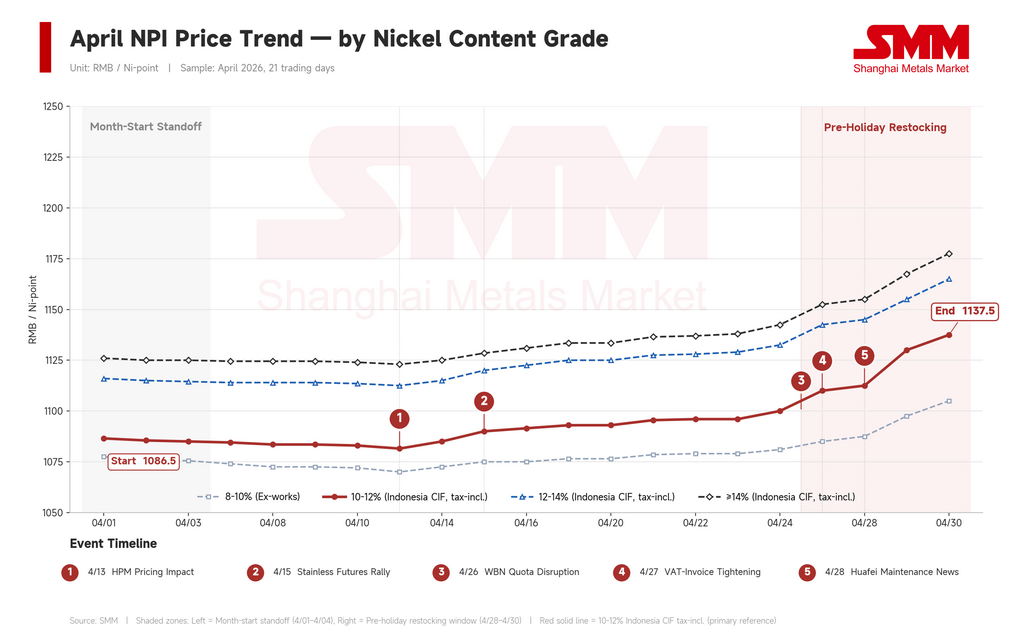

Indonesian high-grade nickel pig iron (NPI) closed April at approximately RMB 1,138 per nickel point ($166), up 4.7% from RMB 1,087 ($159) at the start of the month. But the headline figure flatters a more complicated story. April broke into three phases: early-month weakness as scrap competition capped buying interest, mid-month firming as Indonesian cost signals shifted seller psychology, and a final-week breakout that was driven almost entirely by the nickel futures rally rather than anything happening on the ground in Indonesia.

For context: NPI in China and Indonesia is priced per nickel point — that is, per percentage point of contained nickel. An 11% NPI cargo at RMB 1,138 per nickel point translates to roughly RMB 12,520/mt ($1,830/mt) of physical product. NPI is a low-grade ferro-nickel alloy produced primarily from laterite ore and used almost exclusively as feedstock for stainless steel.

Phase 1: Scrap kept NPI capped (April 1–15)

The first half of April looked like a standoff between holding-out sellers and resistant buyers. In reality, prices drifted lower — the 10–12% Indonesian CIF benchmark slipped from RMB 1,087 to RMB 1,082 per nickel point.

