SMM, May 20

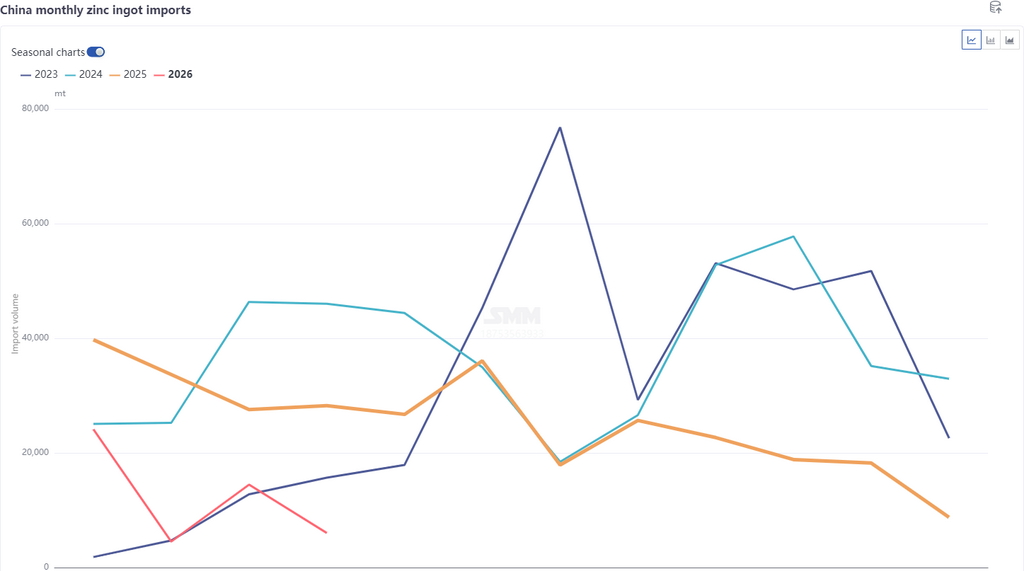

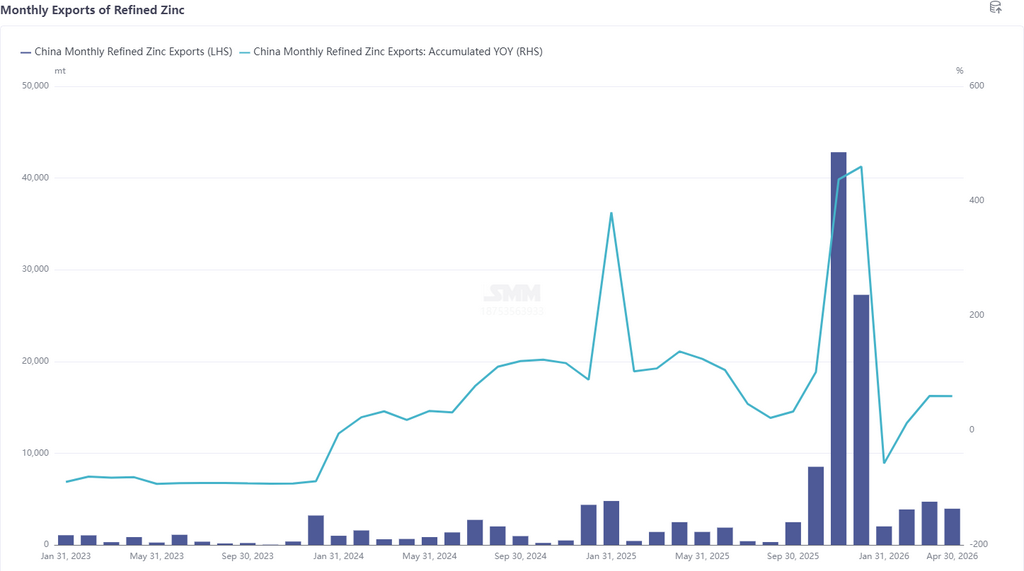

According to the latest customs data, refined zinc imports in April 2026 totaled 6,000 mt, down 8,400 mt or 58.27% MoM and down 78.62% YoY. Cumulative refined zinc imports from January to April were 49,000 mt, down 61.98% YoY. Refined zinc exports in April were 3,900 mt, down 16.22% MoM and up 59.21% YoY. Cumulative refined zinc exports from January to April were 14,000 mt, up 59.69% YoY. That is, net imports of refined zinc in April were 2,000 mt, with cumulative net imports from January to April at 34,500 mt.

