SMM Apr 13 News:

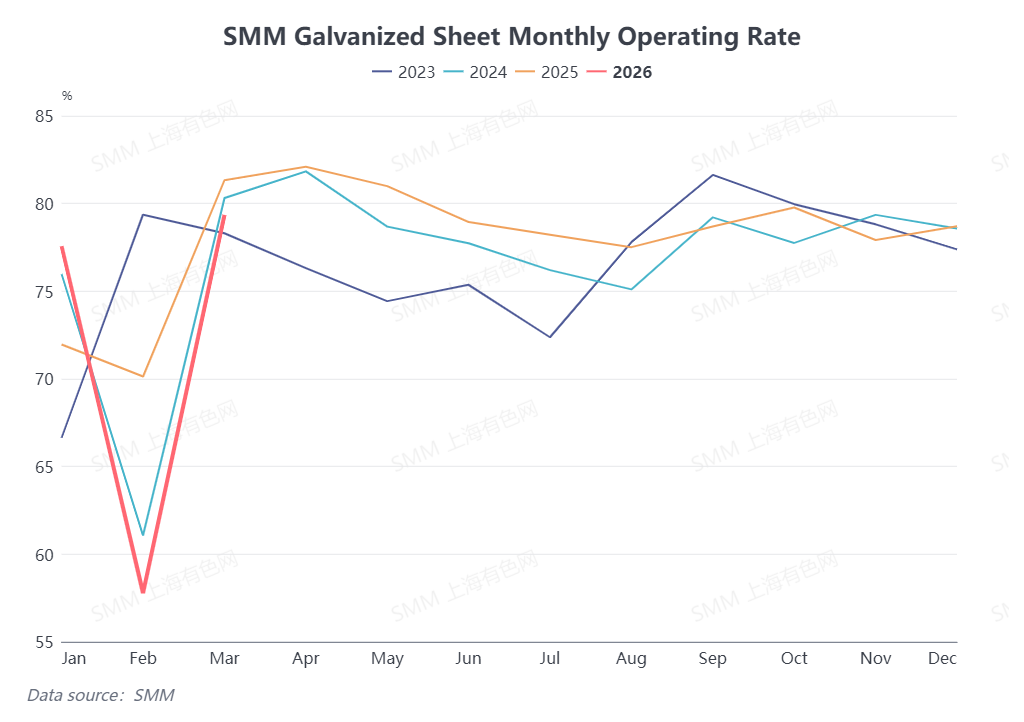

Q1 has ended. From an order perspective, January orders weakened seasonally, February coincided with the Chinese New Year holiday when most galvanized sheet producers in China were on holiday, and although galvanized sheet enterprises gradually resumed operations in March, overall utilization rates were lower than last year on a YoY basis. Q1 galvanized sheet orders in China were somewhat mediocre. What are the expectations for Q2?

