On April 24, the SMM Imported Copper Concentrate Index (weekly) stood at -81.44 USD/dmt, down 2.83 USD/dmt from the previous reading of -78.61 USD/dmt. The deeply negative TC reflects the tightness in the global copper concentrate market, which has already shifted from market expectations to an actual rigid contraction in supply.

In the first quarter of 2026, the world's leading mining companies frequently revised down their production guidance, with supply-side disruptions far exceeding early-year forecasts. Freeport significantly lowered its full-year 2026 copper production forecast from 1.542 million tonnes to approximately 1.406 million tonnes, with an expected recovery rate of only 65%, due to slower-than-expected mine recovery at its Grasberg site in Indonesia, affected by mudslides and ore moisture. In addition, road blockades caused by strikes at BHP's Escondida and Zaldivar mines have led to actual production impacts that remain to be monitored.

According to SMM exclusive data, the global copper concentrate deficit in 2026 is estimated at 317,000 metal tonnes, a situation that may ease somewhat in 2029.

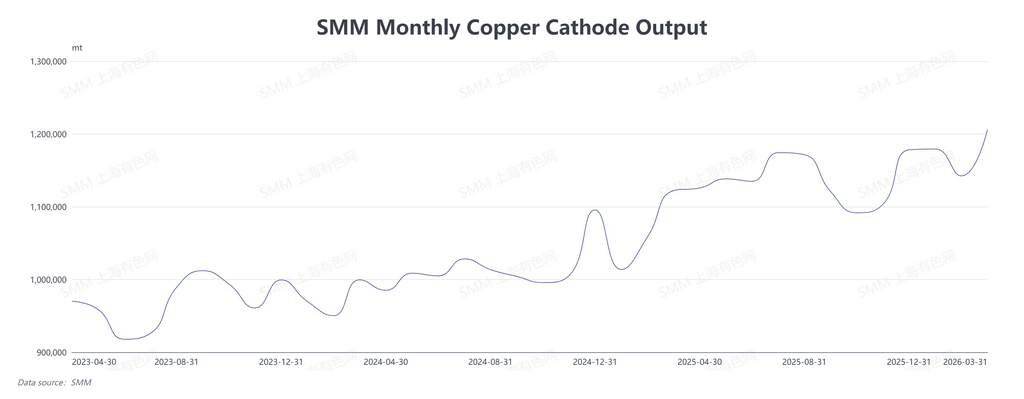

In stark contrast to the persistently falling TC, domestic smelter operating rates remained high in Q1 2026. According to SMM data, China's electrolytic copper output in March 2026 reached 1.2061 million tonnes, up 5.58% month-on-month and 7.49% year-on-year. In Q1 2026, total electrolytic copper output was 3.5278 million tonnes, up 4.60% quarter-on-quarter and 10.45% year-on-year.

SMM survey data shows that 11 smelters have confirmed maintenance schedules for Q2 2026. This means that domestic electrolytic copper output is expected to decline in Q2, with spot supplies likely tightening temporarily in May and June. However, some smelters have reported that due to high sulfuric acid prices, maintenance completion times may be brought forward.

