SMM, July 3:

I. Market Landscape

In H1 2026, a surge in downstream demand steadily boosted prosperity across the anode industry, markedly unleashing overall market vitality. In the EV sector, the NEV industry maintained a stable growth trajectory. Although the domestic sales market in China faced significant resistance, the export market achieved doubling growth. Meanwhile, considering the significant increase in vehicle battery capacity, coupled with policy dividends driving improved commercial vehicle sales, power battery cell demand continued to expand, providing solid demand-side support for the anode market. In the ESS sector, standalone ESS projects in China were driven by economic viability at the beginning of the year, combined with motivations to "meet deadlines" for grid connection, leading to a concentrated surge in tenders. In markets outside China, the European and Asia-Pacific markets saw significant volume growth driven by policy support. Driven by combined demand from in and outside China, ESS sector demand soared.

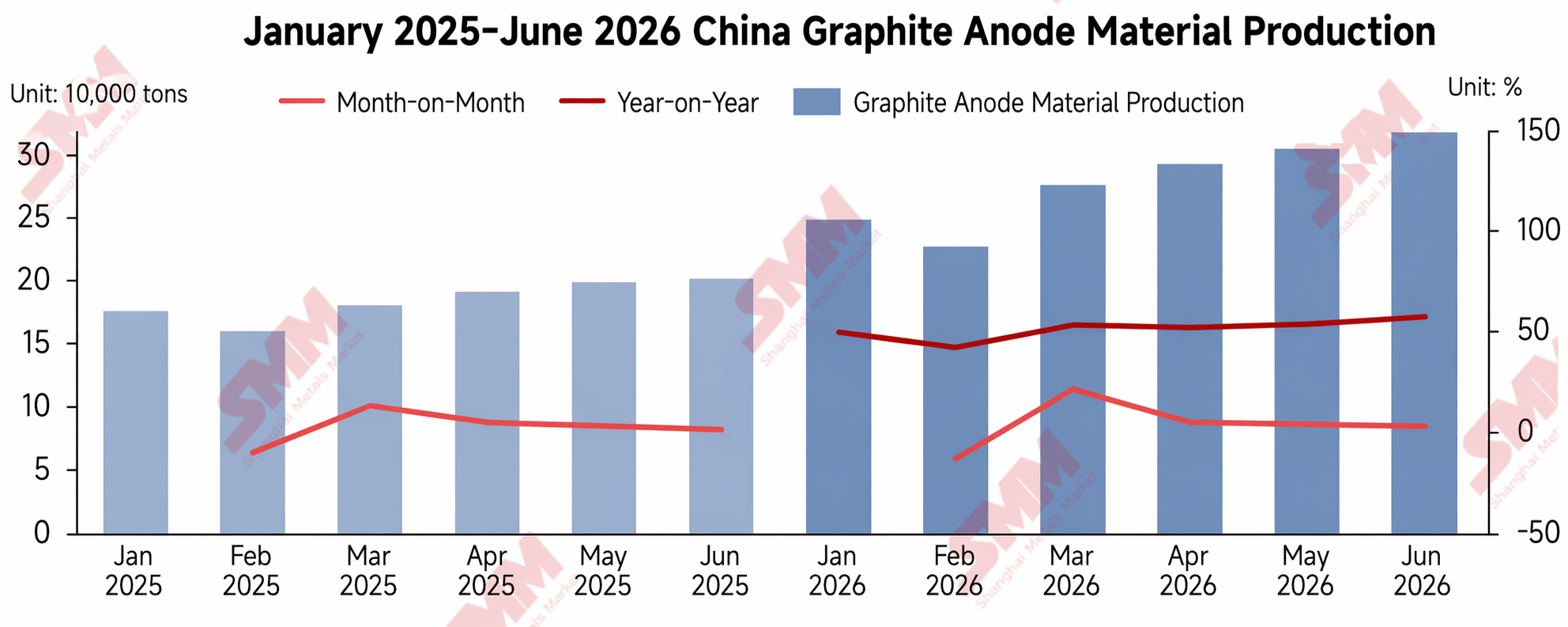

The two major sectors of NEV and ESS batteries empowered each other and exerted coordinated force, driving end-use demand in the anode industry to explode; overall graphite anode demand in H1 rose by over 68% YoY. Against this backdrop, major anode enterprises accelerated their production schedules. According to SMM statistics, in H1 2026, China's total production of graphite anode material reached approximately 1.69 million mt, an increase of over 52% compared to the same period in 2025. Among them, top-tier player BTR exhibited particularly outstanding production performance, solidifying its leading position.

