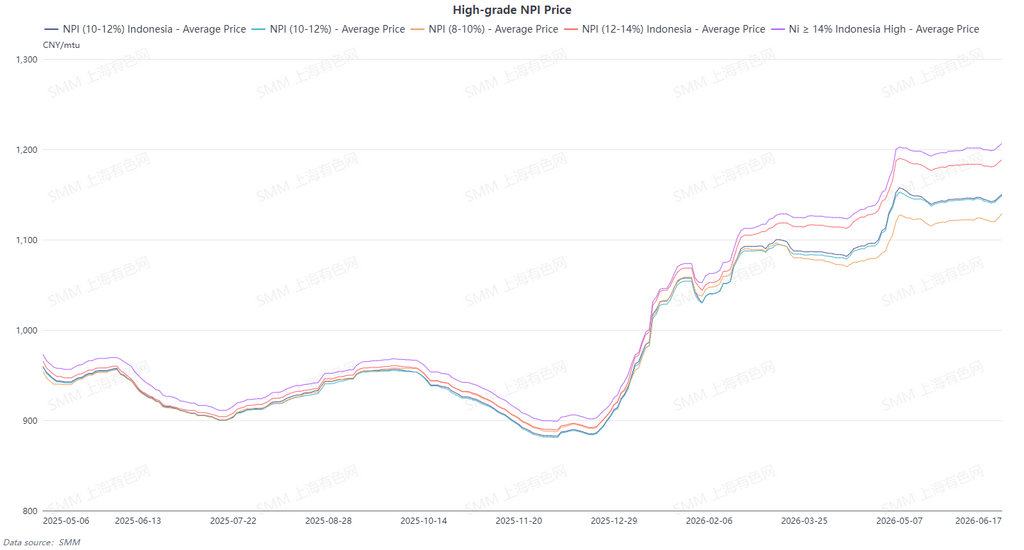

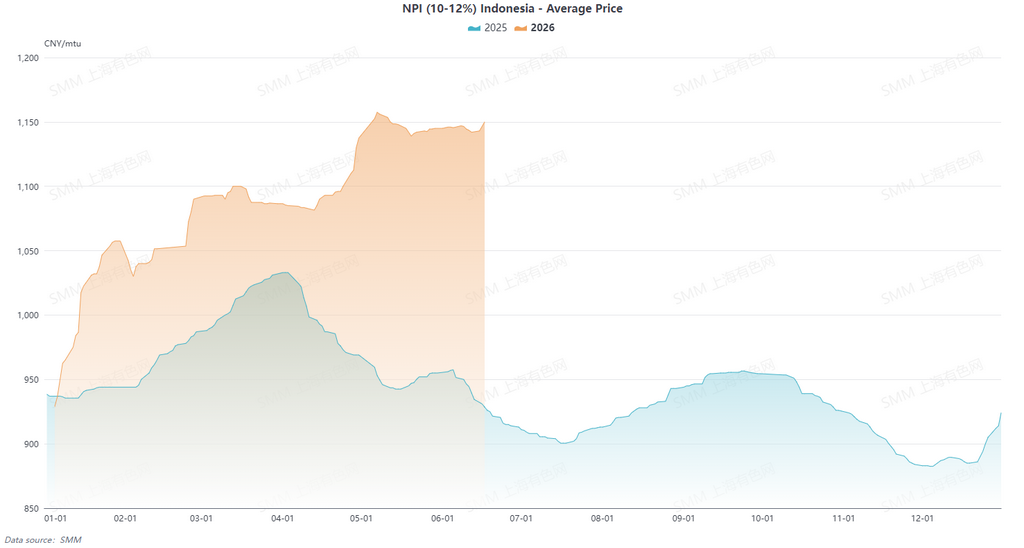

In H1 2026, the Indonesian 10-12% high-grade NPI (delivered to port, tax inclusive) market trended steadily upward, with the SMM average price rising 12% compared to the same period in 2025. Price movements were characterized by “stepwise increases and fluctuations at highs.” Each round of supply-demand imbalance and policy disruption pushed prices onto a higher level.

At the beginning of the year, the market remained weighed by expectations of ample supply from late 2025, and prices hit the H1 low on January 5. Subsequently, as news of tightening Indonesian nickel ore quotas escalated, combined with the release of restocking demand from steel mills in China before the Chinese New Year, a tightness in spot supply began to emerge, sending prices surging rapidly. At end-January, prices closed at 1,057.5 yuan per nickel unit, logging a monthly gain of more than 13%. After the Chinese New Year, the market shifted into a phase driven by both policy and cost factors. Tight Indonesian nickel ore supply and declining feed grades resulted in lower-than-expected effective nickel output from high-grade NPI, causing supply contraction expectations to keep building. Production costs for high-grade NPI also gradually rose, pushing prices to break through the 1,100 yuan per nickel unit mark in March.

