In March 2026, the global steel market experienced a fierce geopolitical "sudden chill." According to the latest data from the World Steel Association (worldsteel), global crude steel production in March fell by 4.2% year-on-year to 159.9 million tons. If the decline in China's production can be attributed to an "active contraction" driven by squeezed profit margins, then the sudden plunge in the Middle East's production is a "forced paralysis" triggered by a geopolitical black swan event. The US-Iran conflict that erupted on February 28, and the subsequent blockade of the Strait of Hormuz, have completely disrupted the spring recovery rhythm of the global steel supply chain, with the shadow of energy crises and logistical interruptions rapidly spreading worldwide.

Regional Review: The "Sudden Chill" in the Middle East and CIS vs. Volume Growth in Africa and Eastern Europe

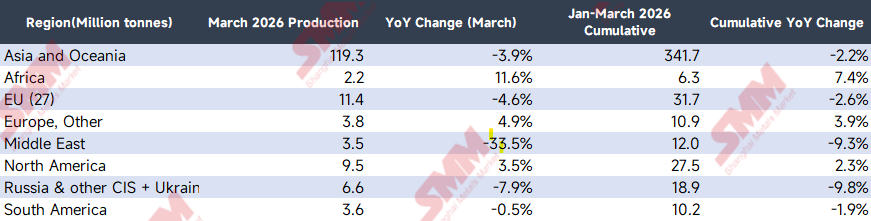

Looking at the monthly regional output, the center of gravity for global supply shifted dramatically in March.

(Data Source: World Steel Association)

Among the regional data for March, the plunge in the Middle East was the most striking. Crude steel production in this region plummeted by 33.5% year-on-year in March, recording only 3.5 million tons. The market had previously anticipated that the region would be affected by seasonal factors such as Ramadan, but the core culprit for such a massive "physical-level" production cut is precisely the sudden escalation of the US-Iran conflict on February 28 and the total blockade of the Strait of Hormuz.

- Dual Cut-off of Energy and Logistics: Iran, as the largest steel producer in the Middle East, saw its electric arc furnace (EAF) capacity—which heavily relies on the natural gas Direct Reduced Iron (DRI) process—suffer a fatal blow. The conflict led to damaged energy infrastructure or wartime rationing in the region, causing widespread gas and power outages at steel mills.

- Locked Import and Export Channels: The blockade of the Strait of Hormuz not only cut off the export routes for finished steel products from the Middle East, but more lethally, it blocked the import of scrap and related raw materials necessary to keep the region running. This forced numerous steel mills to directly declare force majeure and shut down their blast furnaces and EAFs.

Meanwhile, the decline in the CIS widened in March compared to the previous two months, reflecting that Russia's domestic construction season recovery in March fell short of expectations after its exports were hindered. The negative growth in the EU is locked in a period where energy cost fluctuations intertwine with sluggish manufacturing orders. Notably, Africa was the fastest-growing region in March, primarily driven by the release of new capacity in North Africa and local seasonal infrastructure restocking.

