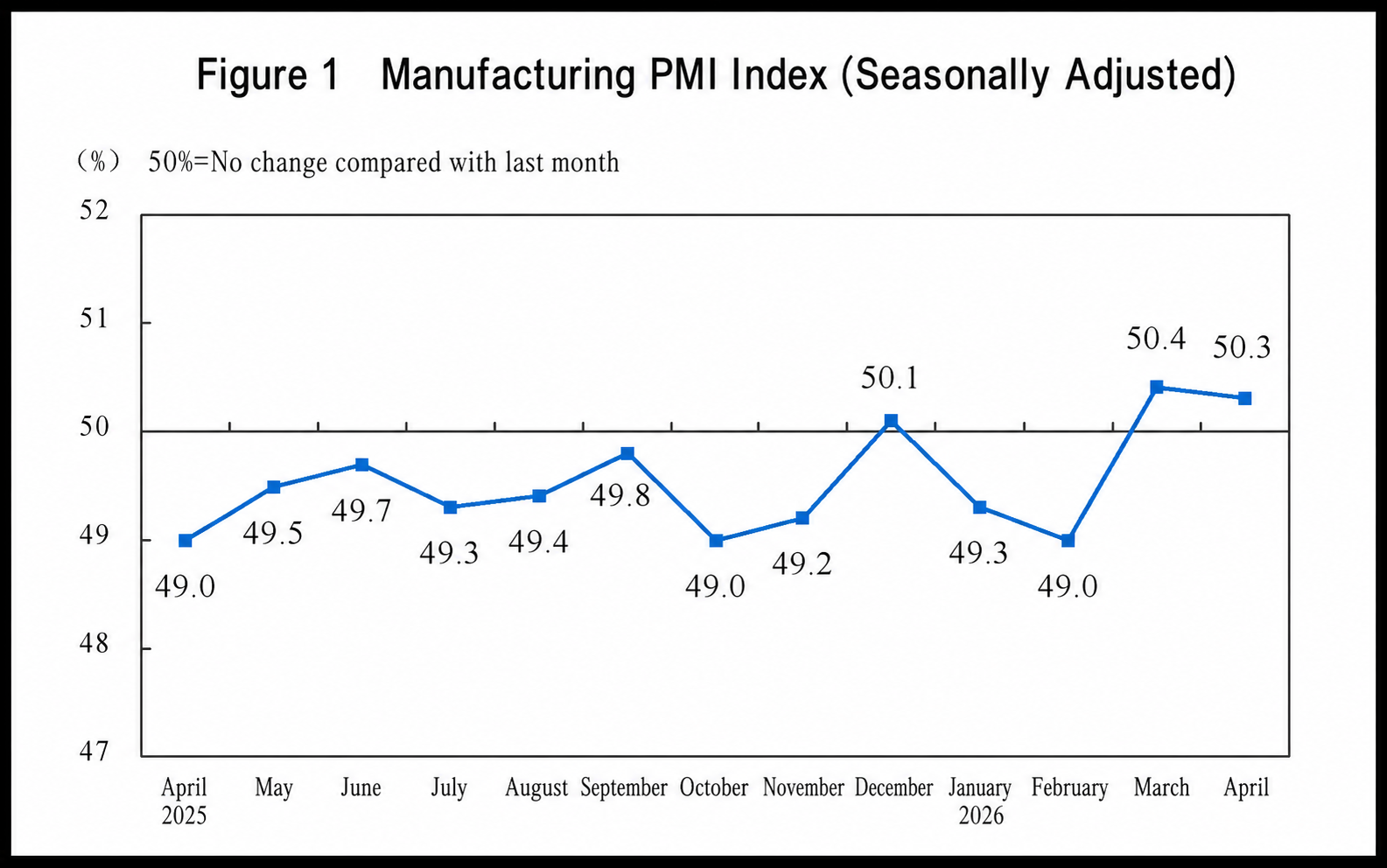

The NBS Service Industry Survey Center and the China Federation of Logistics and Purchasing released China's PMI for April today. The manufacturing PMI continued to operate in expansion territory after rebounding into expansion territory in March, indicating that the manufacturing sector maintained a generally stable level of prosperity and continued its favorable operating trend. In April, China's manufacturing PMI was 50.3%, down 0.1 percentage points MoM, operating in expansion territory for the second consecutive month.

China's PMI Performance in April 2026

I. China's Manufacturing PMI Performance

In April, the manufacturing PMI stood at 50.3%, down 0.1 percentage points from the previous month, with the manufacturing prosperity level remaining generally stable.