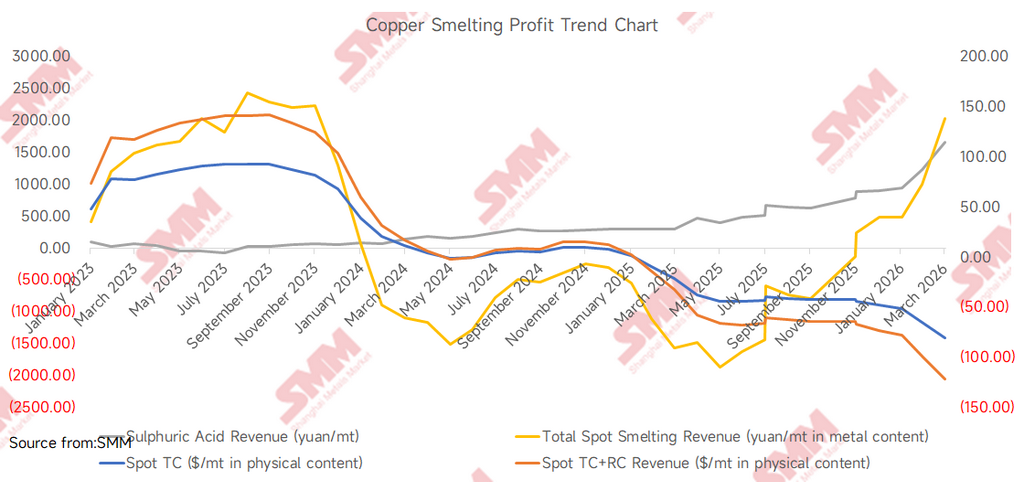

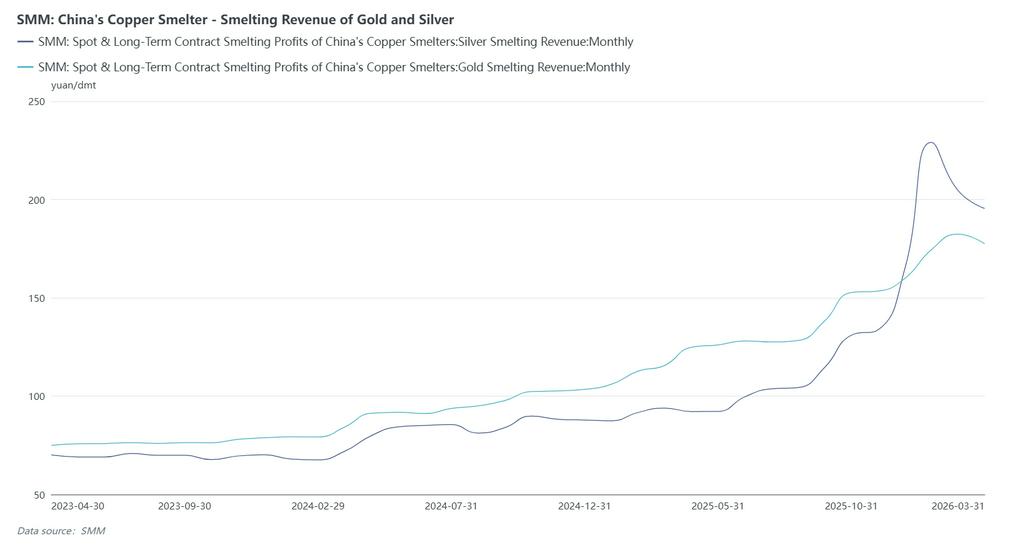

Sulfuric acid is currently the most important by-product revenue source for the copper smelting industry. According to SMM data, on April 24, 2026, China's copper smelting acid index stood at 1,660.5 RMB/ton, up 31.5 RMB/ton from the previous period. As sulfuric acid revenues have risen steadily from 890 RMB/ton at the start of 2026 to 1,660.5 RMB/ton in April 2026, based on the co-production of 3–4.5 tonnes of sulfuric acid per tonne of electrolytic copper, sulfuric acid income can now cover the copper concentrate procurement cost and part of the processing cost for smelters. The upward slope and magnitude of this increase exceed the deterioration in spot TC. The substantial boost in sulfuric acid profitability allows smelters to tolerate lower TC, creating a cycle of "higher sulfuric acid prices, lower TC." Meanwhile, rising gold and silver prices have further expanded smelters' comprehensive profit margins. Although the copper smelting segment is deeply loss-making, driven by the hefty profits from sulfuric acid, gold, and silver, domestic copper smelters have been able to maintain high operating rates without large-scale production cuts caused by deeply negative TC.

Additionally, about 20% of the world's electrolytic copper comes from hydrometallurgical processes, with the DRC and Chile together accounting for nearly 80% of that. Hydrometallurgical copper production consumes large amounts of sulfuric acid, and sulfur is a key raw material for sulfuric acid. The current disruption in the Strait of Hormuz has cut off approximately 50–60% of Middle Eastern sulfur shipments by sea, pushing up sulfur and sulfuric acid prices. Worth noting is that as late April 2026 progresses, sulfuric acid export restrictions combined with increased domestic production have shown signs of price softening. If sulfuric acid prices continue to decline, it will directly squeeze the comprehensive profit margins of domestic smelters. At that point, the dual pressure of persistently low TC and falling sulfuric acid prices could trigger real production cuts on the smelting side.

Although gold and silver prices do not directly determine TC trends, their macro-pricing logic as part of the non-ferrous metals sector is worth attention. The market has largely priced in the expectation that the Federal Reserve will not cut interest rates at all in 2026, with the first rate cut possibly delayed until July 2027. For copper, a delayed rate cut means no near-term easing of macro liquidity, but copper's core pricing logic remains the ongoing tug-of-war between tightening supply on the mining side and rigid demand. In other words, precious metals are under pressure, but industrial metals' pricing center remains in real supply-demand fundamentals, which explains why weaker gold and silver prices have not dragged copper prices lower.

According to SMM, for Chinese smelters, domestic copper concentrate spot TC transactions are feasible in the range of -81 USD/dmt to -88 USD/dmt. Some holders have attempted to offer TC at -100 USD/dmt, while some smelters are willing to accept deliveries at the lower end around -90 USD/dmt. The downward trend in TC has not yet stopped, and smelter purchasing activity may have weakened slightly, but not significantly.

Key areas to watch moving forward:

Sulfuric acid side: The price trend will depend on the interplay of multiple factors. First, China's sulfuric acid export policy direction: if export restrictions continue, domestic sulfuric acid supply will be relatively abundant, and prices may fall from highs; if exports are temporarily allowed, overseas hydrometallurgical copper supply risks will rise, but domestic sulfuric acid prices may find support. Second, the recovery of sulfur supply: when shipping through the Strait of Hormuz returns to normal will directly affect the pace at which Middle Eastern sulfur can supplement global markets. Third, seasonal demand changes for downstream products such as phosphate fertilizers will also cause periodic price volatility for sulfuric acid.

Mining side: Focus on the progress of the Grasberg conversion project, labor negotiation results at Chilean mines, and logistics stability at mines such as Las Bambas in Peru. Any new supply release will effectively ease TC pressure.

Macro side: Monitor the Federal Reserve's monetary policy path, the U.S. dollar index, the actual driving effect of China's pro-growth policies on copper consumption, and whether the growth rate of copper demand in global new energy sectors is slowing marginally.