Nickel Ore

This week, the price of domestic nickel ore in Indonesia has increased. In the second half of April, the Indonesian nickel ore benchmark price (HPM) was set at $16933.6 per dry metric ton, a month-on-month decrease of 0.93%. According to SMM's Indonesian nickel ore premium data, the average premiums for laterite nickel ore with grades of 1.4%, 1.5%, and 1.6% were reported at $40, $44, and $44.5 per wet metric ton respectively. Among them, the domestic arrival price for 1.6% grade nickel ore was $69.2–80.2 per wet metric ton. The dual strengthening of premiums this month reflects the release of smelters' restocking demand and pessimistic expectations regarding the reduction of RKAB quotas. Meanwhile, the delivery price of 1.2% grade hydrometallurgical ore has also increased to $27–33 per wet metric ton. Despite the significant overhaul of the HPM formula, which now incorporates byproduct contents such as iron, cobalt, and chromium, the market remains in a state of transition ("wait and see" mode). Because the new formula sharply increases the calculated base price for both saprolite and limonite, most smelters are pushing back and rejecting these concepts of premium until the end of April. They currently favor the "Old HPM + Premium" pricing mechanism to maintain cost stability. Due to the sudden nature of this regulatory rollout, smelters have had little time to adjust their internal pricing mechanisms or renegotiate premium structures. Consequently, market transactions have remained stable, with no new trades yet reported using the updated multi-element formula.

- Pyrometallurgical Ore:

From the perspective of supply and demand fundamentals, key mining hubs, including Morowali and Konawe, have shifted to predominantly cloudy conditions this week, stepping back from continuous heavy downpours. However, local humidity is still expected to approach a saturation level of 99%. Under the combined effect of active atmospheric waves and thick, persistent cloud cover, the lack of direct sunlight and the extremely humid environment will continue to constrain the ore-drying efficiency of open-pit mines. This slow evaporation rate continues to hamper logistics and transportation, further exacerbating the operational difficulties of high-moisture management during the shipping of laterite nickel ore.

Furthermore, the market is facing a clear trend of declining ore grades, although saprolite grades in the Sulawesi region remain relatively higher than those in Halmahera. While some NPI smelters have begun accepting ore with grades of 1.45% and below, pyrometallurgical ore supply remains exceptionally tight in April.

- Hydrometallurgical Ore

Additionally, limonite ore transactions have been sparse. Following the significant price hikes for pyrometallurgical ore, limonite prices have also edged up, which miners hope will stimulate sales. However, a major pricing disparity has emerged: the newly calculated HPM for limonite now exceeds the final CIF market price. Consequently, although miners continue to push for higher prices, most smelters are aggressively negotiating to keep purchase prices below the new HPM, thereby holding actual limonite transaction prices stable at previous levels