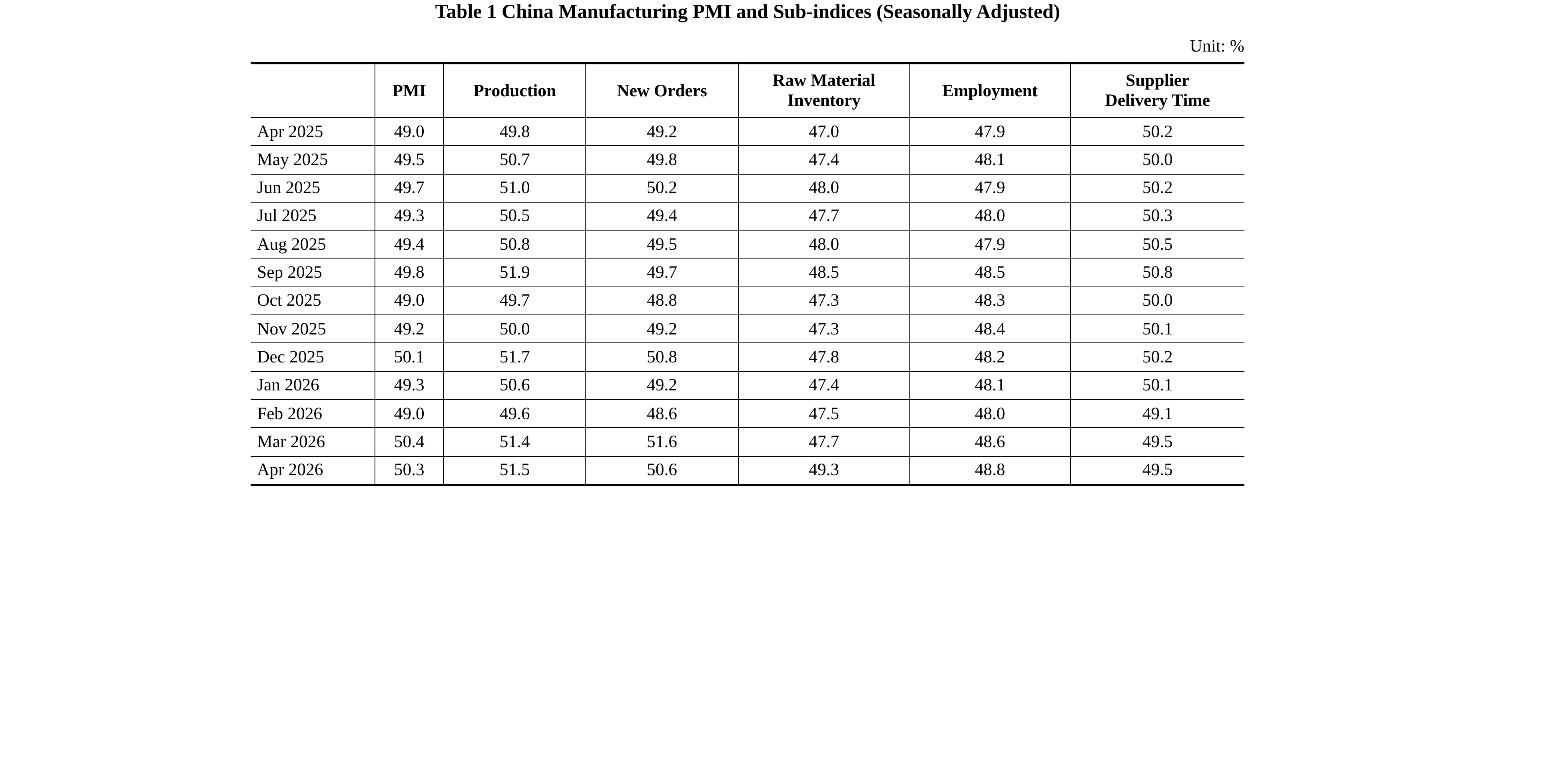

By enterprise size, the PMI for large enterprises was 50.2%, down 1.4 percentage points MoM but still above the threshold; the PMIs for medium and small enterprises were 50.5% and 50.1% respectively, up 1.5 and 0.8 percentage points MoM, both above the threshold.

By sub-indices, among the five sub-indices constituting the manufacturing PMI, the production index and new orders index were both above the threshold, while the raw material inventory index, employment index, and supplier delivery time index were all below the threshold.

The production index was 51.5%, up 0.1 percentage points MoM, indicating that manufacturing production activity accelerated somewhat.