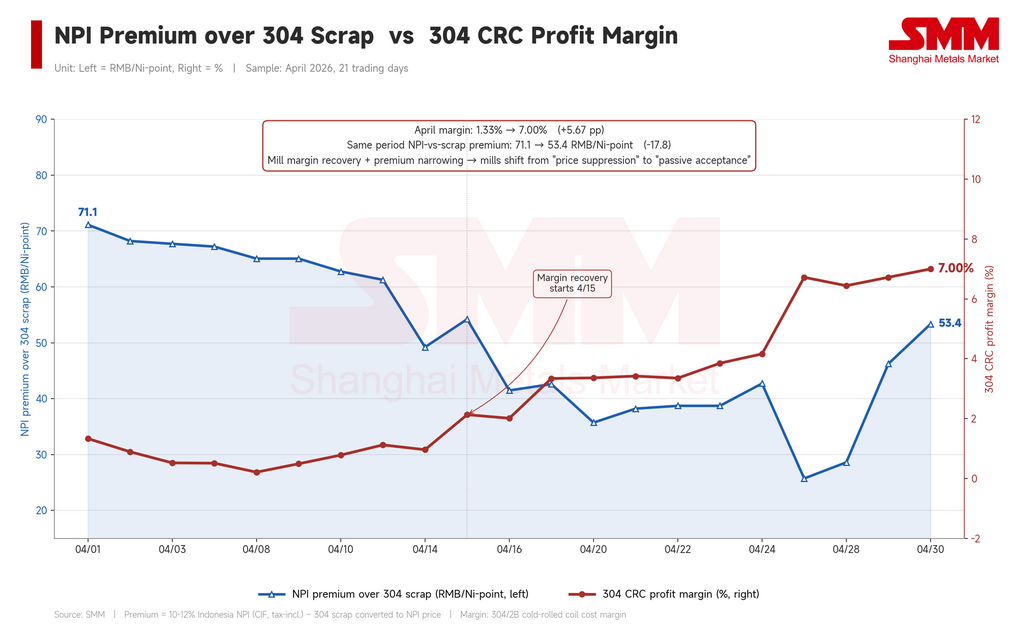

The drag came from the substitute, not from NPI itself. At the start of the month, NPI traded at a premium of RMB 71.12 ($10.40) per nickel point over 304 stainless scrap on a contained-nickel basis — meaning scrap was nearly 10% cheaper than NPI per unit of nickel content. With cold-rolled coil (CRC) margins below 2%, Chinese stainless mills had every reason to push scrap inputs to the maximum and keep NPI procurement to a minimum. Lower-nickel-content cargoes moved poorly even when offered near RMB 1,050.

Bullish narrative was not in short supply — Indonesia's HPM (Harga Patokan Mineral, the country's official monthly mineral reference price) revisions, higher freight, and ore-side cost pressure were all in circulation. But none of it made it into actual transaction prices. Cost-side stories don't move the spot market until downstream cost structures shift to absorb them.

Phase 2: Seller psychology resets (mid-April)

The turn came in mid-April. Expectations of a structural revision to Indonesia's HPM formula firmed, raising the implied floor under Indonesian NPI production costs. Indonesian tender prices stepped up. A nickel project inside one of the major Indonesian industrial parks reportedly idled lines — the actual output impact was modest, but the signal mattered.

The bigger shock came from sulfur. Prices jumped from $725/mt to $1,020/mt during the month, a 40.7% increase, pressuring HPAL (high-pressure acid leach) project economics. Reports that Huafei Nickel-Cobalt — Zhejiang Huayou Cobalt's HPAL project — would cut roughly 50% of output for maintenance starting May 1 emerged from the same pressure. None of this directly raised NPI cash costs, but it changed how nickel units across the chain were expected to flow, and that fed into seller psychology.

What these developments actually accomplished wasn't a price increase; it was the disappearance of cheap offers. Sellers who had been willing to clear at RMB 1,080 or below pulled back. Quotation logic shifted from "discount to mean" to "premium to mean." The 10–12% Indonesian CIF benchmark moved up to RMB 1,093 per nickel point by the third week. Stainless steel futures firmed, and CRC margins recovered toward 3%. But buyer acceptance lagged — 11.5%-grade port-pickup quotes were still struggling to clear above RMB 1,100 per nickel point.

Phase 3: The nickel rally breaks the range (final week)