As downstream demand continued to be released, overall shipments in the anode industry maintained rapid growth. According to SMM statistics, total industry shipments in H1 2026 rose by 64% YoY. However, constrained by persistently tight integrated capacity among first- and second-tier anode enterprises, the release of effective supply was limited. Hindered by lengthy product validation cycles, tail-end enterprises found it difficult to substantially fill the supply-demand gap in the short term; the industry thus exhibited a pattern of material supply shortage. Against this backdrop, industry inventory continued to destock through H1 2026, with destocking becoming the main theme and overall inventory levels pulling back significantly.

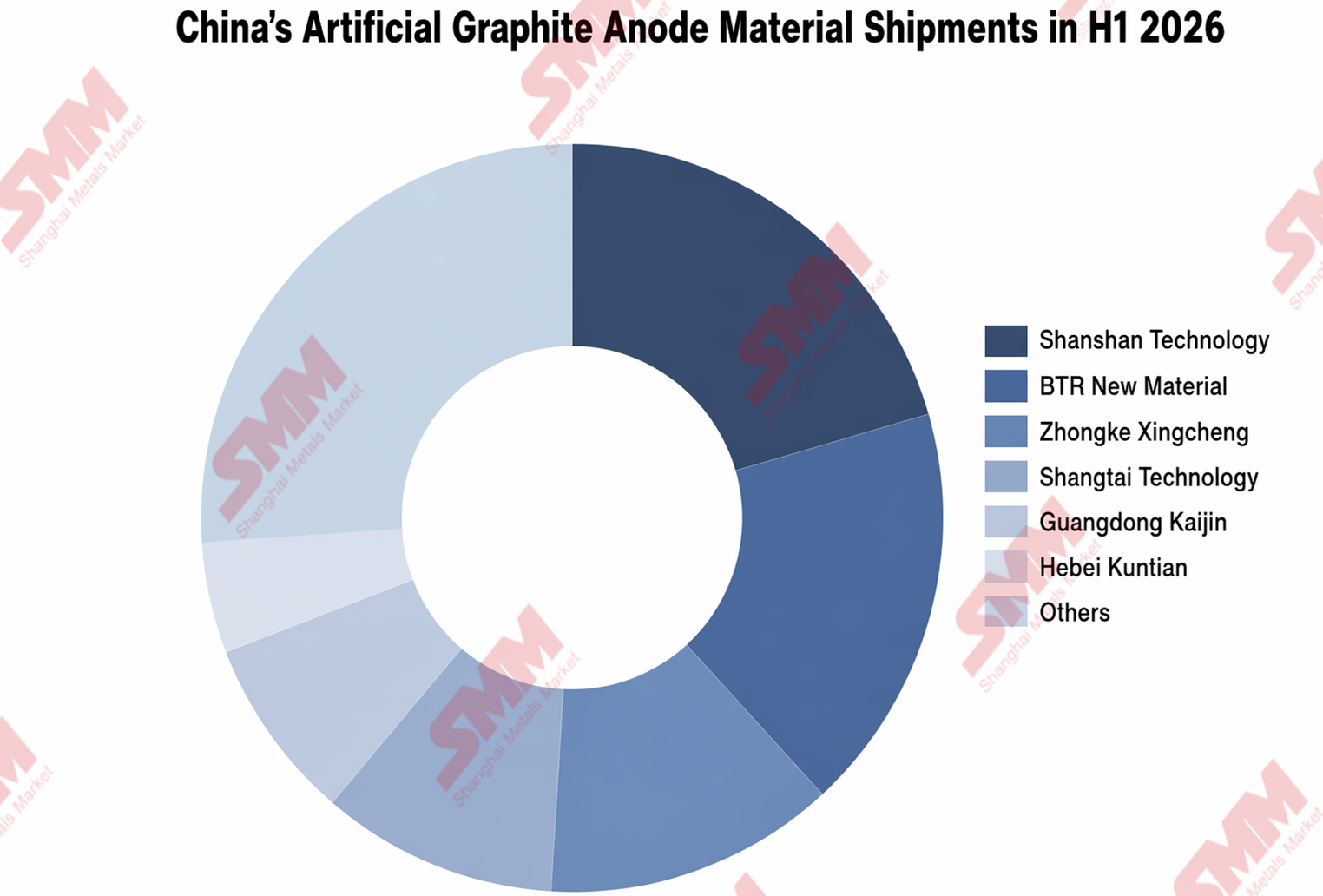

In terms of product structure, artificial graphite anode material, characterized by relatively abundant capacity deployment and notable comprehensive cost-performance advantages, saw continuously strengthening competitive resilience in the market. According to SMM statistics, China's artificial graphite anode material production rose by 56% YoY in H1 2026, with its market share in the graphite anode market climbing to 93%. In terms of corporate competitive landscape, Shanshan remained top in artificial graphite shipments with a 21% market share, further reinforcing its industry-dominant position.