The new orders index was 50.6%, down 1 percentage points MoM but still above the threshold, indicating that manufacturing market demand maintained expansion.

The raw material inventory index was 49.3%, up 1.6 percentage points MoM, indicating that the decline in major raw material inventory in manufacturing narrowed significantly.

The employment index was 48.8%, up 0.2 percentage points MoM, indicating a rebound in the employment prosperity level of manufacturing enterprises.

The supplier delivery time index was 49.5%, unchanged from the previous month and below the threshold, indicating that delivery times of raw material suppliers in manufacturing continued to lengthen MoM.

II. China's Non-Manufacturing PMI Performance

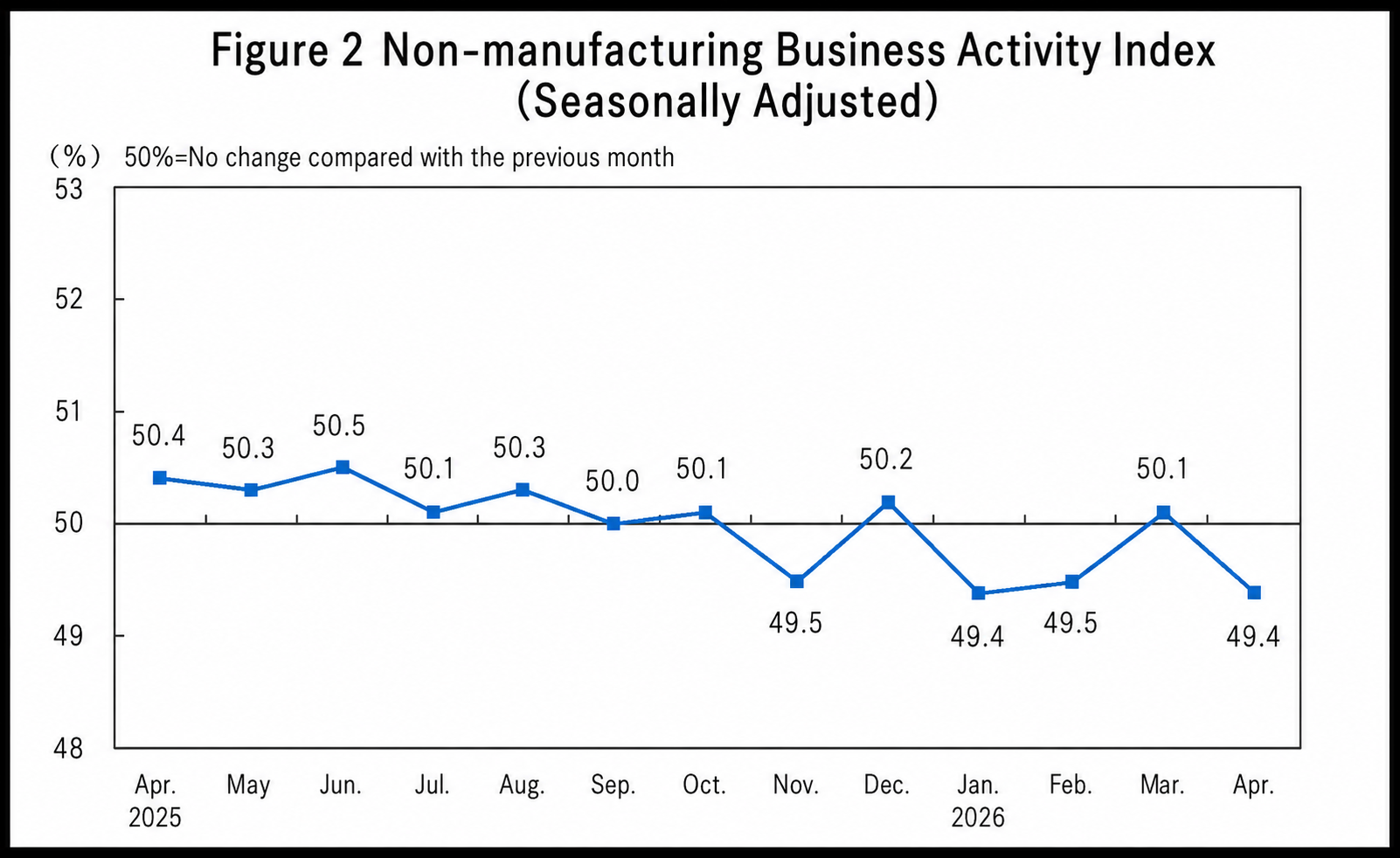

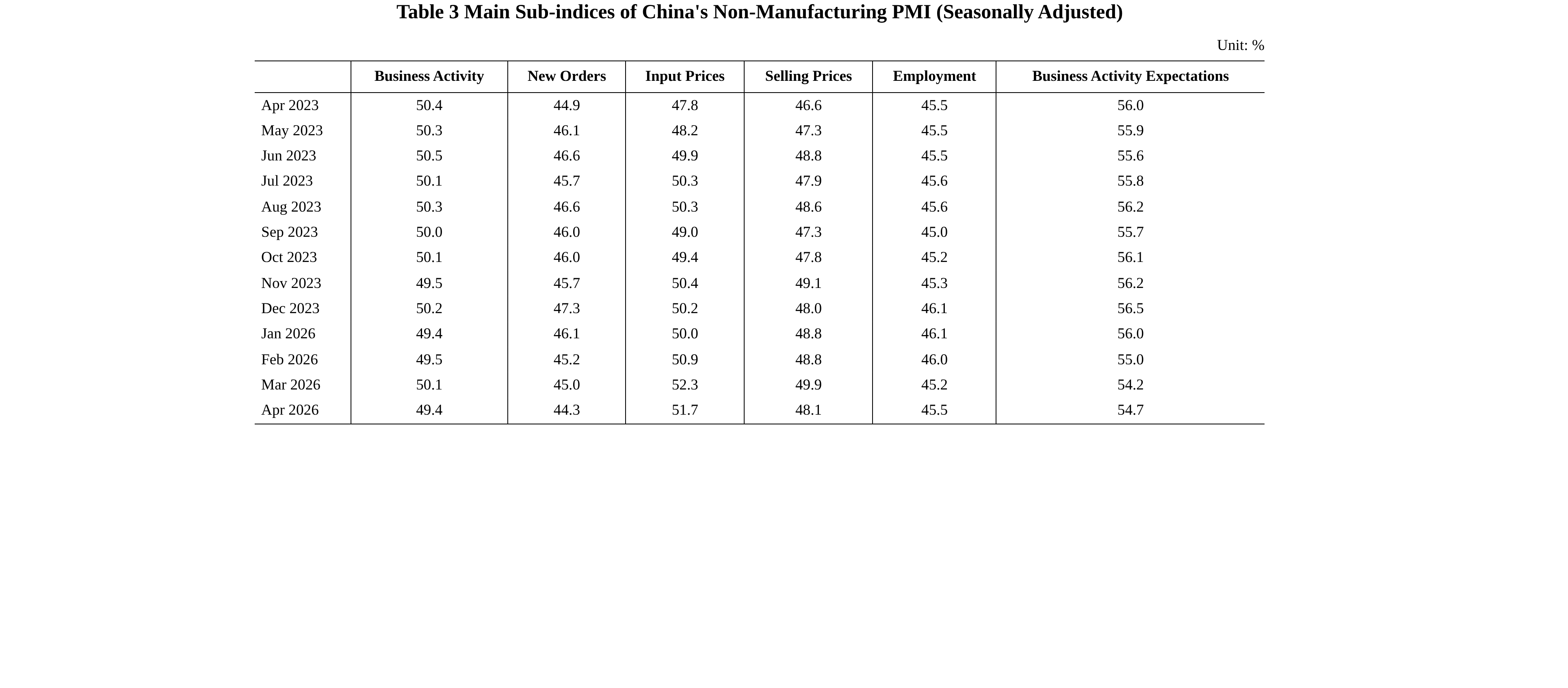

In April, the non-manufacturing business activity index was 49.4%, down 0.7 percentage points from the previous month, with the non-manufacturing prosperity level declining somewhat.