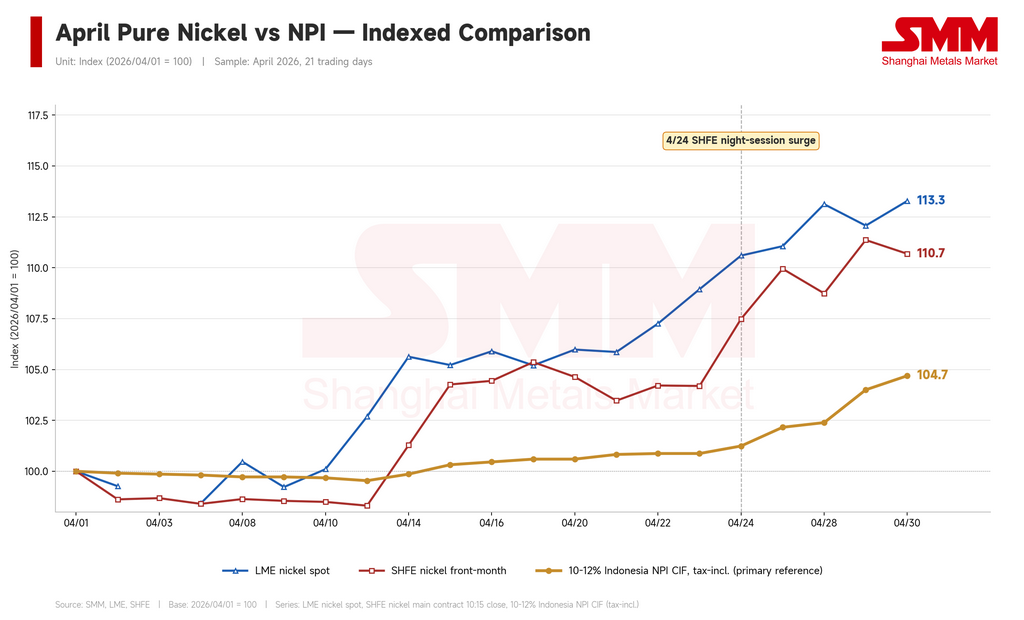

The actual breakout came in the last week, and it didn't come from Indonesia. WBN (Weda Bay Nickel) mining quota issues added another supply-side wrinkle, but the dominant force was the refined nickel rally on the screens. LME nickel rose from $17,023/mt to $19,284/mt over the month (+13.3%), and SHFE nickel jumped from RMB 135,700 to RMB 150,200/mt ($19,840 to $21,960, +10.7%). On the night the SHFE main contract leapt from RMB 145,900 to 151,100/mt, the 10–12% Indonesian NPI benchmark moved from RMB 1,100 to 1,138 per nickel point in just four trading sessions — close to a 4% gain.

The last-week move was a chain reaction off LME nickel. Stainless followed: 304/2B in Wuxi (a major eastern China stainless trading hub) climbed from RMB 14,400 to 15,450/mt ($2,105 to $2,259), or +7.3%. Critically, stainless rose faster than NPI — CRC margins expanded from 1.33% at the start of the month to roughly 7% by month-end. That margin expansion is what enabled mills to accept higher NPI prices. Without it, the breakout doesn't happen.

The premium of high-grade NPI over stainless scrap also reflects this process from another angle. From a premium of 71.12 yuan/mtu at the beginning of the month, the spread narrowed to a monthly low of 25.71 yuan/mtu by mid-to-late April. This means that, over the same period, stainless scrap prices on an NPI-equivalent basis rose faster than NPI itself.

As stainless steel prices strengthened, stainless scrap prices also moved higher, sharply narrowing NPI’s cost disadvantage against scrap. Together with tighter invoice controls and additional constraints on scrap procurement and circulation, mills had stronger incentives to switch part of their feedstock demand back to NPI.

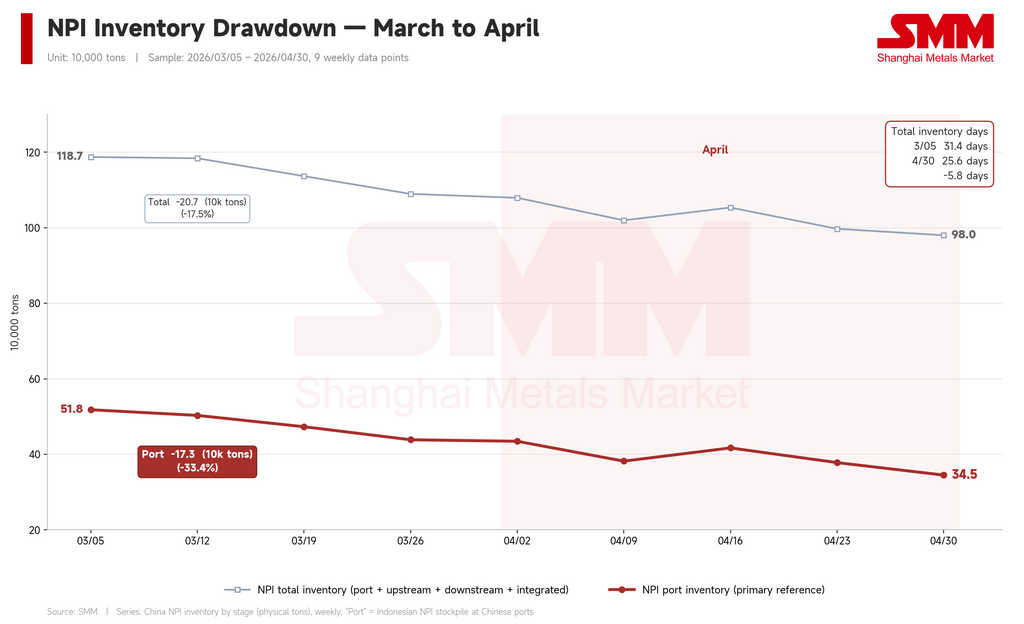

Inventory data confirms the switch. Chinese port stocks of NPI fell from 435,000 mt to 345,000 mt over the month — a 90,000 mt drawdown, or 20.6%. Total inventory dropped from 1.08 million mt to 980,000 mt; days-of-inventory cover compressed from 28.3 to 25.6. This was passive restocking — mills absorbed port material rapidly as relative pricing flipped and the scrap channel narrowed.

