SMM April 14:

Since the joint U.S.-Israeli airstrikes on Iran on February 28, tensions in the Middle East have persisted for 45 days. In terms of recent openings, the Strait of Hormuz was briefly opened for several hours on April 8, but due to Israeli airstrikes on Hezbollah in Lebanon, it was fully closed again that afternoon, with shipping disruptions continuing to this day. Against this backdrop, China's die-casting zinc alloy market has been affected to varying degrees in terms of costs, demand, and industrial structure. The following is a detailed analysis.

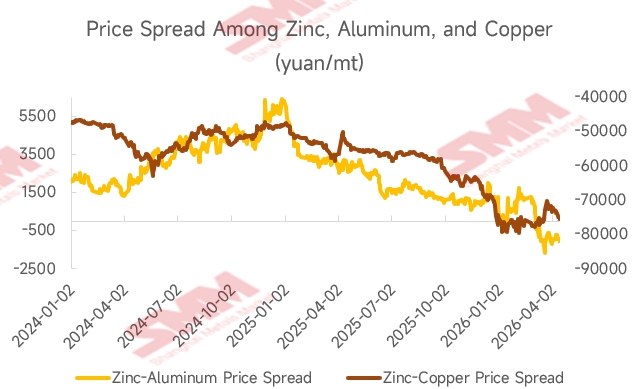

Since the escalation of tensions in the Middle East, the amplitude and frequency of non-ferrous metal price fluctuations have increased significantly, directly affecting the production costs of die-casting zinc alloy enterprises. According to SMM's 2026 data comparison, the average zinc-aluminum price spread and zinc-copper price spread before the tensions escalated (January 5, 2026 – February 27, 2026) were 778 yuan/mt and -77,224 yuan/mt, respectively. From March 2 to this Monday (April 13), the zinc-aluminum price spread shifted to -751 yuan/mt, while the zinc-copper price spread stood at -74,428 yuan/mt. Among these, the impact on Zamak #3 is more notable — the zinc-aluminum price spread turned from positive to negative, meaning that at the same zinc price level, the relative cost of aluminum has risen, directly pushing up the raw material costs for enterprises producing Zamak #3.

Second, it was reflected in demand:

In terms of domestic demand, affected by wild swings in prices, upstream and downstream enterprises generally adopted a strategy of restocking on dips. Purchase willingness declined notably when prices were high, which in turn affected the operating levels of the die-casting zinc alloy industry. In segmented sectors, luggage zipper hardware exhibited certain peak-season characteristics, and daily-use hardware such as auto parts gradually recovered. However, overall domestic demand performance was largely suppressed by prices.

External demand: The contraction of end-user hardware orders in the Middle East directly dragged down export demand from some end-user hardware factories in south China and east China, making it the most direct variable on the consumption side of die-casting zinc alloy in this round of impact.

Outlook for Short-Term and Medium and Long-Term Impact on Enterprises

- The trading proportion of die-casting zinc alloy factories in China is expected to increase. Affected by rising raw material costs for production, domestic alloy factories may increase the volume of externally purchased mainstream #3 and #5 alloys to protect their interests, redirecting their own production lines toward customized, high-value-added alloys to maintain profit margins.

- If short-term tensions are not effectively resolved, the cancellation or suspension of export orders from the Middle East is expected to become the norm, continuously impacting demand for domestic alloy factories.

- However, if tensions ease, post-war demand replenishment is expected to provide certain medium and long-term support for the consumption of die-casting zinc alloy factories in China.

![SHFE Zinc Slightly Recovers [SMM Zinc Morning Comment]](https://imgqn.smm.cn/usercenter/qdibi20251217171755.jpg)

![U.S.-Iran Tensions Fluctuate, LME Zinc Center of Gravity Shifts Downward [SMM Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/CGlrd20251217171755.jpg)