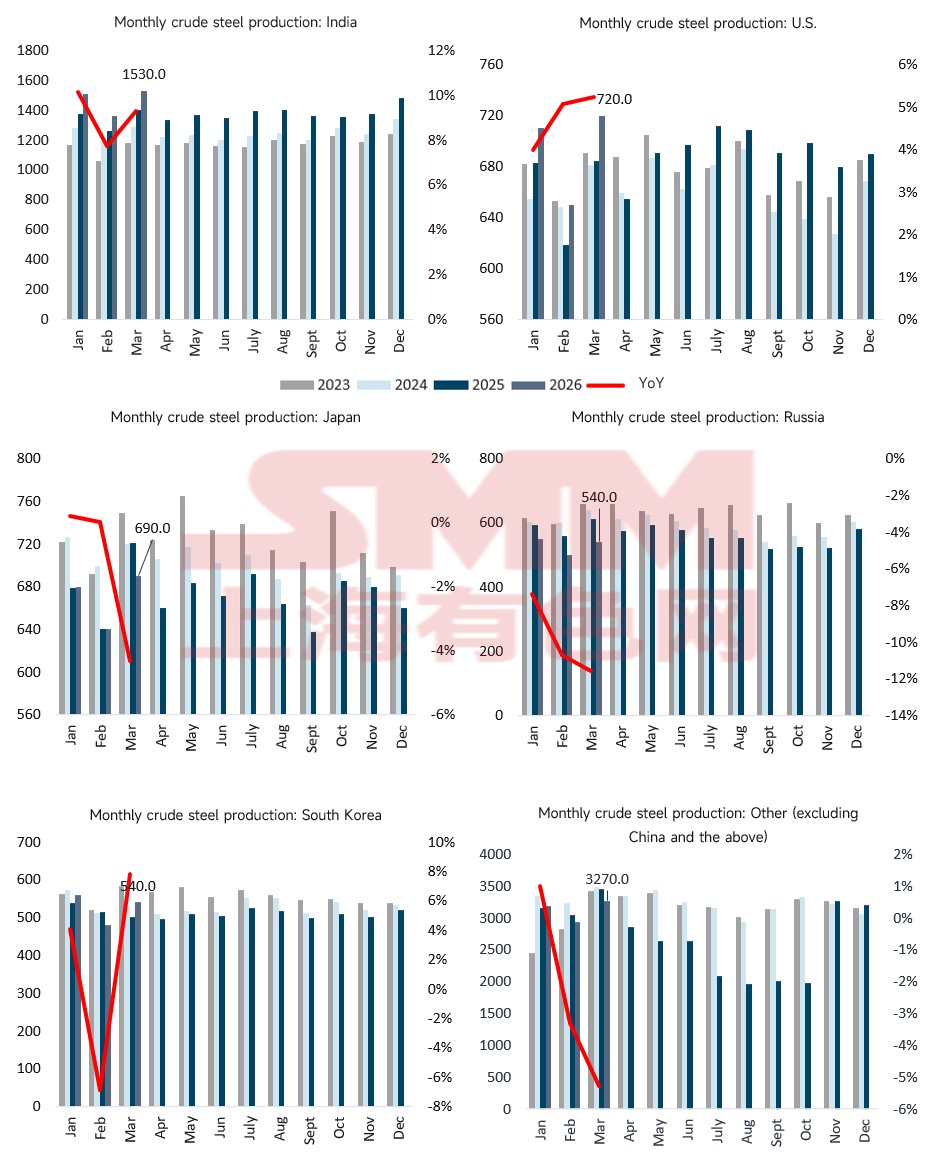

Core Country Analysis: China's Active Contraction and India's "Quarter-End Sprint"

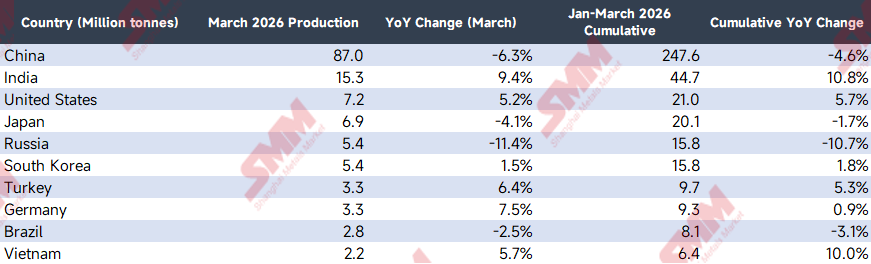

The shockwaves of the geopolitical conflict did not stop in the Middle East. Surging global energy prices and shipping freight rates, along with the complete standstill at the Strait of Hormuz, directly led to exacerbated divergence among major producing countries in March.

(Data Source: World Steel Association)

- Europe and the US (Heavy Cost Pressures and Structural Bright Spots): Despite the threat of imported energy cost inflation, the United States (+5.2%) and Germany (+7.5%) remained resilient in March. This was mainly due to seasonal production increases in their domestic automotive and high-end manufacturing sectors, as well as the continuous support of infrastructure bills; in the short term, flat product demand absorbed the pressure of rising costs. However, it is alarming that the EU as a whole (-4.6%) remains weak, indicating that the geopolitical premium has already substantially suppressed the fragile European construction sector.

- China (Active Defense at -6.3%): Facing a broad rally in commodities driven by surging crude oil, Chinese steel mills encountered soaring imported cost pressures, while the recovery of domestic end-user demand for finished steel remains in a structural transition period. Confronted with severely squeezed profit margins, domestic steel mills took the opportunity to increase maintenance and production cuts during the traditional peak season. This is a typical market-oriented defensive strategy.

- India's Capacity Surge (+9.4%): India is marching toward its national strategic target for steel capacity. In the past 2025/2026 fiscal year, new blast furnace capacities heavily invested by domestic steel giants (such as JSW, Tata, etc.) came online one after another, entering a substantive production ramp-up phase in the first quarter of this year. The massive leap in the capacity base, coupled with the pull of the fiscal year-end (March 31) sprint to meet targets, created its structural high growth in production.

