China's stainless steel futures swung in a wide range over the week of June 15–19, 2026, driven almost entirely by shifting overseas macro expectations, according to SMM data. The board rallied early and then faded, with the bull-bear contest intensifying. The most-traded August contract (SS2608) on the Shanghai Futures Exchange (SHFE) closed June 19 at RMB 15,060/mt (≈ $2,199), up RMB 355 (≈ $52) on the week and recovering most of its earlier losses.

The week's defining feature was a macro-led market with a sharp futures-spot divergence. Futures were wholly driven by overseas sentiment and traded erratically, while spot edged higher with contained volatility, supported by marginally tighter supply and firm mill pricing.

Macro: a violent swing in Fed expectations set the whole rhythm

Overseas monetary policy expectations whipsawed, and sentiment ran up early before turning down. At the start of the week, a de-escalation in US-Iran geopolitical tension combined with a soft US core CPI print lifted expectations of cooling inflation, sending the broader base metals complex higher and pulling stainless futures up with it. But mid-week the Federal Reserve held rates for a fourth straight meeting while dropping language that had hinted at further cuts; with nine officials on the dot plot now projecting a hike this year, the signal was distinctly hawkish. Markets moved to price roughly 38 basis points of tightening before year-end, the macro tailwind faded fast, risk-off sentiment picked up, and stainless futures pulled back.

Domestically, the recovery in internal demand remained limited: May industrial value-added rose 4.5% year-on-year, while retail sales grew just 1.4% cumulatively over January–May, with the single-month retail figure on the soft side. Liquidity stayed reasonably ample — M2 was flat, M1 recovered, and aggregate social financing in the first five months reached RMB 17.48 trillion (≈ $2.55 trillion) — but the direct lift to the board was limited. On balance, the week's tempo was set almost entirely by overseas rate-hike expectations, which amplified the wide swings.

Fundamentals: inventory steady, spot trade hostage to board sentiment

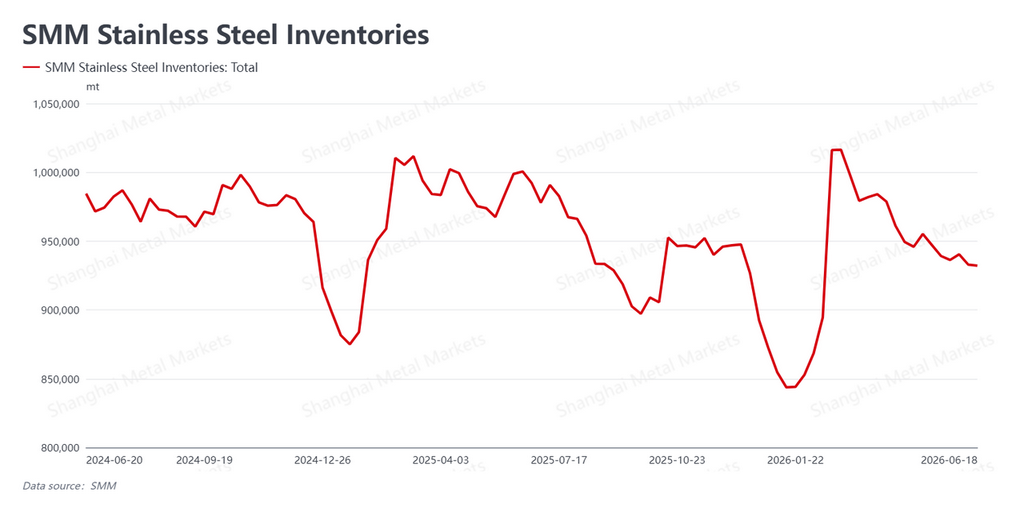

Distributor (social) inventory held steady, and spot transactions tracked the board closely. Stainless distributor inventory came in at 932,200 mt, down a marginal 700 mt on the week and essentially flat. With no accumulation despite the seasonal lull, inventory provided a degree of floor support for spot.

Spot trade moved in tight lockstep with futures, with clear phase-to-phase divergence: the early-week rally prompted concentrated end-user restocking and a notable pickup in volume, while the mid-week pullback brought renewed caution and a quick fade in transactions. End-user purchasing followed board sentiment entirely, and the off-season trend of weakening, less-resilient demand was unchanged. Even so, firm mill pricing and a marginal supply contraction kept spot prices edging higher with limited volatility — they did not weaken in step with futures, leaving the futures-spot split pronounced.

