SMM, June 23:

Metals market:

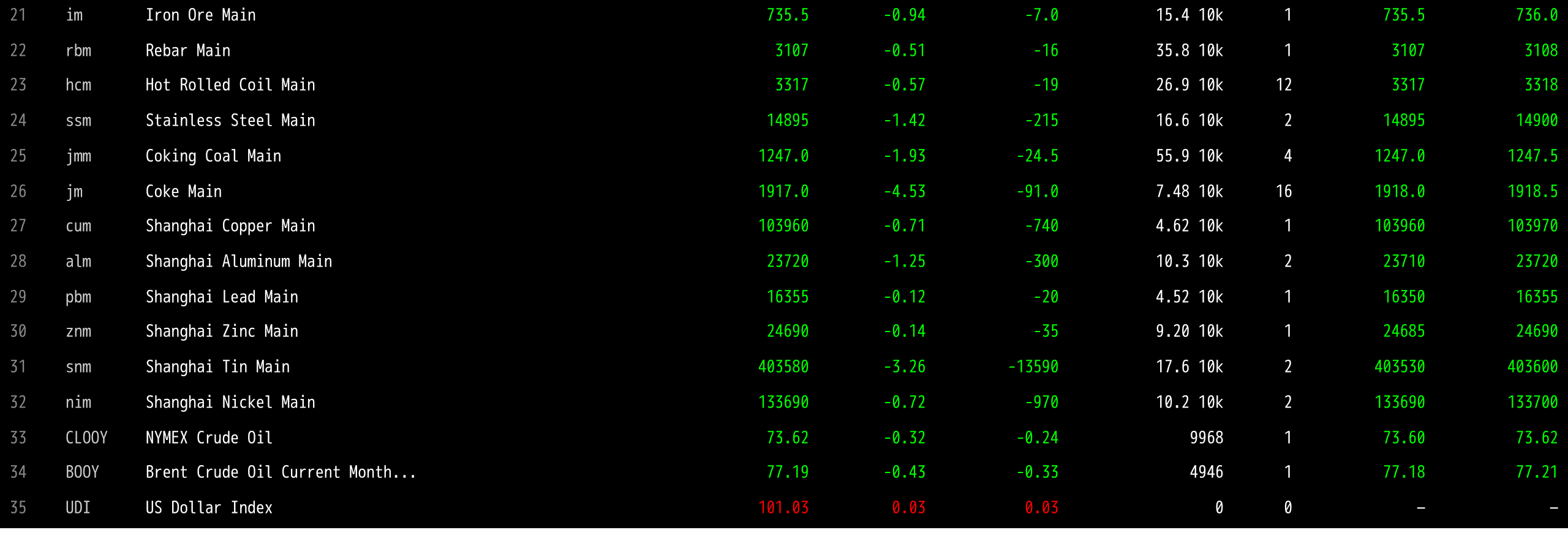

As of the midday close, base metals in the domestic market fell across the board, with SHFE copper down 0.71%, SHFE aluminum down 1.25%, SHFE lead down 0.12%, SHFE zinc down 0.14%, SHFE tin down 3.26%, and SHFE nickel down 0.72%.

In addition, the most-traded foundry aluminum futures contract fell 1.17%, the most-traded alumina contract fell 2.43%, the most-traded lithium carbonate contract fell 0.79%, the most-traded silicon metal contract fell 0.41%, and the most-traded polysilicon futures contract fell 0.56%.

Ferrous metals all fell, with iron ore down 0.94%, rebar down 0.51%, HRC down 0.57%, and stainless steel down 1.42%. Coking coal and coke: the most-traded coking coal contract fell 1.93%, and the most-traded coke contract fell 4.53%.

In the overseas base metals market, as of 11:43, LME metals trended lower across the board, with LME copper down 0.89%, LME aluminum down 1.56%, LME lead down 0.84%, and LME zinc, LME tin, and LME nickel all down nearly 1%.

In precious metals, as of 11:43, COMEX gold fell 1.07% and COMEX silver fell 3.78%. In the domestic precious metals market: the most-traded SHFE gold contract fell 1.36%, and the most-traded SHFE silver contract fell 4.91%.

Additionally, as of the midday close, the most-traded platinum futures contract fell 2.85%, and the most-traded palladium futures contract fell 2.36%.

As of the midday close, the most-traded containerized freight index (Europe) futures contract fell 2.23% to 3,689 points.

As of 11:43 on June 23, selected futures midday market quotes:

Spot Market and Fundamentals

Zinc: Today, mainstream transaction prices for #0 zinc were concentrated at 24,585–24,770 yuan/mt, mainstream transaction prices for Shuangyan were at 24,685–24,860 yuan/mt, and mainstream transaction prices for #1 zinc were at 24,515–24,700 yuan/mt. In the morning session, offers against the SMM average price stood at a premium of 10–20 yuan/mt, with no quotes against the contract...

Macro Front

Domestically:

[Draft Financial Law Submitted to the NPC Standing Committee for First Review] On June 23, 2026, the Financial Law of the People's Republic of China (Draft) was submitted to the 23rd Session of the Standing Committee of the 14th National People’s Congress for its first review. The Financial Law is China's foundational, comprehensive, and overarching law governing the financial sector, positioned as the "1" in the financial legal framework, serving a guiding, commanding, and normative role. Sectoral laws in banking, insurance, securities, and other fields—the "N"—along with other financial regulations and rules—the "X"—must align with the fundamental provisions established by the "1," with equal emphasis on enactment and revision, to specifically regulate financial activities in their respective areas. Together, the "1+N+X" structure forms a scientifically complete and unified financial legal system. The draft financial law adheres to the main theme of strengthening regulation, preventing risks, and promoting high-quality development, focusing on coordinating development and security, and striving to resolve legal hurdles constraining high-quality financial development. (Xinhua)

[PBOC reverse repos net injection of 75 billion yuan today] The PBOC conducted 524.5 billion yuan of 7-day reverse repo operations today at an interest rate of 1.4%, unchanged from before. Today, 449.5 billion yuan of reverse repos matured.