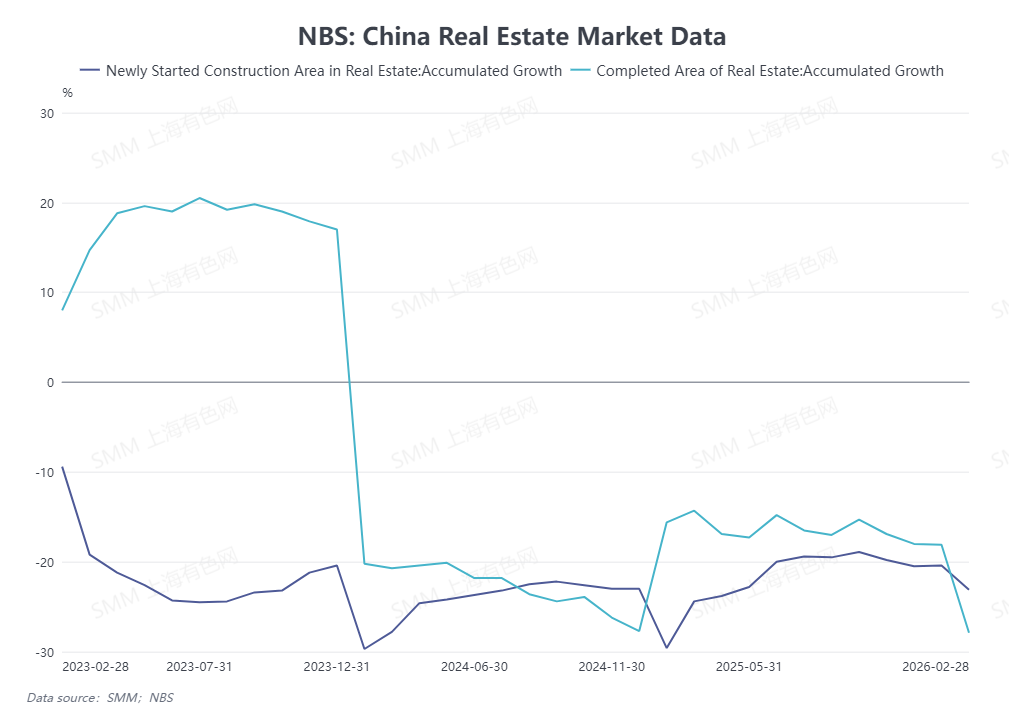

Construction sector. In Q1 this year, cumulative YoY new construction starts and completions in real estate continued to maintain negative growth, and the related demand decline continued to drag down construction galvanized sheet orders in China. It is understood that orders performed poorly from January to February due to the off-season and holiday. In March, end-user projects in China gradually commenced, but the overall recovery pace was slow, and March galvanized sheet orders underperformed compared to last year. Looking ahead to Q2, domestic consumption in April is expected to continue improving from March with more construction sheet orders, while June is a typical plum rain season. Overall Q2 orders are expected to increase first and then decrease.

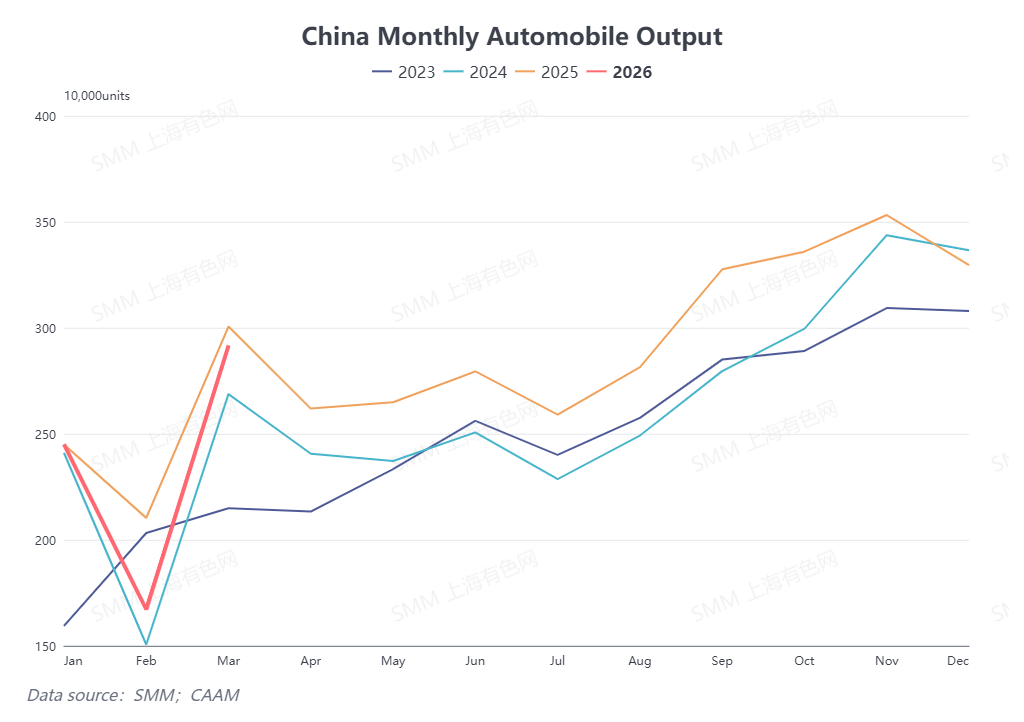

Auto sector. According to CAAM data, from January to March 2026, China's auto production and sales reached 7.039 million units and 7.048 million units respectively, down 6.9% and 5.6% YoY respectively. Among them, NEV production and sales were down 6.8% and 3.7% YoY respectively, with NEV sales accounting for 42% of total new vehicle sales. Q1 auto production and sales underperformed compared to the same period last year, likewise affecting related auto sheet demand. Looking ahead to Q2, auto production and sales data are typically relatively stable in Q2, and related auto sheet orders are expected to run steadily.

