Core Data:

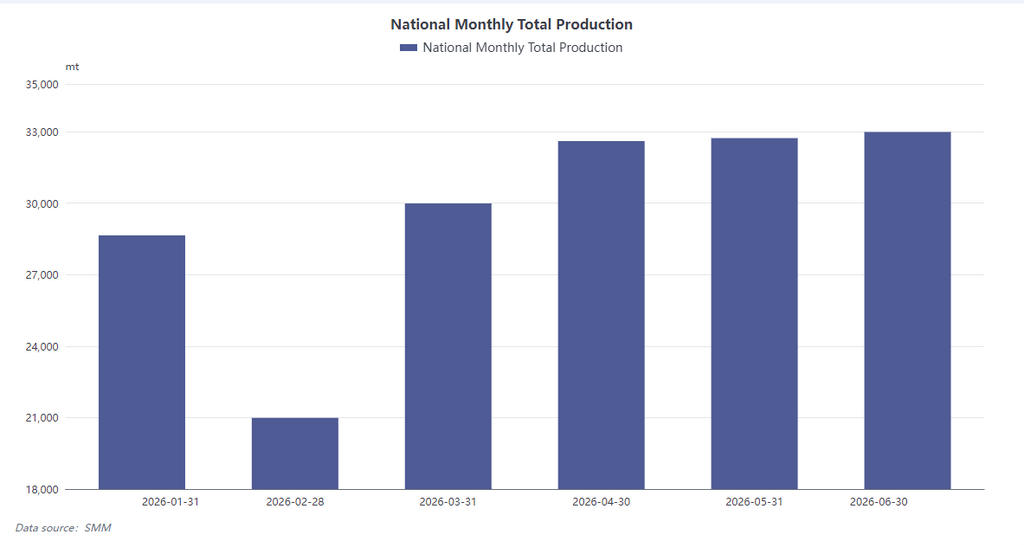

According to SMM research, China’s total sintered NdFeB blank production reached 32,985 metric tons in June 2026, up 11.2% YoY and 1.7% MoM. The industry-wide capacity utilization rate averaged 74.23%. However, this increase was not driven by fundamental demand recovery but rather by a surge in precautionary orders triggered by raw material price volatility. SMM estimates July output will pull back to approximately 31,731 metric tons.

June Review: Price Volatility Drives Order Pulse

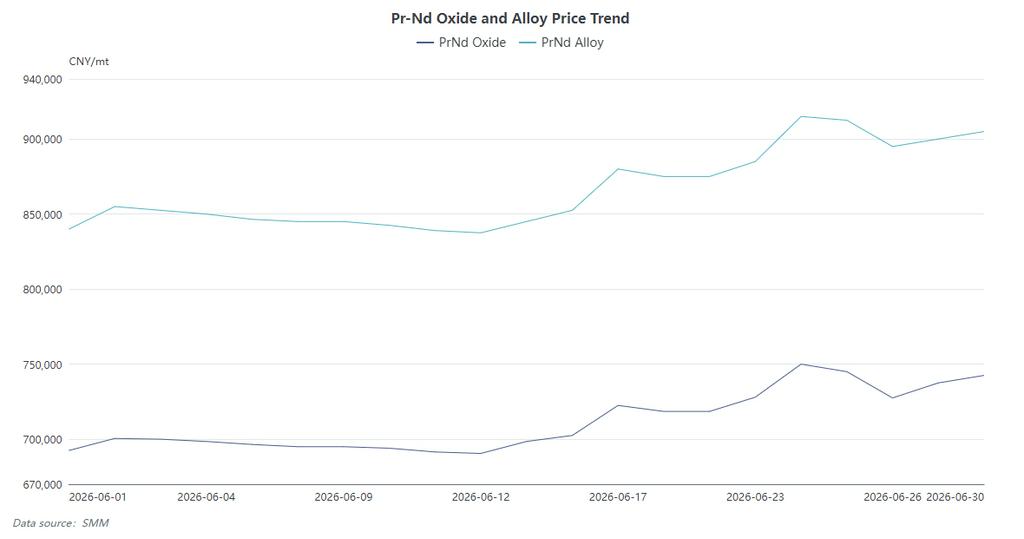

The market mirrored the sharp V-shaped rebound in Pr-Nd metal prices. Early-month price declines kept buyers on the sidelines. The trend reversed sharply in mid-June, culminating in a single-day jump of RMB 27,500/ton on the 17th. Under a cost-plus pricing model, this spike triggered urgent buying from downstream clients on a "case-by-case pricing" basis to hedge against further cost increases. This led to a significant short-term order influx, particularly for mid-sized producers. However, as prices peaked on June 24, "sticker shock" set in, causing end-users to slow their purchasing pace. Consequently, June’s output growth represents inventory shifting through the supply chain rather than genuine consumption growth.

July Outlook: Inventory Drawdown and Dual Headwinds

The support factors from June are fading, suggesting a return to fundamentals.

-

Domestic Demand: While NEV traction motor orders remain stable (anchoring large manufacturers), industrial servo motor demand faces uncertainty amid a tepid macroeconomic recovery. Additionally, the peak summer season typically sees slower wind power installations and scheduled maintenance in industrial sectors, constraining demand.

-

Export Risks: External demand faces policy uncertainties. Anticipating potential extensions to China's export licensing controls, some European and U.S. clients accelerated purchases in late June, effectively pulling forward Q3 demand. Ongoing complexities in international trade relations add further uncertainty to license approvals, potentially impacting export-oriented producers.

H2 Forecast: Subdued Stability with Inventory Risks

SMM analysis indicates that June’s stockpiling has essentially "front-loaded" future demand. In a global manufacturing environment lacking strong catalysts, speculative orders are unsustainable. The second half of the year will likely see adjusting pressures. With traditional sectors like consumer electronics and HVAC showing only modest recovery signs, overall apparent consumption is expected to remain subdued yet stable. Competition will shift from capacity expansion to cost control and client diversification. Producers are advised to monitor upstream rare earth policies and downstream inventory levels closely to mitigate the risk of overstocking.

![Spot Pr-Nd oxide posts two consecutive gains; rare earth permanent magnet concept strengthens; Zhong Ke San Huan, Dongfang Zirconium, and other stocks hit the daily upper limit [SMM Flash]](https://imgqn.smm.cn/usercenter/vpWKL20251217171743.jpeg)