On the US dollar:

As of 11:43, the US dollar index rose 0.03% to 101.03. According to CME "FedWatch," the probability of the Fed keeping rates unchanged in July is 63.7%, and the probability of a cumulative 25-basis-point rate hike is 36.3%. By September, the probability of the Fed keeping rates unchanged is 26.1%, the probability of a cumulative 25-bp hike is 52.2%, and the probability of a cumulative 50-bp hike is 21.4%. (Jin10 Data APP)

Citadel Securities said that Fed Chairman Warsh's commitment to reducing inflation has enhanced the Fed's credibility, thereby supporting US long-term Treasury yields and suppressing term premiums. Following last week's Fed meeting, trading in the $31 trillion US Treasury market exhibited a pattern: long-term yields were more stable than the more policy-sensitive two-year yield. Nohshad Shah, the firm's head of fixed income sales, said, "A highly credible Fed should benefit long-end rates." (Jin10 Data APP)

Bank of America currently expects the Fed to raise rates three times this year, the latest sign that Wall Street is bracing for more aggressive Fed hikes. The bank's economists had previously expected the Fed to keep rates unchanged this year. The revision was driven by strong economic data and a hawkish shift in the Fed's communications, signaling a more proactive approach to combating inflation. Bank of America's forecast of three rate hikes remains a minority view: currently, only 19% of market investors expect three hikes, though this is up from 3% a week ago. Investors see two hikes as the most likely outcome.

On other currencies:

Following further yen weakening and reports of an online meeting between Japanese Finance Minister Satsuki Katayama and US Treasury Secretary Bessent, foreign exchange traders are on high alert for possible intervention. In early Tuesday trading, the yen was around 161.57 per dollar, near a 40-year low. NHK and Kyodo News reported that Kataoka and Bessent may have discussed exchange rates. Market concerns persist that the Bank of Japan, after raising rates at last week’s policy meeting, has not hiked borrowing costs quickly enough to curb inflation, keeping the yen under pressure. Additionally, oil prices elevated by the US-Iran war have imposed an extra drag on the yen. Takeru Yamamoto, a trader at Sumitomo Mitsui Trust Bank in New York, said: "Japanese authorities may hope to use the US-Japan meeting to signal that they are coordinating actions with the US, while hinting that the threshold for intervention is not high. Although market concerns over intervention have increased, the fundamentals behind the yen's weakness remain unchanged. USD/JPY could test the 162 level this week." (Jin10 Data APP)

On the data front:

Today's releases include the preliminary French June manufacturing PMI, preliminary German June manufacturing PMI, preliminary Eurozone June manufacturing PMI, preliminary UK June manufacturing PMI, preliminary UK June services PMI, UK June CBI industrial order balance, US ADP employment change for the week ending June 6, preliminary US June S&P Global manufacturing PMI, preliminary US June S&P Global services PMI, and the US June Richmond Fed manufacturing index. Also of note: Bank of Canada Governor Macklem delivers a speech; the 17th Summer Davos Forum takes place in Dalian, June 23–25; MSCI announces its annual market classification review, with South Korea likely to enter the watchlist for developed market status.

In crude oil:

As of 11:43, both benchmarks edged down, with WTI losing 0.32% and Brent falling 0.43%. Oil prices stabilized as the market weighed early progress in the Iran war peace negotiations, including the US allowing some Iranian crude sales. A 60-day US license allows Iran to sell a portion of its oil and petroleum products. Rebecca Babin, Managing Director and Senior Energy Trader at CIBC Private Wealth Management, said: "The road to negotiations remains long, yet the market is likely to price in a crude surplus before one actually materializes, just as it priced in a supply deficit before it truly happened. Oil prices frequently overshoot." (Jin10 Data APP)

Danske Bank forecasts Brent crude will average $80 per barrel for the remainder of 2026, rising to $85 per barrel next year. The bank also stated that even if a US-Iran deal is reached, oil prices will not return to the pre-war level of $60–70 per barrel. The institution noted that a US-Iran agreement would reopen oil shipments through the Strait of Hormuz, but cautioned that it would take months for Iranian oil production and exports to return to normal levels. The bank noted that the continuous release of strategic petroleum reserves by the US may affect the near-term supply landscape, and indicated that the US may choose to maintain this policy before the November midterm elections for political reasons. (Jin10 Data APP)

Spot Market at a Glance:

►

►

►

►

►

►

►

►

![Market Bottom Solidifies, Major Players Bid Up Prices for Market Making [SMM South China Spot Aluminum Daily Review]](https://imgqn.smm.cn/usercenter/TFHUe20251217171651.jpg)

![Futures pulled back, prompting end-user restocking, while buying and selling sentiment recovered and discounts held steady [SMM North China spot copper]](https://imgqn.smm.cn/usercenter/OsOmo20251217171709.jpg)

![Macro and Fundamental Bullish and Bearish Factors Coexist, Lead Prices Expected to Consolidate [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/lIHfM20251217171721.jpeg)