- Vietnam's Rigid Demand Uptake (+5.7%): Vietnam and the ASEAN region maintained stable positive growth in March, primarily benefiting from the gradual commissioning and production ramp-up of tens-of-millions-of-tons high-end expansion projects, such as Hoa Phat's Dung Quat Phase 2. More importantly, this region is currently in a typical rapid development phase. The relatively low per capita steel stock provides huge upward elasticity, and strong local infrastructure rigid demand perfectly absorbed and digested these newly commissioned increments, maintaining an extremely high capacity utilization rate.

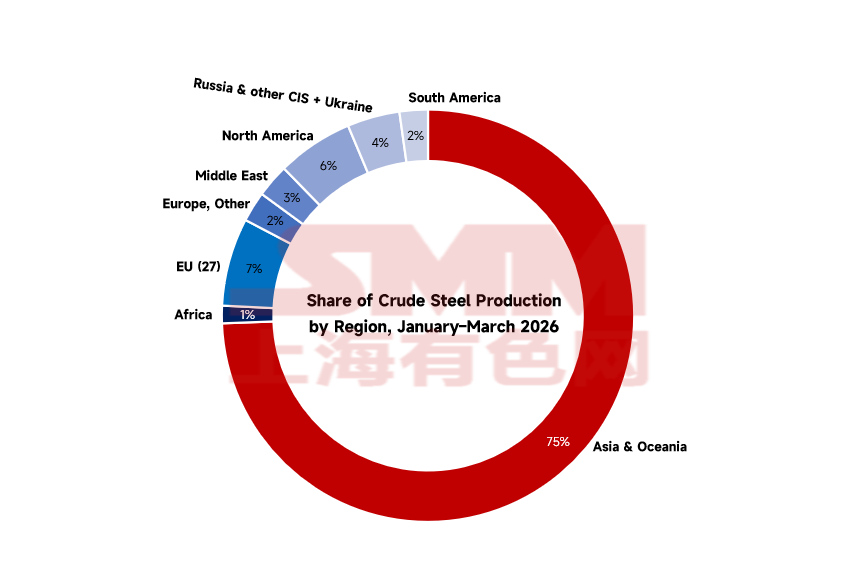

Global Trends: The Stock Game in Non-China Regions

(Data Source: World Steel Association)