(For overseas readers: distributor inventory, known in China as "social inventory," is stock held across the trading channel rather than at mills.)

Cost and supply: raw materials split, mill margins recover slightly

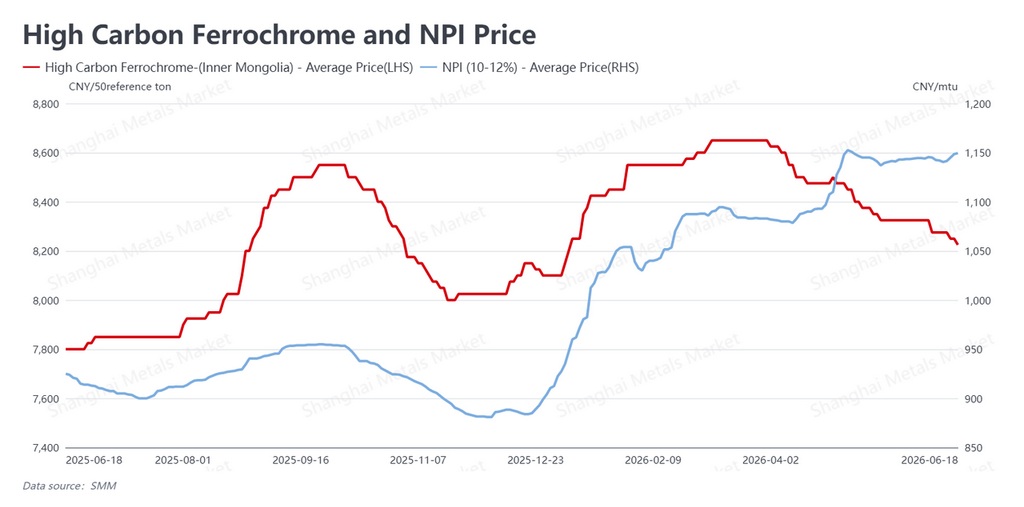

On the cost side, raw material prices diverged structurally. High-grade Nickel Pig Iron (NPI) was quoted at RMB 1,149.5/nickel unit (≈ $168), up RMB 9 (≈ $1.3) on the week, with trading more active and prices firming. High-carbon ferrochrome was quoted at RMB 8,225/mt on a 50% Cr basis (≈ $1,201), down RMB 50 (≈ $7) and still soft, while stainless scrap held steady. With nickel iron strengthening and ferrochrome weakening, overall cost movement was mild.

On supply, in-month maintenance cuts took effect and some mills delayed restarts, tightening industry supply at the margin — a meaningful support for spot that underpinned its small move higher. A modest rise in finished-product prices effectively offset some of the raw-material pressure, nudging mill margins wider; but even after that recovery, margins remain ample enough to sustain the incentive to produce, so the industry's overall high-supply structure is fundamentally unchanged. Over the medium term, loose supply remains the constraint on any upward shift in the price center of gravity.

Outlook

On balance, the stainless board swung widely this week on the back-and-forth in overseas macro expectations, while tighter supply and recovering margins supported spot resilience, with the futures-spot divergence in sharp relief. Looking ahead, the Fed's hawkish turn and the building of rate-hike expectations before year-end will continue to dominate commodity valuations and the board's tempo — the single biggest external variable near-term. With China now in its seasonal demand lull, end-user trade is entirely sentiment-driven and demand resilience is weak, so whether spot can stay steady hinges on the durability of mill price support and supply contraction. The structural split in raw materials and the modest margin recovery offer some support to production, but the high-supply backdrop is intact.

The most-traded contract is expected to stay in a wide range near-term, its center of gravity swinging with macro sentiment, while spot holds relatively steady on supply support. Industry participants would be well served to view the macro noise rationally, keep a close watch on Fed policy expectations, the durability of downstream transactions, and the progress of mill maintenance and restarts, and maintain a steady operating stance.

Written by Bruce Chew

Nickel & Stainless Steel Analyst, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088

![[SMM Analysis] Downstream Purchase Willingness Weak; Intermediate Product Payables in the Doldrums This Week](https://imgqn.smm.cn/usercenter/NHXhQ20251217171733.jpg)