By the final two trading days of the month, NPI was rising faster than scrap, reopening the premium back to RMB 46–53 per nickel point. If that gap continues to widen in May, scrap competition could quickly reassert itself.

Grade spreads widened — but not where you'd expect

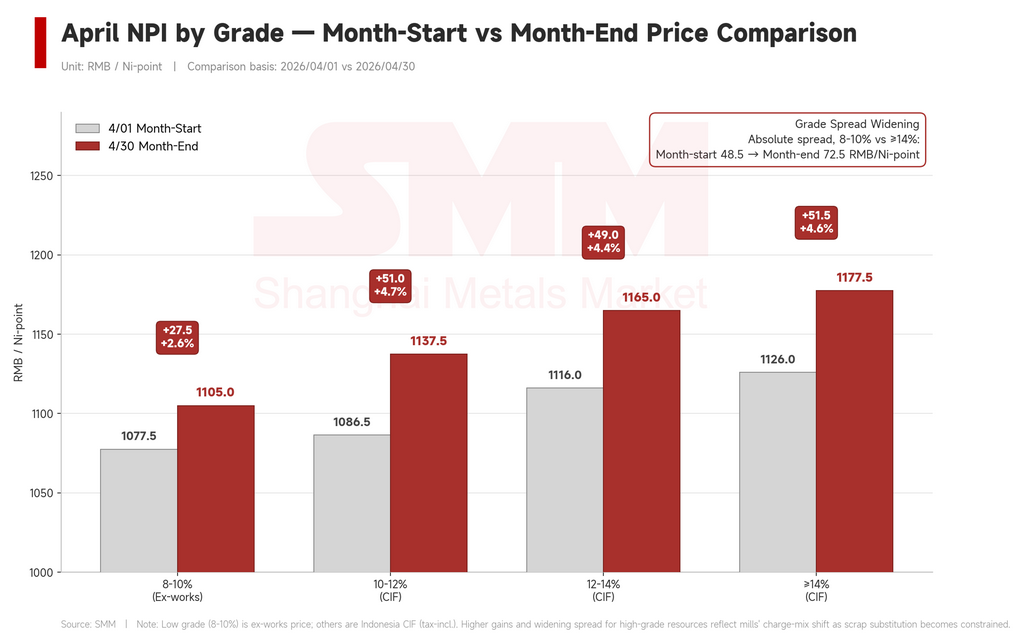

April's gains layered unevenly across grades. Domestic 8–10% NPI ex-works rose 2.6% (from RMB 1,077.5 to 1,105 per nickel point). The Indonesian CIF benchmarks for 10–12%, 12–14%, and ≥14% all rose between 4.4% and 4.7% — roughly twice the pace of domestic low-grade material.

The absolute spread between domestic 8–10% and Indonesian ≥14% widened from RMB 48.5 to 72.5 per nickel point ($7.09 to $10.60). The mechanism: under scrap-substitution pressure, mills actively shifted feedstock blends toward higher-grade Indonesian material, which is more efficient at hitting nickel-content targets. Domestic low-grade material got marginalized.

Within the Indonesian grades, however, no clear leader emerged. The 12–14% premium over 10–12% actually compressed slightly (from RMB 29.5 to 27.5); the ≥14% premium held roughly flat (RMB 39.5 to 40). Brief mid-month widenings — peaks of RMB 33 and 42.5 respectively — pointed to structural tightness in higher grades, but the late-month broad rally erased those premiums quickly.

So April's grade-spread story is really about domestic-versus-Indonesian divergence, not Indonesian-grade differentiation. A pattern of broad-based grade strength across Indonesian CIF, layered on top, has historically meant steep upside followed by fragile pullbacks.

May: three external variables, not Indonesian ones

Indonesian narrative will continue in May. HPM, WBN, sulfur, Huafei maintenance — all of it will keep cycling through the news flow and providing marginal cost support. But the actual direction of NPI prices will be set by three external variables.