II. Supply-Demand, Cost, and Price Trends

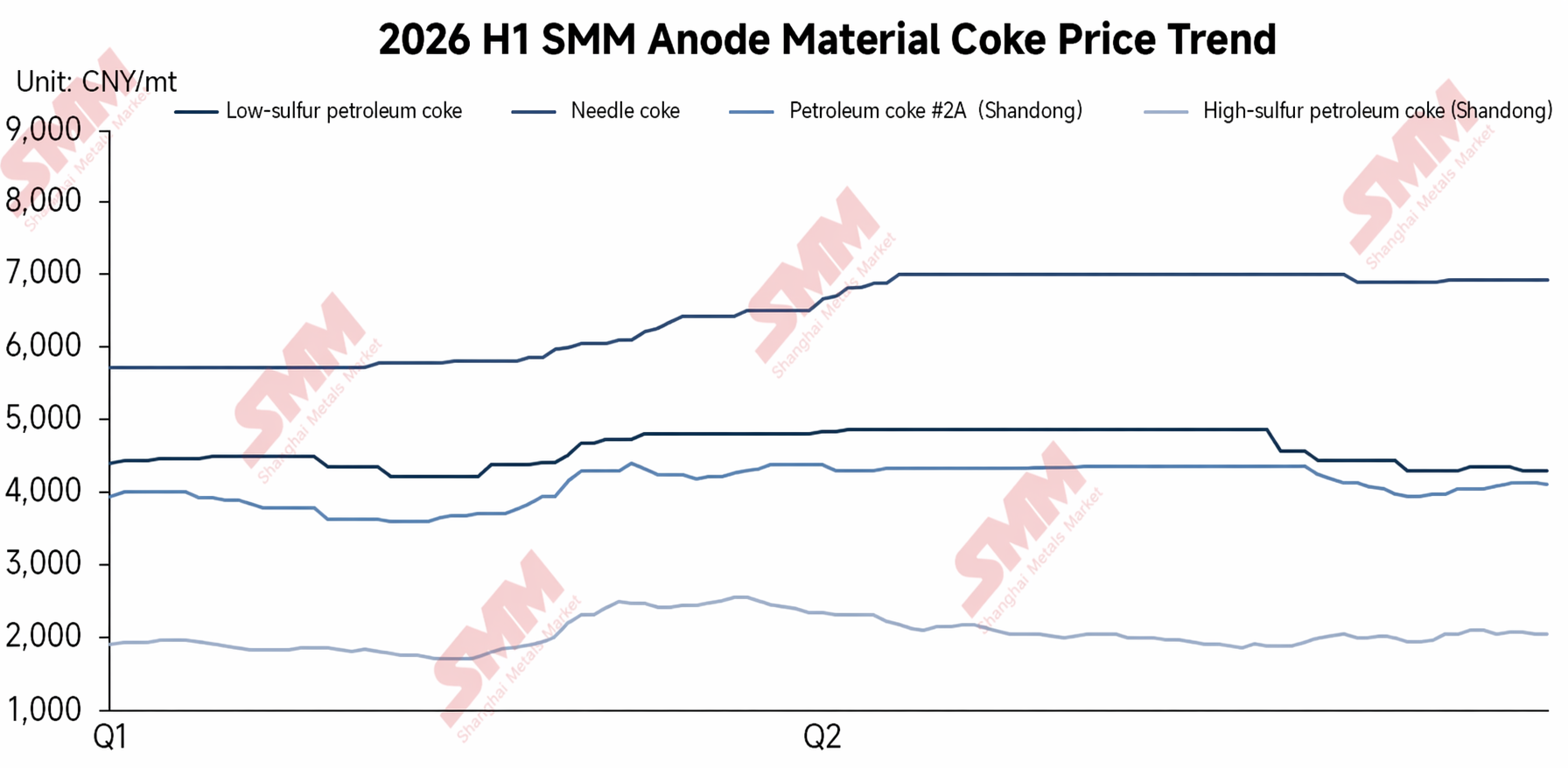

In Q1 2026, geopolitical conflicts drove up costs, and prices stagnated under a tight supply-demand balance. On the cost side, due to escalating geopolitical conflicts in the Middle East, disruptions to shipping through the Strait of Hormuz drove international oil prices sharply higher. Production costs for various raw material cokes rose significantly, leading to a broad-based price hike for raw material cokes. Simultaneously, graphitisation auxiliary material prices also rose, directly offsetting the price downtrend caused by overcapacity; graphitisation tolling service prices became mired in stalemate and negotiation. On the supply and demand side, against the backdrop of soaring costs, anode enterprises widely adopted a produce-based-on-sales model to hedge against cost pressure. Willingness to stockpile among anode enterprises remained weak, and industry inventory progressively decreased. Overall, the anode industry in Q1 maintained a tight supply-demand balance. Consequently, cost pressure continuously accumulated in Q1 2026, but due to production lag effects, price negotiations constrained price stability at quarter-end, and expectations for price hikes gradually built.

In Q2 2026, mounting cost pressure combined with ample orders allowed anode material prices to successfully rise. On the cost side, raw material coke prices for anodes continued to rise sharply since Q1, with industry production cost pressure persistently accumulating. On the supply and demand side, orders from downstream battery enterprises remained full, and self-owned integrated capacity among first- and second-tier anode enterprises was tight. Consensus on market price adjustments formed, allowing costs to be successfully passed downstream; landing price adjustments for anode materials were completed, and market bargaining power somewhat recovered.