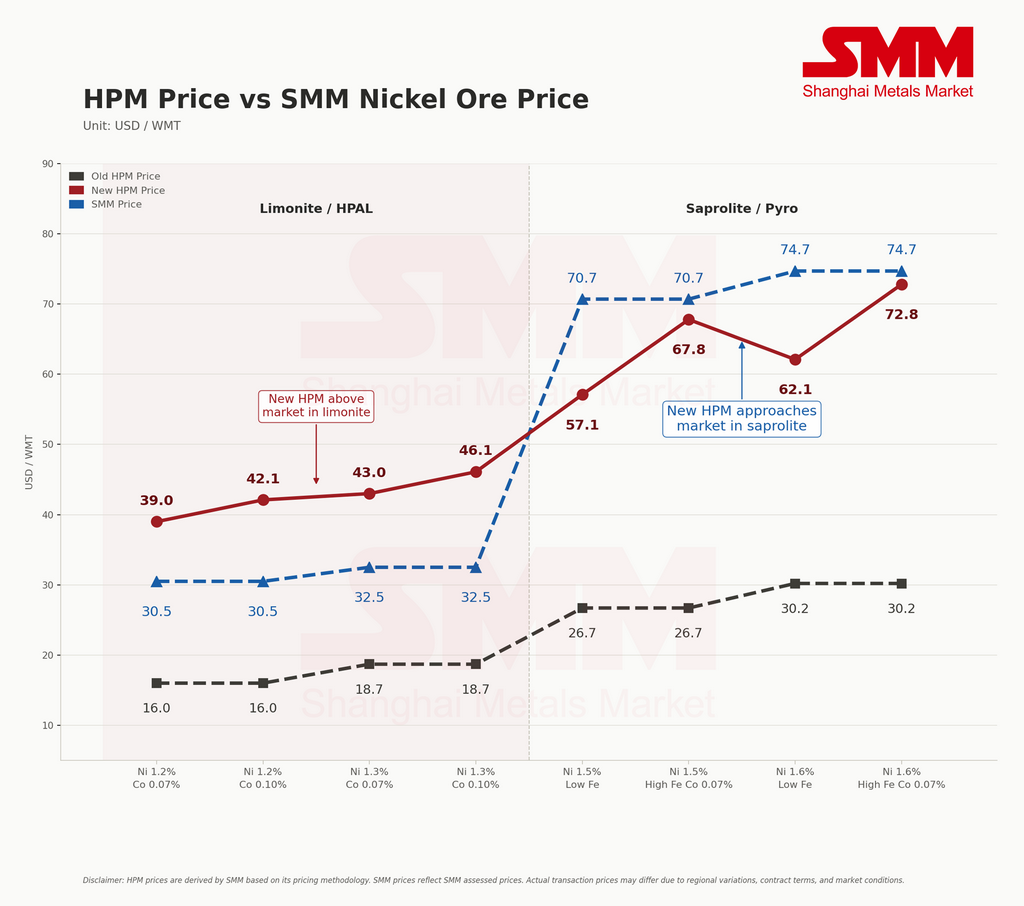

HPM Price Outlook (SMM's Internal Assumption)

With three byproduct elements now factored into the nickel ore pricing formula, we observe a diverging impact on the calculations for saprolite and limonite. Overall, the new HPM-derived price for limonite is tracking higher than SMM's assessed market price. Conversely, while the prevailing market price for saprolite remains above the official benchmark, the gap between the two is steadily narrowing.

Regulatory & Quota Outlook (RKAB)

Director General of Minerals and Coal Tri Winarno has stated that the Ministry of Energy and Mineral Resources (ESDM) is still actively processing the 2026 Work Plans and Budgets (RKAB) for mineral and coal commodities, with approval progress reaching approximately 90% by mid-April. At present, some mining enterprises have received preliminary notices from the government regarding their latest quota indicators, but most have yet to obtain the final approved data. The market generally expects the 2026 RKAB quotas to be officially finalized by the end of April.

In terms of demand, due to the resource uncertainty faced by smelters in Indonesia and the ongoing difficulty in securing high-grade nickel ore, prices have maintained a strong performance. To ensure steady raw material supply, some smelters have even begun offering increased trade bonuses and premiums to secure cargoes.

Nickel Pig Iron

"High-NPI Market Dips Before Rebounding Amid Demand Recovery and the Impact of Indonesia's New HPM Policy"

The average price of SMM 10-12% NPI average price dropped by RMB 5.15 per nickel unit week-on-week to RMB 1085.4 per nickel unit (ex-works, tax included), while the Indonesia NPI FOB index increased by USD 1.5 USD per nickel unit to an average of USD 138.51 per nickel unit. High-grade NPI (Nickel Pig Iron) market conditions generally remained steady.

This week, the high-NPI market exhibited a "dip before rebounding" trend. Early in the week, prices fell slightly due to sluggish terminal demand. However, subsequently driven by multiple favorable factors, market activity increased significantly, and the price center gradually shifted upward. Mid-week, Indonesia's new HPM policy was rolled out, causing a sharp surge in the nickel ore HPM price. This bolstered upstream smelters' willingness to hold firm on prices. Simultaneously, supported by the continuous rise in nickel prices, traders' willingness to support prices and purchase goods was also stimulated.

On the demand side, as the futures market moved significantly higher, stainless steel spot prices followed suit, and scrap steel prices also rose. With downstream profit margins and economic viability recovering, steel mills' acceptance of high-NPI prices increased synchronously, leading to a month-on-month growth in market transaction activity. In summary, supported by costs and the recovery of market activity, the high-NPI price center has moved higher. Looking ahead, backed by cost support and a tight supply-demand balance, high-NPI prices are expected to continue their upward trajectory.

![[SMM Stainless Steel Flash] Asian Stainless Steel Prices Hold Steady for Third Consecutive Week Amid Quiet Market](https://imgqn.smm.cn/usercenter/NHXhQ20251217171733.jpg)