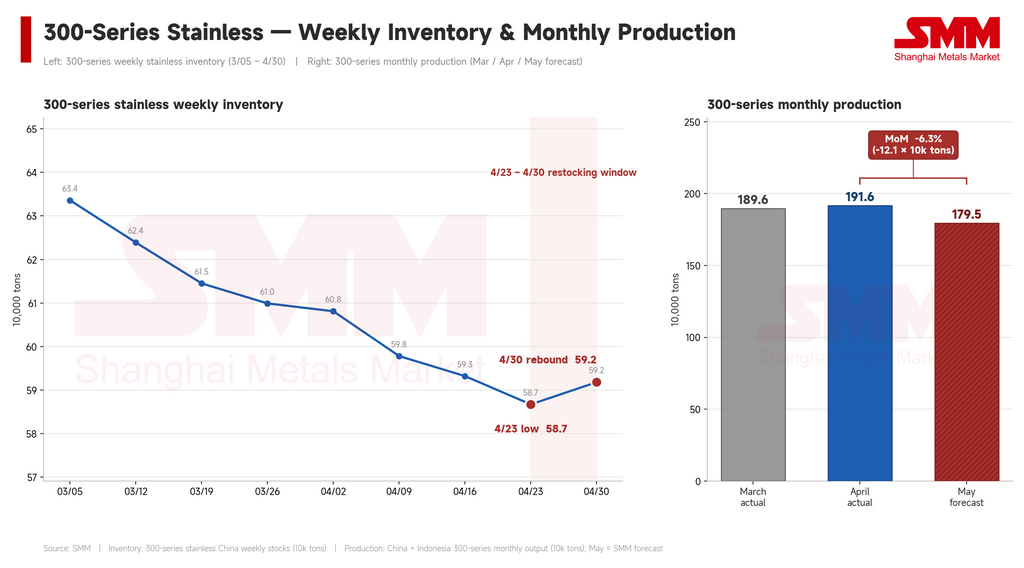

The first is stainless steel. NPI's ability to extend higher depends entirely on whether stainless prices hold and mill margins stay elevated. The expansion from 1.33% to 7% CRC margin was the foundation of late-April's gains. Two warning signs are already visible: 300-series stainless inventory rose slightly from a monthly low of 587,000 mt to 592,000 mt heading into the May 1 Labor Day holiday, suggesting demand is starting to lag behind upstream restocking; and SMM forecasts May 300-series production in China and Indonesia at 1.795 million mt, down 121,000 mt or 6.3% from April's 1.916 million mt. A weaker stainless market with shrinking margins immediately erodes mills' ability to pay up for feedstock. This is the single most sensitive variable in the system.

The second is the NPI-scrap premium. With the late-month rally already pushing it back to RMB 53 per nickel point, any easing of VAT-invoicing controls or restoration of normal scrap circulation will see mills push scrap blends back up — and NPI demand support will weaken in step.

The third is refined nickel itself. NPI follows nickel futures with a lag; when the screen pulls back, NPI loses momentum quickly. Trading at RMB 1,150 per nickel point depends substantially on SHFE nickel holding near RMB 150,000/mt. If the contract retraces toward RMB 140,000/mt or below, the basis for trading at current NPI levels weakens.

Base case: May NPI ranges between RMB 1,130 and 1,170 per nickel point ($165–171), but the range is fragile. Pre-holiday restocking and unresolved Indonesian noise provide near-term support. But the projected 121,000 mt monthly drop in stainless production weakens the demand backbone for high-priced NPI, downstream stainless has limited room for further margin expansion, and refined nickel has limited additional upside. Upside risk: stainless futures and physical prices firm together while scrap controls stay tight. Downside risk: stainless prices retrace, refined nickel pulls back, and scrap regains its cost advantage simultaneously.

Conclusion

NPI ended April at RMB 1,138 per nickel point, with transaction levels migrating from RMB 1,070–1,090 to RMB 1,130–1,150. The aggregate move was moderate, but the three phases each had different drivers: scrap competition kept prices weak in the first half; HPM and Indonesian tenders reset seller psychology in mid-month; WBN, sulfur, and Huafei sharpened the supply narrative late; and the refined nickel rally drove the final-week breakout downstream.

Indonesian cost factors — HPM revisions, ore grade, reagent prices — are necessary conditions for any sustained NPI price-center upgrade. They are not sufficient. Whether NPI rises, how far, and how stably depends increasingly on two external variables: refined nickel futures and downstream stainless prices. That is the structural feature of a midstream product whose production is concentrated in Indonesia but whose pricing power is dispersed across Chinese stainless mills and Asian futures markets. It is not a feature of any single month's market action. To track May from here, watch those two variables.

Written by Bruce Chew

Nickel & Stainless Steel Analyst, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088

![[SMM Analysis] May 2026 Global (Ex-China) Stainless Steel Market Review, Indonesia Export Six-Month Rally Ends](https://imgqn.smm.cn/usercenter/qLeLR20251217171733.jpg)