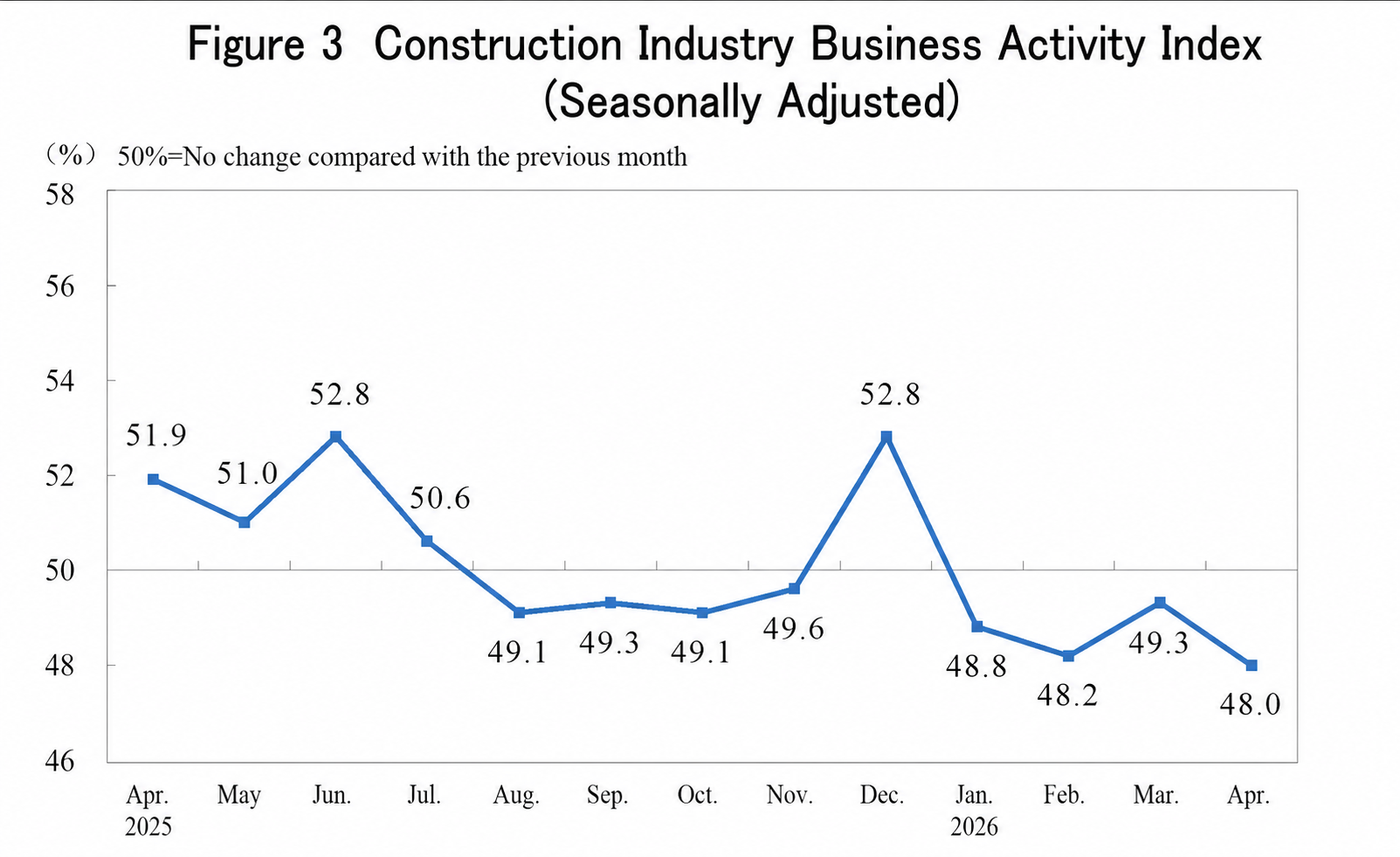

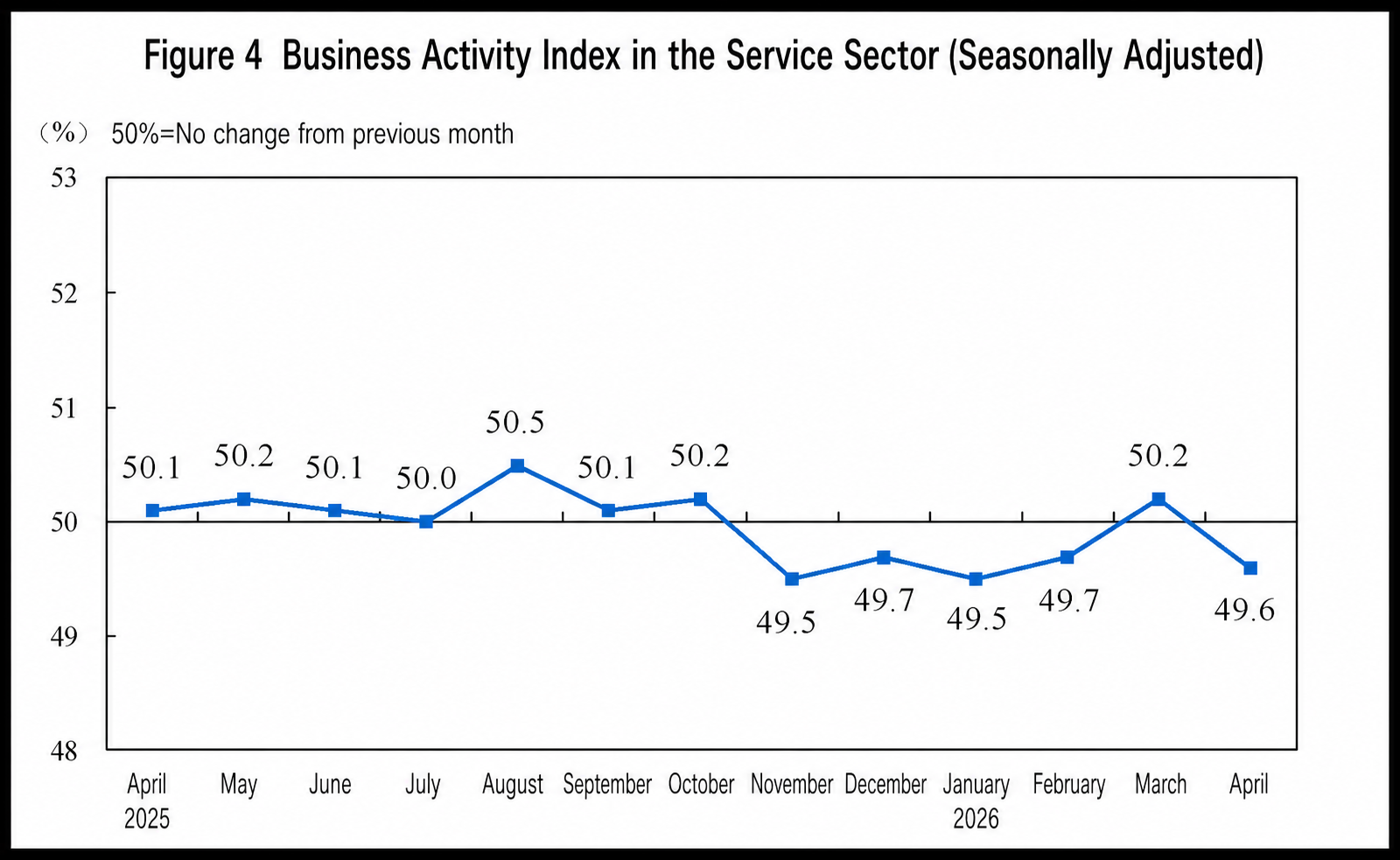

By sector, the construction business activity index was 48.0%, down 1.3 percentage points MoM; the services business activity index was 49.6%, down 0.6 percentage points MoM. Within the services sector, industries such as railway transportation, postal services, and telecommunications, broadcasting, television, and satellite transmission services all had business activity indices above the relatively high prosperity zone of 55.0%; industries such as wholesale, retail, and resident services all had business activity indices below the threshold.

The new orders index was 44.3%, down 0.7 percentage points MoM, indicating a decline in non-manufacturing market demand. By sector, the construction new orders index was 41.6%, down 1.9 percentage points MoM; the services new orders index was 44.8%, down 0.5 percentage points MoM.

The input price index was 51.7%, down 0.6 percentage points MoM but still above the critical point, indicating that input prices for non-manufacturing business activities continued to rise overall. By sector, the construction input price index was 54.9%, up 2.2 percentage points MoM; the services input price index was 51.2%, down 1 percentage points MoM.

The selling price index was 48.1%, down 1.8 percentage points MoM, indicating an overall decline in non-manufacturing enterprise selling prices. By sector, the construction selling price index was 49.0%, down 0.3 percentage points MoM; the services selling price index was 47.9%, down 2.1 percentage points MoM.

The employment index was 45.5%, up 0.3 percentage points MoM, indicating improved employment conditions in non-manufacturing enterprises. By sector, the construction employment index was 39.6%, up 0.5 percentage points MoM; the services employment index was 46.5%, up 0.3 percentage points MoM.

The business activity expectations index was 54.7%, up 0.5 percentage points MoM, indicating strengthened confidence among non-manufacturing enterprises in market development. By sector, the construction business activity expectations index was 50.5%, unchanged MoM; the services business activity expectations index was 55.4%, up 0.6 percentage points MoM.