Overall, the anode industry finally achieved a price increase in H1 2026 after multiple rounds of price negotiations between upstream and downstream players. However, this round of price rise stemmed mainly from the passive transmission of upstream costs, and the industry has yet to truly experience a full-fledged recovery. While industry prosperity indeed empowers and enhances the development of anode enterprises, it also leaves many topics worthy of deep cultivation: how to hedge against wild swings in raw material prices caused by geopolitical disruptions, how to rely on integrated capacity to strengthen bargaining power, and how to grasp the pace of price transmission along the industry chain to balance upstream and downstream interests… These are all subjects that enterprises must continuously refine for long-term development.

III. Outlook

Looking ahead to H2, on the supply and demand side, industry-end-use demand is expected to continue its release, driving steady increases in anode enterprise operating rates and production schedules. However, the tight effective supply situation will be difficult to quickly alleviate, and tight cargo supply will likely continue to support product prices. On the cost side, as the integrated capacity gap widens, demand for graphitisation tolling services will continue to climb. Graphitisation tolling fees are expected to rise; simultaneously, upstream raw materials—such as raw material cokes—also have room for price increases, which is expected to push up anode processing costs. In summary, supported by both tight supply-demand and rising costs, domestic anode material prices are expected to possess sustained upward momentum in H2, and overall development prosperity is poised for steady improvement.

SMM New Energy Research Team

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lv Yanlin 021-20707875

Zhou Zhicheng 021-51666711

Zhang Haohan 021-51666752

Wang Zihan 021-51666914

Wang Jie 021-51595902

Xu Yang 021-51666760

Xu Mengqi 021-20707868

Hu Xuejie 021-20707858

![DRC Policy Disrupted Market, Refined Cobalt Price Rose 2,000 Yuan, How Did Downstream Demand Perform? [Weekly Observation]](https://imgqn.smm.cn/usercenter/WgbTp20251217171727.jpg)