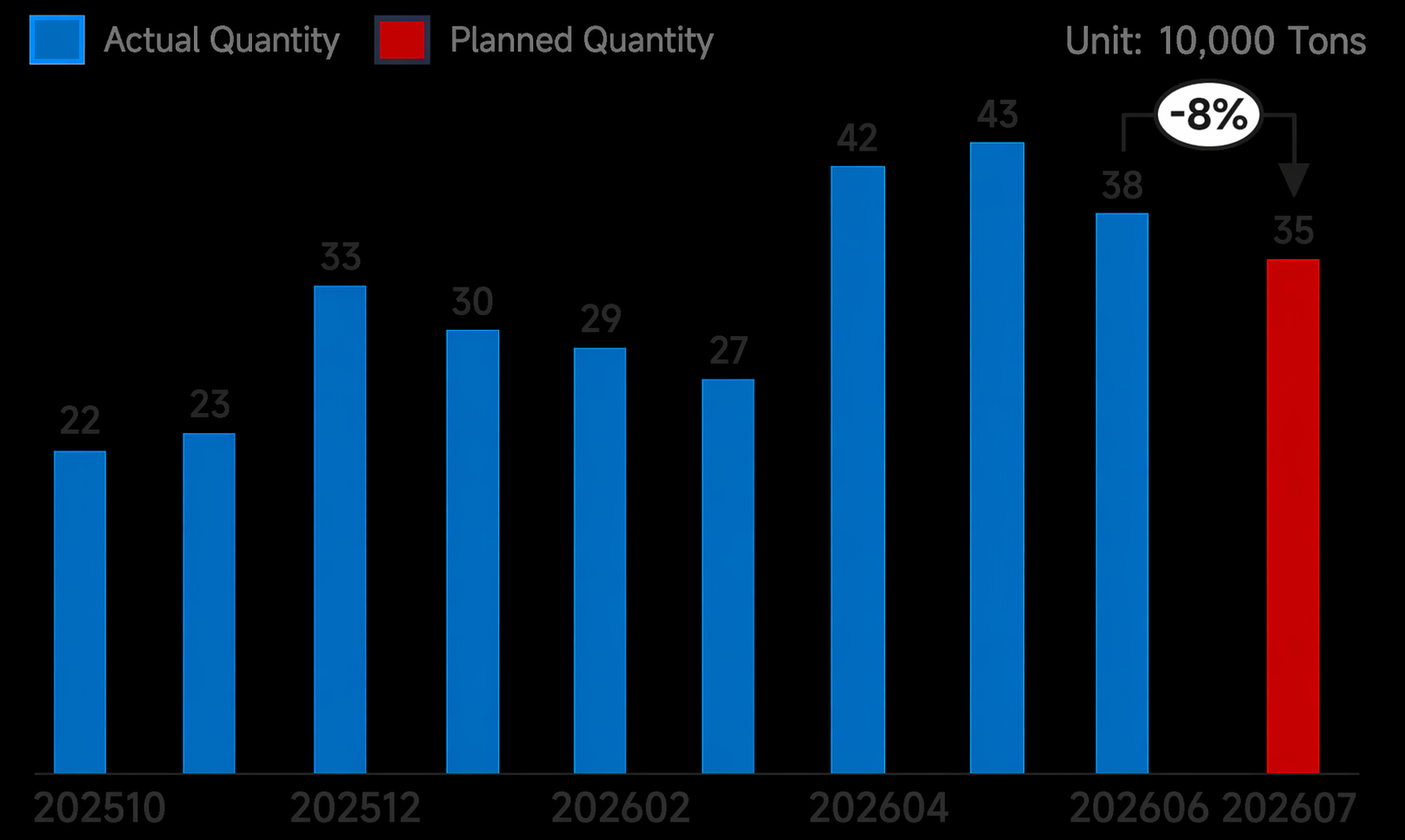

Chart 4: Billet Export Schedule at Sample Steel Mills

Source: SMM

By region:

Table 1: Rebar and Coiled Rebar Production Schedule - Last Month's Actuals and This Month's Plans

Source: SMM

Northeast: For some mills, pricing for overseas billet export orders was unfavorable, leading to a slight decline in export orders. Additionally, some hot metal was redirected to construction steel, but the total volume changed little.

North China: Current production profitability of steel mills is mostly around break-even levels, and they can still maintain previous production levels for the time being.

East China: Some mills in the region have maintenance plans for blast furnaces and rolling lines. Some mills plan to halve their July rebar production. In addition, for a few mills, profitability of sheets & plates is relatively better than that of construction steel, so some hot metal was shifted to increase sheets & plates output. As a result, overall construction steel production dropped notably.

Central & South China: Some steel mills face significant inventory pressure. Combined with rebar production being less profitable than specialty products, they plan maintenance or rebar production cuts in July.