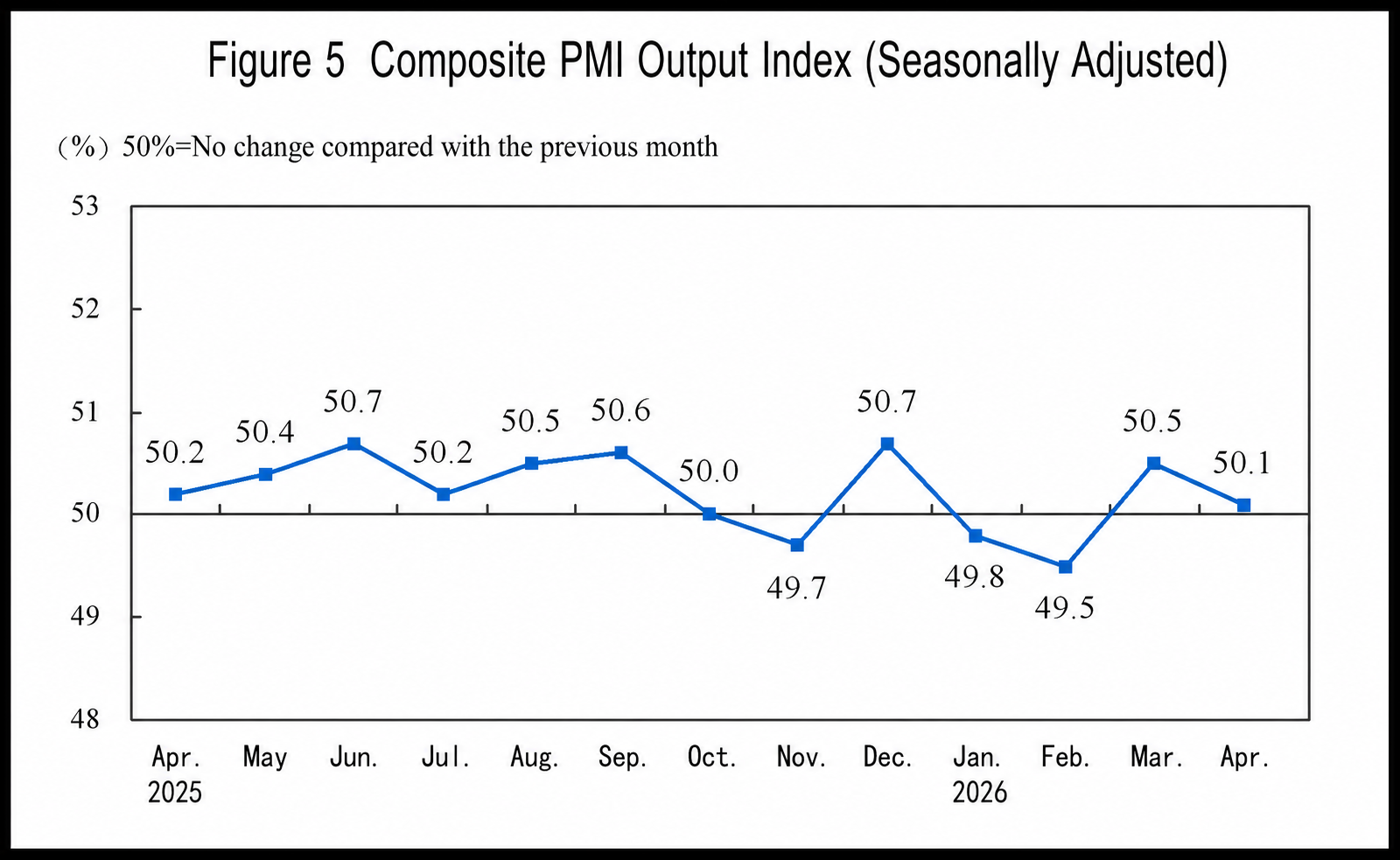

III. China Composite PMI Output Index

In April, the composite PMI output index was 50.1%, down 0.4 percentage points MoM but above the critical point, indicating that China's enterprise production and business activities continued to expand overall.

Manufacturing PMI Remained in Expansion Territory in April

— Interpretation of China's April 2026 PMI by Huo Lihui, Chief Statistician of the NBS Service Industry Survey Center

On April 30, 2026, the NBS Service Industry Survey Center and the China Federation of Logistics and Purchasing released China's PMI. Huo Lihui, Chief Statistician of the NBS Service Industry Survey Center, provided an interpretation.

In April, the manufacturing PMI was 50.3%, slightly lower than the previous month by 0.1 percentage points, remaining in expansion territory; the non-manufacturing business activity index was 49.4%, down 0.7 percentage points MoM; the composite PMI output index was 50.1%, down 0.4 percentage points MoM but still above the critical point, with China's overall economic output maintaining expansion.