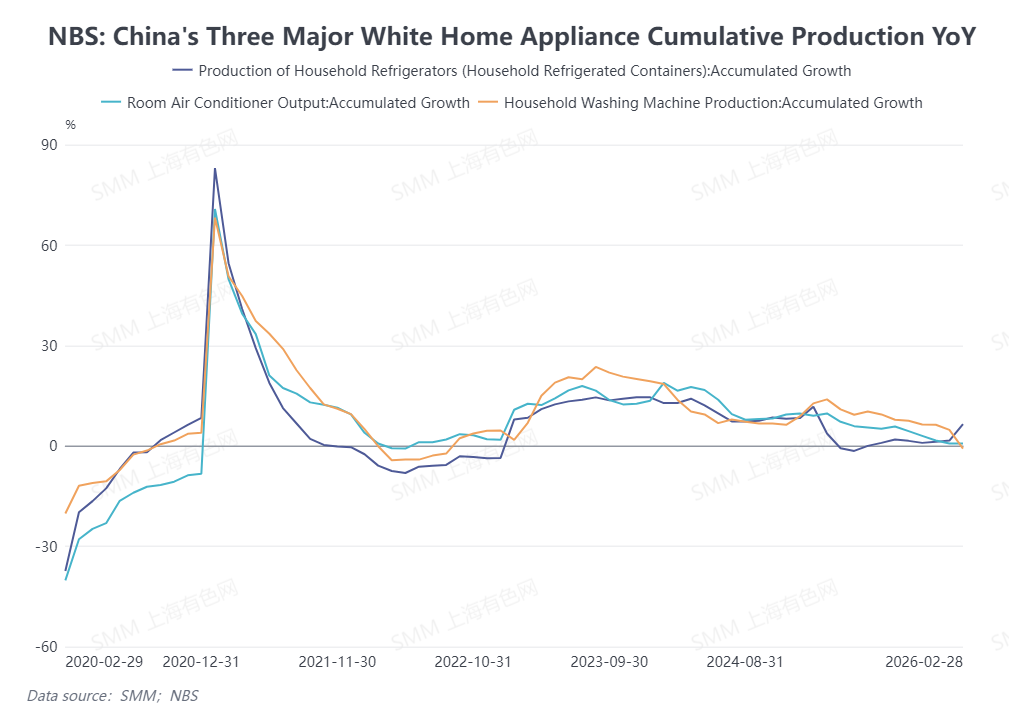

Home appliance sector. From January to February 2026, cumulative production of household refrigerators was up 6.5% YoY, air conditioners up 0.7% YoY, and washing machines down 0.8% YoY. Q1 home appliance production showed mixed results, with overall order performance being moderate, and end-use demand continued to boost galvanized sheet orders. Typically, April to May remains the peak season for home appliance production and sales in China, but the subsequent arrival of summer is expected to affect home appliance factory production. Q2 home appliance galvanized sheet orders are expected to be strong first and then weaken.

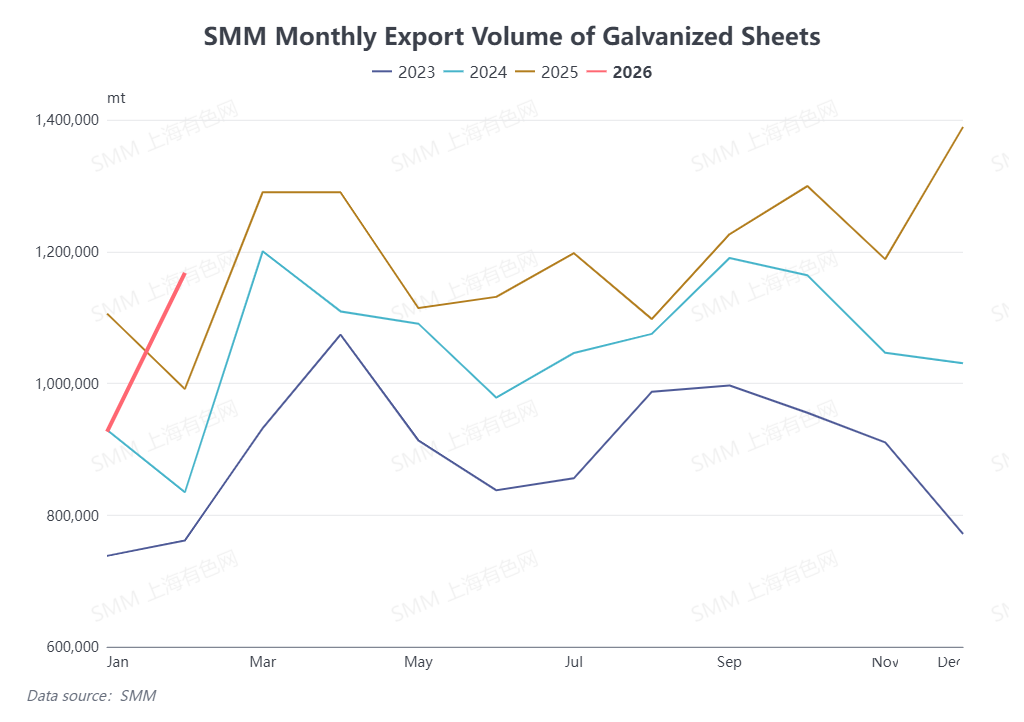

Export side. According to General Administration of Customs data, galvanized sheet exports in January 2026 were 926,600 mt, and in February were 1.1677 million mt. Cumulative exports from January to February totaled 2.0942 million mt, down 0.14% YoY cumulatively. China's total galvanized sheet exports from January to February this year were basically flat with last year. For Q2, although recent Middle East tensions have affected some export demand, with related orders in March and April being impacted, considering that demand in Southeast Asia remains robust, Q2 galvanized sheet exports are not expected to see a notable pullback.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)