Today, the General Administration of Customs released import and export data for April 2026. Customs data showed:

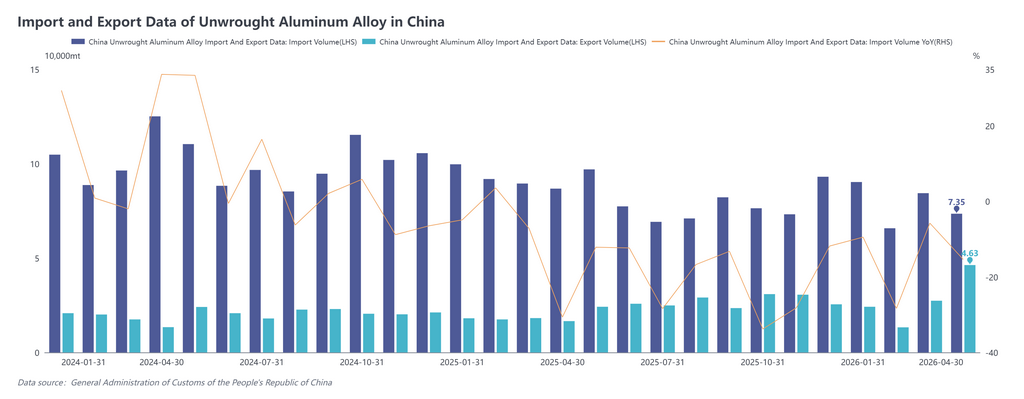

Imports of unwrought aluminum alloy in April 2026 were 73,500 mt, down 15.4% YoY and down 12.9% MoM. Cumulative imports from January to April 2026 were 313,900 mt, down 14.6% YoY.

Exports of unwrought aluminum alloy in April 2026 were 46,300 mt, hitting a single-month export high since July 2022, surging 179.7% YoY and up 68.9% MoM. Cumulative exports from January to April 2026 were 111,200 mt, up 58.1% YoY.

Import source structure, the concentration of import sources for unwrought aluminum alloy in China remained high in April 2026, with the top five sources accounting for approximately 77% combined. Among them, Malaysia ranked first with imports of 22,600 mt, its share rebounding to 31%; Thailand and Russia ranked second and third with imports of 12,700 mt and 11,800 mt respectively, while Russia's share edged down to 16%; Vietnam and Mongolia ranked fourth and fifth with imports of 8,300 mt and 1,600 mt respectively. MoM from March, total imports decreased by 10,900 mt, with the decline mainly from Thailand and Russia, while Malaysia and Vietnam saw slight increases.

Trade mode, processing trade with supplied materials ranked first at 21,300 mt (46% share), followed by Entrepot Trade by Customs Special Control Area and processing trade with imported materials in second and third place, accounting for 21% and 20% respectively. Notably, Ordinary Trade exports reached 6,066 mt, with its share jumping to 13%, a significant increase from the previous level of less than 1%. Considering the 15% export tariff, the current export structure remained dominated by processing trade (nearly 70%), but driven by overseas supply gaps triggered by Middle East geopolitical conflicts, Ordinary Trade exports achieved a substantial increase.

Destination structure, Japan remained the top export destination, with April exports of 22,800 mt, accounting for as high as 49% and occupying nearly half of the total, with processing trade with supplied materials as the primary export mode. Thailand, Morocco, South Korea, India, and Brazil formed the second tier, with individual country shares mostly ranging between 5%-8%, indicating relatively dispersed market distribution. Among them, Southeast Asian and Asian markets carried higher weight, reflecting regional manufacturing relocation and growing ex-China die-casting demand, providing important support for China's aluminum alloy exports.

Overall, in April 2026, China's unwrought aluminum alloy imports continued to pull back, while exports performed strongly, hitting a record single-month high. Import side, after March, geopolitical tensions in the Middle East drove LME aluminum prices to surge, compounded by logistics disruptions, pushing up ADC12 prices outside China, with import margins narrowing rapidly and turning into losses. In April, losses continued to widen under the dual squeeze of elevated prices outside China and weak downward-fluctuating prices in China. Currently, ADC12 prices outside China are quoted at $3,340-3,420/mt, with per-mt import losses exceeding 3,000 yuan, and imports in May are expected to shrink further. Export side, the supply gap outside China triggered by geopolitical conflicts released the export potential of aluminum alloys, and exports in May are expected to stay high. The sustainability of future exports will mainly depend on the pace of supply chain recovery in the Middle East and the long-term growth potential of the die-casting market in Southeast Asia.

![[SMM Analysis] The Southeast Asian secondary aluminum market remains in the doldrums, while the import window has improved but transactions are yet to recover.](https://imgqn.smm.cn/usercenter/iCOMR20251217171653.jpg)