Northwest: Many steel mills in the region were incurring losses, with some focusing mainly on hot-rolled coils or wide and thick plates, leading to a significant decline in rebar production, while the impact on wire rod output was relatively small.

Southwest: In July, individual mills underwent blast furnace maintenance, slightly affecting building material production. Additionally, as the region remained a national price trough, some mills reduced operating loads.

Cost side:

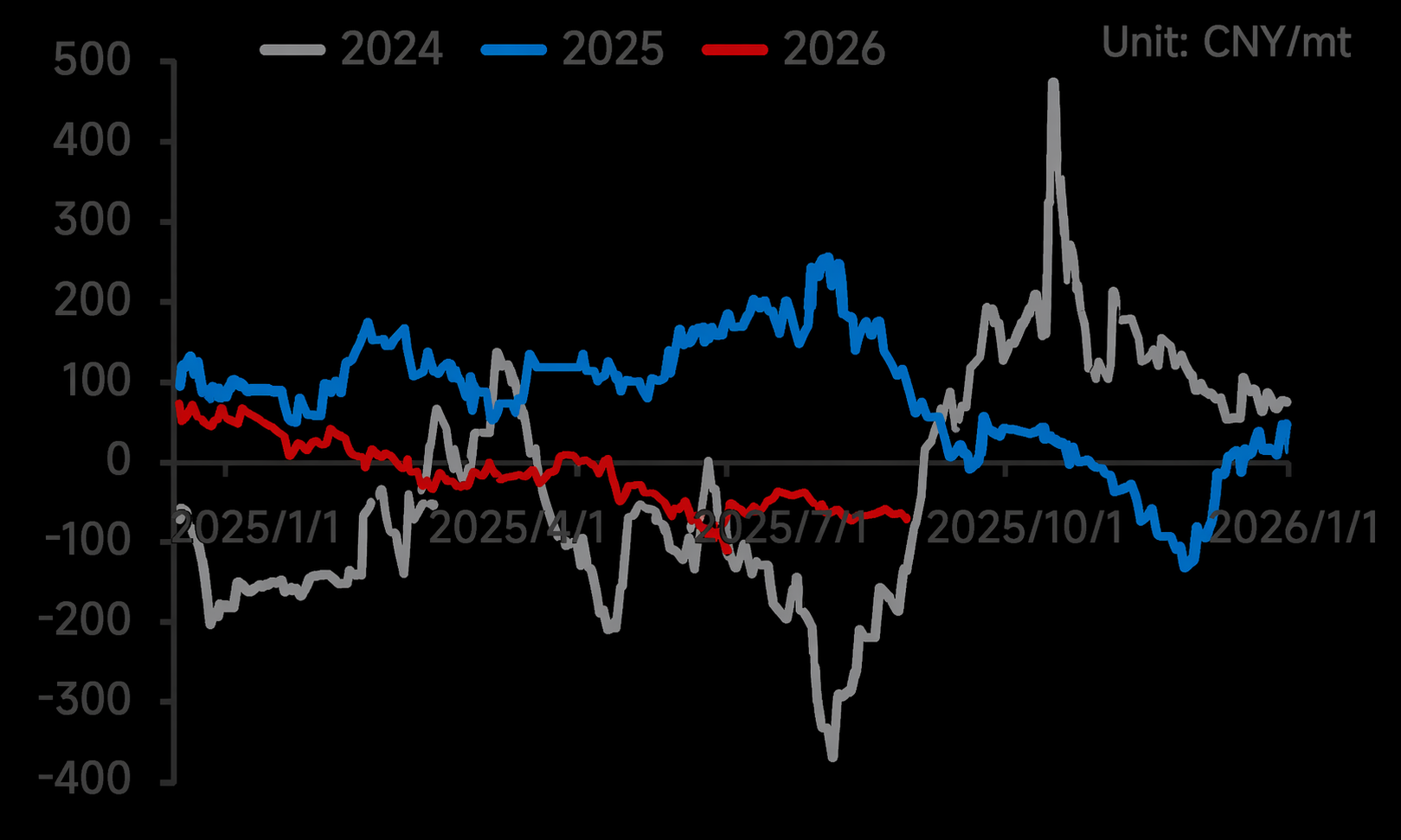

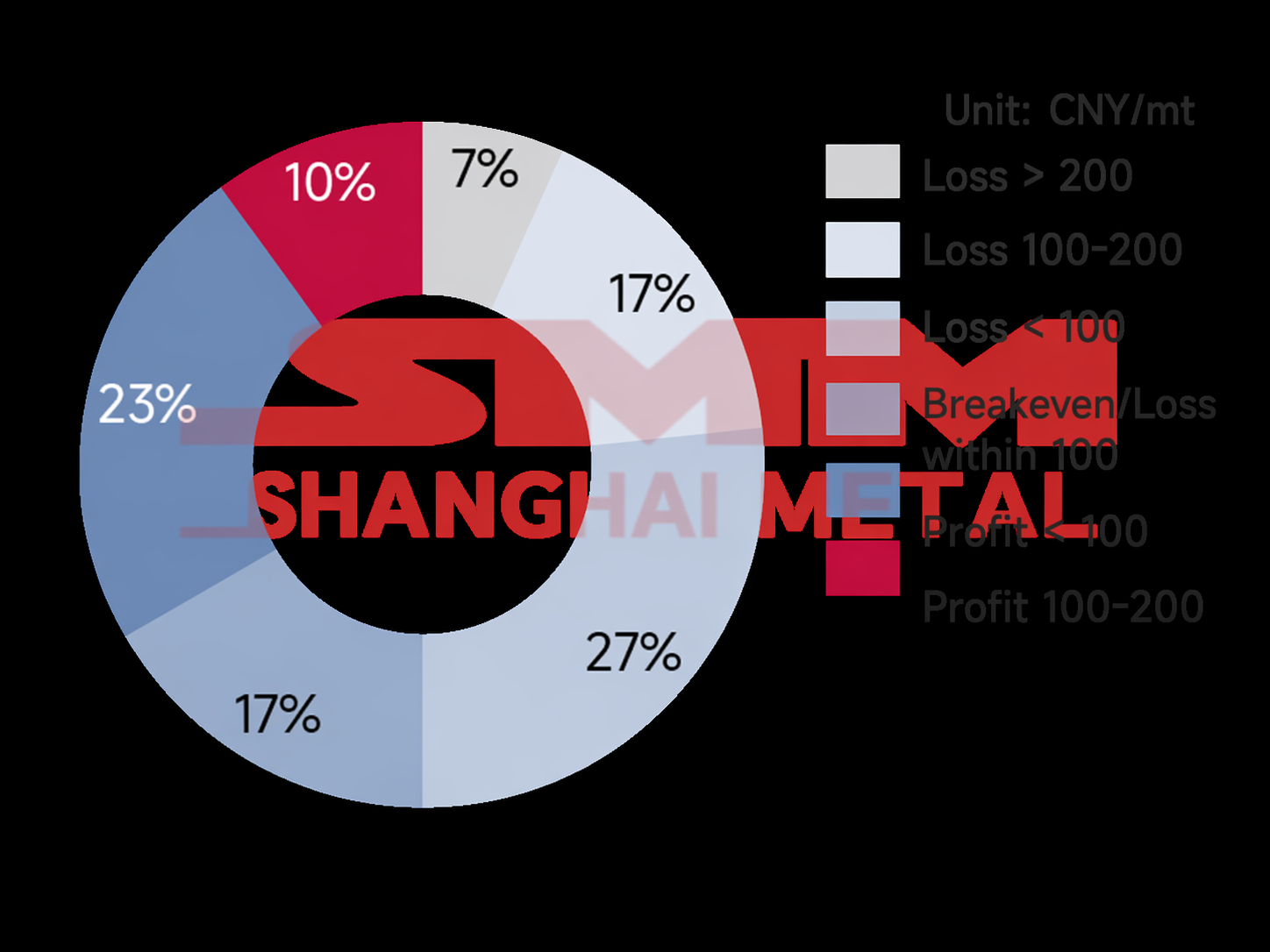

The 10th round of coke price increases was proposed. Although its implementation remained under negotiation, steel mills had already absorbed an additional 3-4 rounds of increases in June, continuously compressing finished product margins. Some enterprises were already at a loss-making stage, with the current mill profitability rate at 33.33%, a marked decline from June. The prevailing margin level now ranged from -200 to 100.

Chart-5: Real-Time Profit Trend of Rebar Production at Steel Mills, 2024 to Date

Source: SMM

Chart-6: Marginal Profitability of Rebar at Sample Steel Mills

Source: SMM

Outlook:

Recently, most steel mills have been operating around the break-even line, weakening production enthusiasm. In east China, south China, and the northwest, mills have scheduled maintenance or switched to other steel products due to poor rebar margins, resulting in a notable drop in planned rebar output for July. Meanwhile, wire rod margins were slightly better than rebar, and some mills had already reduced wire rod output to low levels earlier, producing on a monthly basis to replenish end-user standing demand. As a result, the decline in daily average wire rod production was less than that of rebar.

Overall, the seasonal demand off-season from July to August, combined with building material production generally starting to incur losses, is expected to lead to adjustments in steel mill production pace. Additionally, some mills have scheduled annual overhauls in August, making a later shift to increased building material output less likely. Therefore, production is expected to remain at low levels before profitability improves. However, to ensure direct supply volumes, the planned production cut for August is expected to be relatively small.

![[SMM Steel] 7.31 SMM Global Steel Daily Report](https://imgqn.smm.cn/usercenter/fvyjO20251217171715.jpg)

![Policy Expectations Fell Through, Compounded by Deepening Negative Feedback, Next Week May Continue to Consolidate at Lows [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/eEmCr20251217171746.jpg)