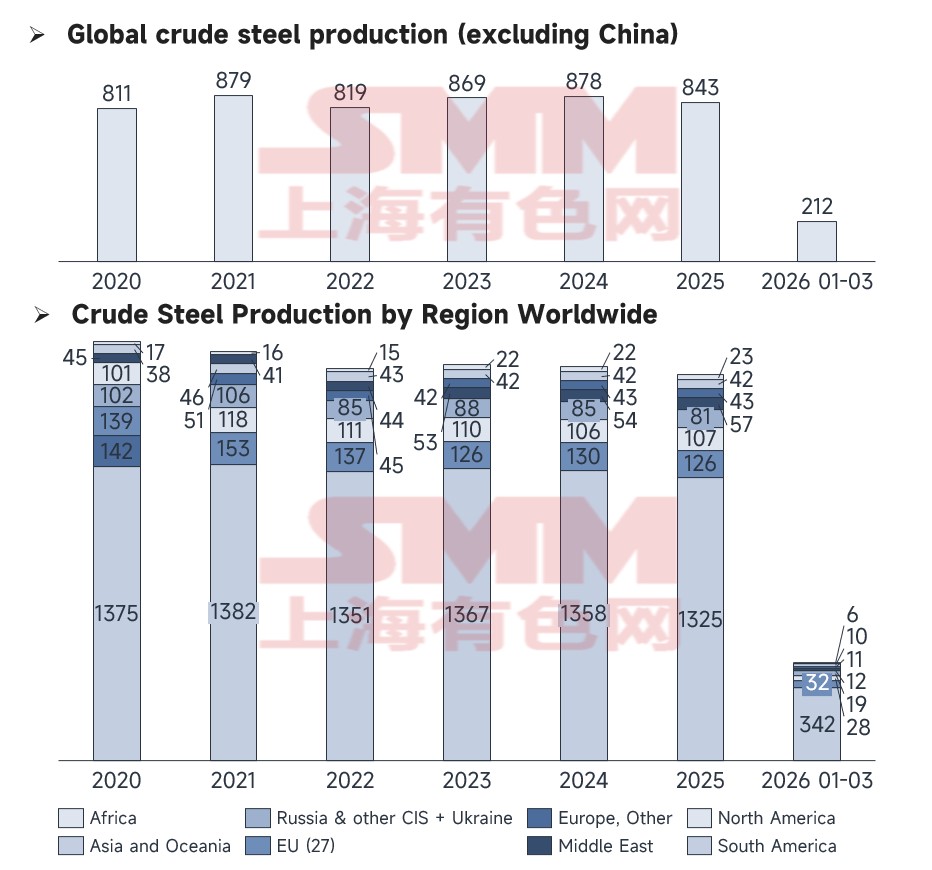

A comparison shows that global production (excluding China) in March 2026 was 212 million tons. Although it maintained the average volume level of recent years, the room for incremental growth is narrowing. The stacked structure of global crude steel production in March reveals that, apart from the absolute dominance of Asia and Oceania, stock growth in other regions is approaching its ceiling. Monthly fluctuations now depend more on the supply balance of raw materials (such as scrap steel).

Monthly Momentum Map: Breakdown of Major Market Trends

Through SMM's monthly tracking data, the real-time trajectories of various countries can be seen more intuitively.

(Data Source: World Steel Association)

- The Downward Drift of Russia and Japan: The production lines for Russia (-11.4%) and Japan (-4.1%) in March were at historic lows. Affected by the slowdown in manufacturing exports, Japan's March production curve failed to tick upward as expected.

- Counter-Trend Recovery in the US and Germany: US production in March reached 7.20 million tons (+5.2%), and Germany reached 3.30 million tons (+7.5%). This is largely due to seasonal production hikes in the automotive and high-end equipment manufacturing industries in both countries during March, which drove short-term volume releases in flat product demand.

- Turkey's Export Rebound: Turkey's production rebounded (+6.4%) in March, largely capitalizing on the international trade gap left by Russia's production cuts.

April Outlook: Intensified Tight Balance and the Safe-Haven Effect of "Exchange Rate Purchasing Power"

Looking ahead to April 2026, the continuation of the Strait of Hormuz blockade and war premiums will keep global crude steel production under sustained pressure, profoundly altering the market's operational logic.

- Irreplaceable Middle East Gap and the Extreme "Tight Balance" of Global Scrap Steel: As the conflict continues, the Middle East is highly unlikely to achieve an effective capacity recovery in April, which will leave a massive regional supply gap. Even more severely, global scrap steel resources are already in a long-term tight balance. With the Middle East cut off as an important scrap flow node, EAF steel mills in Turkey, South Asia, and even Europe and the US will be forced to compete for scrap resources globally at high prices. The skyrocketing price of scrap will relentlessly erode the profits of overseas EAF steel mills, becoming the absolute "ceiling" for production expansion in regions outside the Middle East in April.

- Southeast Asia: Rigid Demand and Exchange Rate Dynamics in a Rapid Development Phase: Facing high energy costs and global supply chain restructuring, the ASEAN region (ASEAN-4, Vietnam, etc.) demonstrates a unique market position. This region is currently in a typical rapid development phase. Its relatively low per capita steel stock, combined with the undertaking of industrial transfers, provides an undeniable rigid demand for local infrastructure and factory construction. Under the turbulent conditions expected in April, the core variable for this region will focus on the exchange rate. Amid capital flows triggered by the geopolitical crisis, if the local currencies of buying countries like the Malaysian Ringgit and Thai Baht can maintain a relative appreciation against the US dollar, it will substantially increase their actual USD purchasing power. This enhanced purchasing power can effectively hedge against the USD-denominated cost of imported steel, thereby securing the inventory-building capacity of regional processing plants and traders for overseas billet and hot-rolled coils (HRC). This positions ASEAN as a rare, stable ballast in the global steel trade flow in April.

Conclusion: In the spring of 2026, the steel industry is no longer just about the interplay of supply and demand curves. The blockade of the Strait of Hormuz has completely torn apart the old trade balance. Global output in April will have to find a difficult new equilibrium amid the multi-directional pulls of high energy costs, extremely scarce scrap resources, and the exchange rate purchasing power of emerging markets.

![[SMM Hot-Rolled Coil Inventory at Zhangjiagang Port] The decline in Zhangjiagang port inventories slowed down this week.](https://imgqn.smm.cn/usercenter/fvyjO20251217171715.jpg)

![[SMM Iron & Steel] India's SEPC Limited Wins 71.13 Million USD Contract for SAIL's IISCO Mill Expansion](https://imgqn.smm.cn/usercenter/gmcdk20251217171720.jpg)