April became a key turning point as Indonesia's new HPM policy was officially implemented, smelting cost expectations surged sharply, and coupled with persistent shortages of spot circulating cargoes, bullish sentiment peaked. On May 7, prices reached the H1 high of 1,157.5 yuan/nickel unit, a cumulative increase of 24.6% from the early-year low. Entering mid-to-late May, upward price momentum marginally weakened. Refined nickel futures weakened, stainless steel margins narrowed, and steel mills showed insufficient willingness to accept high-priced raw materials, intensifying the tug-of-war between buyers and sellers. The market exhibited a pattern of "firm prices but sluggish transactions," with prices slightly retreating to move sideways within the 1,130-1,150 yuan/nickel unit range. As of early June, SMM 10-12% high-grade NPI (delivered duty-paid) still showed a 23% increase from the early-year low, the upward shift of the H1 price center was clearly established, and the tight supply-demand balance and strong cost support formed a solid floor for prices.

I. Supply-Demand Pattern: Global Supply Contraction Intensifies, Domestic Phased Recovery Fails to Alter Tight Balance

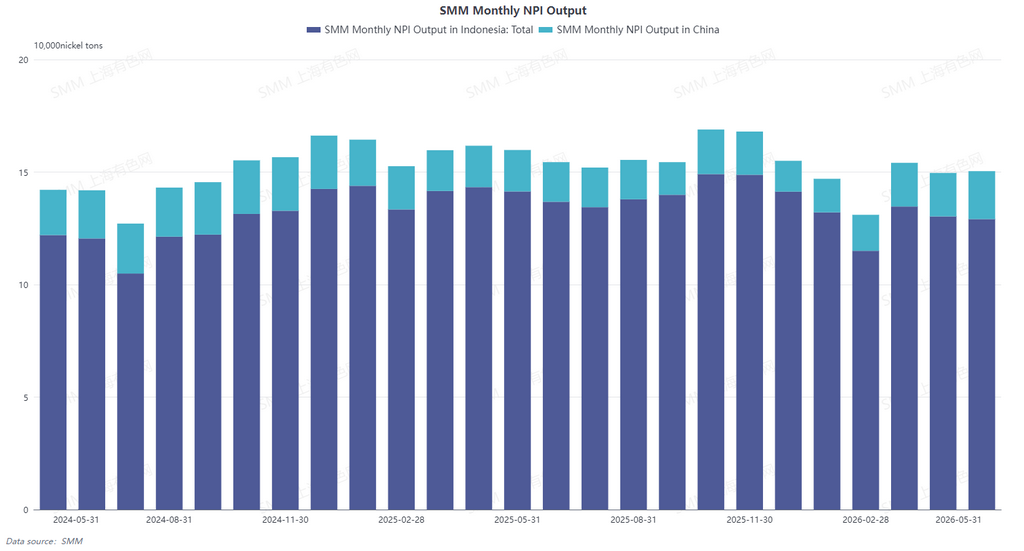

1. Indonesia: Output Continues to Contract Under Multiple Constraints

Indonesia's high-grade NPI production was constrained by multiple factors, showing a sustained contraction in H1. The tightening of nickel ore quotas, declining feed grades, increased difficulty for smelters in procuring raw materials, and rising unit consumption led to higher costs and raw material procurement issues, curbing high-grade NPI output. Even as new capacity ramps up, the increase could not offset the decline. Meanwhile, starting June, the commissioning of new aluminum capacity has been continuously squeezing electricity resources, prompting production cuts and maintenance at some NPI lines. Production is expected to come under further pressure, reinforcing expectations of supply contraction. In 2026, Indonesia's high-grade NPI production is expected to decline YoY.

2. Domestic Side: Profit Recovery Drives a Phased Rebound in Production

Unlike Indonesia, China's high-grade NPI production achieved a phased rebound driven by profit recovery. The core driver was declining costs on the raw material side: the recovery of Philippine nickel ore supply has sent prices into a sustained pullback, significantly lowering raw material costs for Chinese smelters. Coupled with high-grade NPI prices fluctuating at highs, smelting margins have gradually recovered, turning some previously loss-making lines profitable and prompting production capacities that had cut output to resume operations successively. However, the overall increase remains limited and is still insufficient to alter expectations of a supply deficit in 2026.