By country, the top 3 refined zinc import sources in April remained Kazakhstan (4,500 mt, 74.26%), South Korea (700 mt, 11.52%), and Australia (500 mt, 8.53%); the top 3 export destinations in April were Vietnam (1,300 mt, 32.61%), Thailand (900 mt, 23.18%), and Indonesia (700 mt, 17.99%). The decline in April refined zinc import data was mainly due to the continued closure of the import window and reduced tail-end shipments of Kazakh zinc in April. However, imports still reached 6,000 mt, primarily driven by inflows of Entry and Exit Goods in Bonded Control Areas, accounting for 74%. Exports edged down mainly because the export window, though close to opening, remained closed, with some traders exporting small volumes of spot cargo to Southeast Asia. Additionally, from the trade mode perspective, Entry and Exit Goods in Bonded Control Areas accounted for over 80%, with bonded outflows dominating.

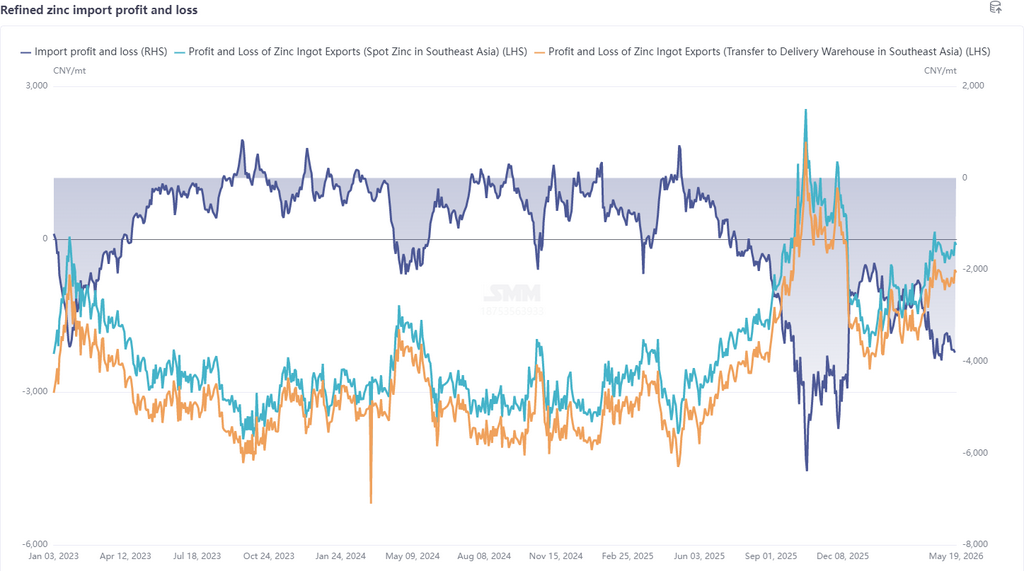

Entering May, on the macro front, geopolitical conflicts eased somewhat, but US PPI data significantly exceeded expectations, the US dollar and Treasury yields rose, market rate hike expectations increased, concerns over liquidity intensified, and macro uncertainties grew. Fundamentals side, overseas supply disruptions continued: Kazzinc's Ust-Kamenogorsk metallurgical complex in eastern Kazakhstan reduced its load after an explosion at its zinc and lead smelters; Peru declared an energy crisis, which has had no impact so far, but given that local zinc concentrates production accounts for 10.5% of global total production and China's dependence on Peruvian zinc concentrates stands at 7.7%, market sentiment fluctuated; additionally, on May 13, Peru's Cajamarquilla zinc smelter with annual production of 345,000 mt suffered a sudden fire, with some infrastructure damaged and operations suspended, and the specific magnitude of impact still requires further monitoring. Although LME inventory increased, it remained at a relatively low level of around 110,000 mt, and LME zinc prices held up well. China side, high smelter production and ore tightness continued to counterbalance each other, with TC declining to historical lows, providing bottom support for zinc prices. However, consumption performed weakly: the rainy season in south China weighed on real estate and infrastructure, April auto data declined both YoY and MoM, home appliance domestic sales were weak with divergent exports, and overall consumption showed no bright spots, with social inventory fluctuating at highs above 260,000 mt. Overall, the pattern of LME outperforming SHFE has not yet changed, the import window remained closed, and May imports are expected to decline further. The export window has not fully opened, but considering that some traders still export spot cargo to Southeast Asia and bonded warehouse goods still have the possibility of outflows, exports are expected to increase slightly.

Data Source Disclaimer: Data other than publicly available information is derived by SMM based on public information, market communication, and SMM's internal database models, and is for reference only and does not constitute decision-making advice.