China's benchmark stainless steel futures contract posted a solid recovery in the first trading week after the Qingming holiday, driven primarily by improved macro sentiment rather than any meaningful shift in underlying demand. The SS2605 contract (May 2026 delivery on the Shanghai Futures Exchange) closed at RMB 14,470/mt (approximately $2,103/mt) on April 10, up RMB 320/mt (roughly $47/mt) from the pre-holiday close of RMB 14,150/mt ($2,056/mt). The rebound, however, was largely a futures market story. Physical spot prices struggled to keep pace, reflecting a market that remains structurally pressured by high production output, elevated inventory, and a cost floor that continues to erode.

Macro Catalysts Do the Heavy Lifting

Two developments drove the week's sentiment recovery. The first was domestic: China's central bank, the People's Bank of China (PBOC), conducted an RMB 800 billion (approximately $116 billion) three-month outright reverse repo operation on April 7, a liquidity injection that significantly exceeded market expectations. The operation was designed to shore up medium-term liquidity in the banking system at the start of the second quarter, and it had an immediate stabilizing effect on commodity market sentiment.

The second was geopolitical: the United States and Iran reached a two-week ceasefire agreement and opened formal negotiations, easing near-term fears of a sustained energy price shock. The de-escalation removed a key source of macro anxiety that had weighed on industrial metals over the preceding weeks.

Offsetting these positives, however, was a hawkish signal from the U.S. Federal Reserve. Minutes from the March FOMC meeting revealed that more officials had begun discussing the possibility of rate hikes, and commentary from influential Fed-aligned market observers reinforced the view that the central bank remains on guard against persistent inflation. This tempered enthusiasm for non-ferrous metals and applied some pressure on longer-term valuations across the base metals complex.

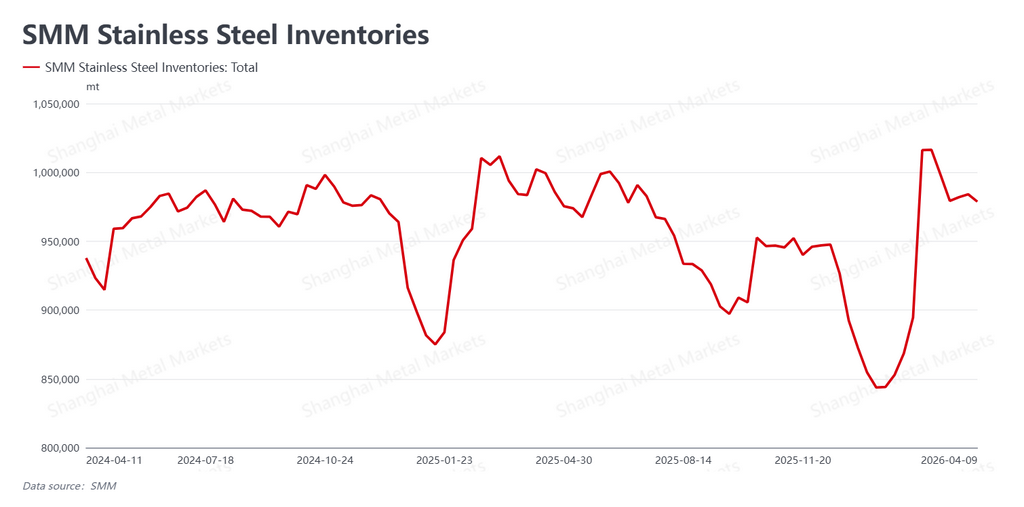

Inventory Dips, But the Structural Overhang Remains

According to Shanghai Metals Market (SMM), social inventory (warehoused stainless steel held outside of mills) fell to 978,000 metric tons this week, down 0.55% from the prior week and pulling back from the psychologically significant one-million-ton threshold. The drawdown was driven largely by the release of orders that had accumulated during the Qingming holiday and a pick-up in inquiry activity in the days immediately following the break.