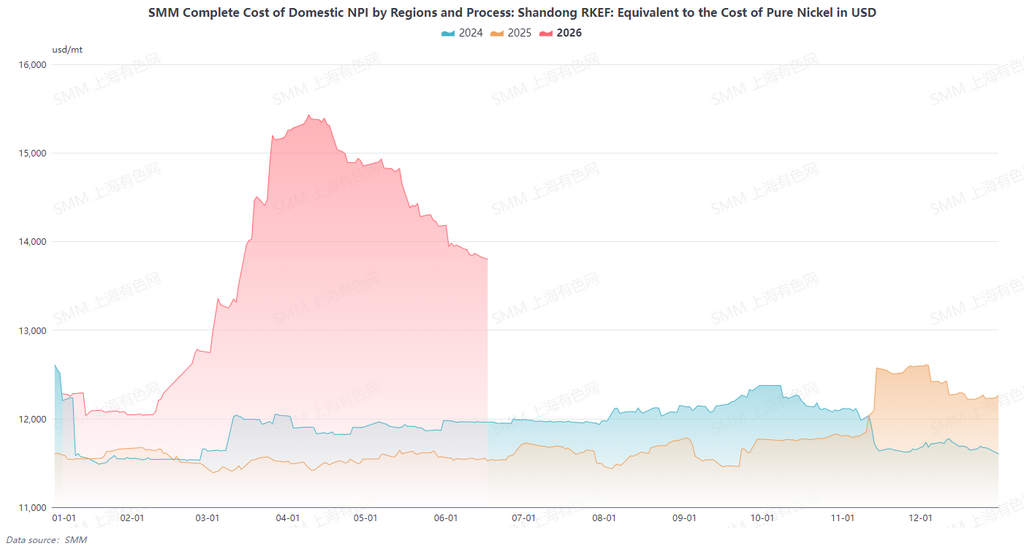

Ⅱ. Costs and Profitability: Divergence Between Domestic and International Curves, China's Profitability Surpasses Indonesia's

The cost-side trends diverged in and outside China, leading to a reversal in the profitability landscape. The recovery of nickel ore supply in the Philippines drove a pullback in prices, causing raw material costs for Chinese smelters to decline. As a result, profits gradually recovered, and some production lines turned from losses to profits. Meanwhile, nickel ore prices in Indonesia fluctuated at highs, compounded by declining grades, which pushed unit consumption and raw material costs up rigidly. Auxiliary material and electricity costs also increased, intensifying cost pressure on smelters. China’s profitability has now surpassed that of Indonesia.

Looking ahead, the pattern of cost divergence in and outside China is expected to persist in the short term. In China, the pullback in Philippine nickel ore prices supports smelting costs remaining low, while high-grade NPI prices remain high under a supply-demand tight balance, and the environment of smelter profit recovery will continue; in Indonesia, tight nickel ore supply, declining grades, and the crowding out of power resources by aluminum smelting are still fermenting, coupled with rising auxiliary material costs, leading to an expected continued climb in production costs, further pressuring smelter profit margins, and making the divergence in profitability in and outside China more pronounced.

III. Raw Material Competition: The Reshaping of Substitution Relationships Among Steel Scrap, FeNi, Refined Nickel, and NPI

As NPI grades decline and prices remain high, the competitive landscape among stainless steel raw materials is changing, with the substitution effect of steel scrap, FeNi, and refined nickel gradually strengthening, and NPI's position is being continuously squeezed.

Steel scrap price advantage re-emerges: Amid the confirmation of the reverse invoicing whitelist, weakening stainless steel prices, and narrowing steel mill profits, the price advantage of stainless steel scrap expanded again. Steel mills, to reduce costs, tended to increase the proportion of steel scrap addition and reduce the use of high-priced NPI, directly weakening NPI's demand elasticity.

FeNi demand recovers in phases: Affected by the declining grade of Indonesian NPI, high-grade NPI suffered from insufficient effective nickel element supply. Stainless steel enterprises began increasing FeNi procurement as a supplementary raw material to ensure nickel content amid inadequate NPI nickel grades, leading to significant growth in FeNi demand.

Refined nickel demand recovers marginally: As NPI prices remained high, the price spread between refined nickel and NPI gradually narrowed. Some steel mills started increasing the proportion of refined nickel use in high-grade stainless steel production, replacing some high-priced NPI.

In the medium and long term, the shares of steel scrap, FeNi, and refined nickel are expected to continue rising. NPI's share in stainless steel raw materials will be partially crowded out, and the trend toward diversification of raw material structure will further strengthen.

IV. Market Outlook: Tight Balance to Persist During 2026-2030, Supply Bottlenecks Emerge as New Key Driver

Looking ahead to 2026-2030, the global high-grade NPI market has shifted from previously expected small surpluses to deficits, sustaining a long-term tight balance. 2026-2027 could be the most supply-constrained period. Constrained by resources and power, Indonesia's capacity growth is unlikely to pick up significantly. China's production may recover in phases but will struggle to provide effective incremental volumes. Against the backdrop of mild growth in stainless steel consumption, the supply-demand gap is expected to persist. Meanwhile, supported by costs, the price center for high-grade NPI is expected to stay high. Attention should be paid to subsequent market adjustments and optimization of alternative pathways, which may gradually ease the deficit pressure.