I. Manufacturing PMI Remained above the Critical Point for Two Consecutive Months

In April, the manufacturing PMI was 50.3%, with the overall prosperity level remaining stable and the manufacturing sector sustaining a sound operating trend.

(I) Both production and demand continued to expand. The production index was 51.5% and the new orders index was 50.6%, both remaining above the critical point, indicating that manufacturing production and market demand stayed in expansion. By industry, the production and new orders indices for railway, shipbuilding, aerospace equipment, electrical machinery and equipment, and computer, communication and electronic equipment sectors were all at or above 53.0%, with production and demand in these industries being released at a faster pace; the two indices for petroleum, coal and other fuel processing, and chemical raw materials and chemical products sectors were both below the critical point, indicating relatively weak market activity. Driven by continued expansion in production and demand, enterprise purchase willingness further strengthened, with the purchasing volume index at 51.1%, up 0.2 percentage points from the previous month.

(II) PMIs for large, medium and small enterprises all remained in expansion territory. The PMI for large enterprises was 50.2%, staying above the critical point for five consecutive months; PMIs for medium and small enterprises were 50.5% and 50.1% respectively, up 1.5 and 0.8 percentage points from the previous month, both rising into expansion territory with prosperity levels rebounding notably.

(III) Three key industries sustained expansion. PMIs for high-tech manufacturing and equipment manufacturing were 52.2% and 51.8% respectively, up 0.1 and 0.3 percentage points from the previous month, with these industries maintaining a positive development trend; the PMI for consumer goods industries was 50.7%, remaining in expansion territory. The PMI for high energy-consuming industries was 47.9%, down 1 percentage point from the previous month, with the prosperity level pulling back.

(IV) Price indices fluctuated at highs. Affected by recent high-level fluctuations in some bulk commodity prices, the raw material purchase price index and ex-factory price index were 63.7% and 55.1% respectively, remaining at highs in recent years, with the overall price level in the manufacturing market rising notably. By industry, both price indices for petroleum, coal and other fuel processing, and chemical raw materials and chemical products sectors remained above 70.0% for two consecutive months, with raw material procurement prices and product selling prices in these industries continuing to rise.

(V) Market expectations continued to strengthen. The business activity expectations index was 54.5%, up 1.1 percentage points from the previous month, rebounding for three consecutive months, indicating that manufacturing enterprises' confidence in near-term market development continued to strengthen. By industry, the business activity expectations indices for food, beverages and refined tea, automobile, and railway, shipbuilding and aerospace equipment sectors were all in the relatively high prosperity zone above 58.0%, with enterprises in these industries being more optimistic about industry development.

II. Non-Manufacturing Business Activity Index Pulled Back

In April, the non-manufacturing business activity index was 49.4%, down 0.7 percentage points from the previous month, indicating a pullback in non-manufacturing prosperity.

(1) Service sector prosperity pulled back. The service sector business activity index was 49.6%, down 0.6 percentage points from the previous month. By industry, the business activity indices for railway transportation, postal services, and telecommunications, radio, television and satellite transmission services were all in the relatively high prosperity range above 55.0%, with rapid growth in total business volume; the business activity indices for wholesale, retail, and resident services were all below the critical point, indicating weak market activity. In terms of market expectations, the service sector business activity expectations index was 55.4%, up 0.6 percentage points from the previous month, rising into the relatively high prosperity range above 55.0%, indicating that service sector enterprises had strengthened confidence in future market development.

(2) Construction sector prosperity remained weak. The construction sector business activity index was 48.0%, down 1.3 percentage points from the previous month, with prosperity pulling back. In terms of market expectations, the construction sector business activity expectations index was 50.5%, unchanged from the previous month, indicating that construction enterprises maintained stable expectations for near-term industry development.

III. Composite PMI Output Index Remained in Expansion

In April, the composite PMI output index was 50.1%, down 0.4 percentage points from the previous month, indicating that overall production and business activities of China's enterprises continued to expand. The manufacturing production index and non-manufacturing business activity index, which constitute the composite PMI output index, were 51.5% and 49.4%, respectively.

![Metals Showed Mixed Performance, with Lithium Carbonate and SHFE Aluminum Leading the Declines, Polysilicon Falling More Than 5%, and Stainless Steel Rising Nearly 3% [SMM Midday Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Downstream restocking and cargo pick-up, market supply decreases [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/arNnt20251217171714.jpeg)

![The most-traded SHFE tin contract fluctuates at highs, and the spot trading sentiment further weakens [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/nyMyJ20251217171751.jpg)