The improvement, though welcome, was not enough to signal a genuine demand acceleration. Overall transaction volumes have not shown the kind of momentum that typically defines a strong "Silver April" buying season. In the spot market, major mills held their guidance prices steady, and while intraday trading activity among distributors improved modestly, procurement remained largely need-based. Buyers are restocking to minimum operational levels rather than building inventory in anticipation of higher prices.

The challenge ahead is on the supply side. Mill production schedules for April remain elevated, meaning a significant volume of new supply is expected to hit the market in the second half of the month. Whether the current pace of inventory drawdown can be sustained against that backdrop is an open question, and most market participants are watching closely.

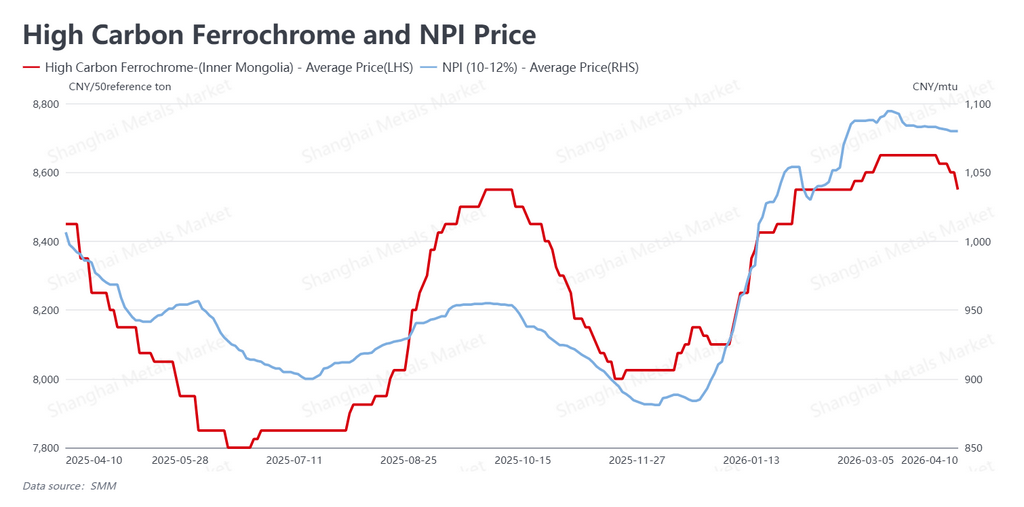

Raw Material Prices Keep Sliding, a Double-Edged Development

On the cost side, Nickel Pig Iron (NPI), the primary nickel feedstock for Chinese stainless steel producers, continued its gradual decline to RMB 1,080 per nickel point (approximately $157/nickel point) as of April 10. High-carbon ferrochrome eased further to RMB 8,550/50-base-ton (approximately $1,243/50-base-ton).

The downward drift in raw material prices reflects the relentless pressure that stainless steel mills have exerted on their suppliers. With spot stainless prices chronically failing to cover production costs, mills have strong incentive to force concessions upstream, and they are succeeding. The irony is that while lower input costs provide some relief to squeezed mill margins, they simultaneously weaken the price floor beneath stainless steel. A market that previously could point to firm NPI and ferrochrome prices as a reason futures could not fall further below a certain level is now losing that argument. The cost floor is softening, and with it, the downside protection.

Outlook: Emotion vs. Reality

The week's dynamic can be summarized as a tug-of-war between improving macro sentiment and stubborn physical market realities. The geopolitical calm and PBOC liquidity injection gave futures traders reasons to buy. But the spot market, where physical tons change hands at real prices with real demand signals, has not confirmed the optimism.

Looking ahead, the two dominant variables will be the trajectory of U.S.-Iran negotiations and any further signals from the Federal Reserve on rate policy. If diplomacy stalls or the Fed turns more explicitly hawkish, the macro lift that carried prices this week could unwind quickly. On the fundamental side, the key question is whether post-holiday restocking translates into a steeper inventory drawdown in the coming weeks. If it does not, the risk is that futures prices, now pressing toward RMB 14,500/mt, run into a wall of unsupported supply and retreat. A rally that outpaces the physical market rarely holds for long.

Written by: Bruce Chew | Nickel & Stainless Steel Analyst | bruce.chew@metal.com | +601167087088