SMM April 9:

Currently, international geopolitical conflicts have seen repeated fluctuations, and commodity prices have also experienced intensified volatility. How will zinc prices trend under different geopolitical conflict scenarios? What variables need to be monitored in the short term?

I. Macro Path: Closely Monitoring "Inflation-Interest Rates-US Dollar" Dynamics

1. Logic for the trend under geopolitical conflict de-escalation:

Conflict easing → risk aversion cooling → industrial metals risk appetite rebounding → zinc prices rebounding with a short-term upward bias.

Conflict easing → inflation cooling → interest rate cut expectations restarting, US dollar weakening → bullish for zinc prices.

2. Logic for the trend under geopolitical conflict escalation:

Conflict escalation → risk aversion rising → industrial metals risk appetite declining → zinc prices under pressure.

Conflict escalation → pushing oil prices higher, intensifying inflation concerns → market expectations for interest rate hikes strengthening, suppressing consumption → bearish for zinc prices.

II. Fundamental Path: Closely Monitoring "Energy-Ore, Smelting Transportation and Production-Demand"

1. Fundamental implications of geopolitical conflict de-escalation:

Transportation: The Strait of Hormuz reopens, shipping resumes, transportation time and costs decline, zinc ore from the Middle East flows in normally, zinc concentrates inflows to China increase, providing support for TC, while smelters replenish raw materials, costs decline, production increases, and zinc prices encounter resistance.

Costs: Geopolitical conflict easing leads to energy prices normalizing, production and transportation costs for ex-China zinc concentrates declining, miner profits increasing, and production rising. Since electricity costs account for roughly 30%-40% of smelter costs, and smelters in Southeast Asia, Europe, and other regions outside China are highly dependent on energy imports, easing of conflicts alleviates pressure on electricity costs and supply, reducing production reduction risk at smelters. Overall supply-side increases put downward pressure on zinc prices to some extent.

Consumption: After conflict easing, pressure from the global economic slowdown diminishes, exports of galvanized sheet from China to the Middle East (accounting for approximately 15% of China's total exports) increase, and export orders improve. Additionally, reconstruction plans that follow conflict resolution are launched, consumption in infrastructure and other sectors increases, driving improvement in zinc consumption and supporting zinc prices. 2. Fundamental analysis under geopolitical conflict escalation:

Essentially the opposite of conflict de-escalation, the supply side would see surging transportation and cost pressures. Transportation and production of ores outside China would be disrupted, with Middle Eastern ores stranded and ex-China mines facing energy shortages, potentially leading to production cuts or shutdowns due to fuel unavailability. Meanwhile, smelter costs would surge sharply. If the conflict persisted, smelters in Japan, South Korea, India, Europe, and other regions would face energy shortage pressures. In addition, raw material ore supply would also be constrained, TCs would continue to decline, and smelters could potentially cut or halt production. Newly planned projects would likewise be delayed. Under supply-side tightness and low LME inventory, structural risks would increase and zinc price support would strengthen. However, the consumption side would be clearly under pressure, with rising global stagflation pressures and slowing consumption growth, putting zinc prices under pressure.

III. Overall, the key areas requiring close attention for zinc currently are:

Geopolitical conflicts fluctuated frequently, macro sentiment shifted rapidly, widening the fluctuation range of zinc prices. Attention should be paid to changes in geopolitical conflicts.

Zinc concentrate shipments from Australia after typhoons and floods, and the volume of Middle Eastern zinc concentrate inflows after the brief opening of the Strait of Hormuz: Transportation in Australia has returned to normal, and zinc concentrates have flowed out of the Middle East within the month, but the volume and subsequent shipment conditions still require attention. Additionally, the specific implementation of subsequent imported ore import standards still needs monitoring.

Overseas mine and smelter profitability and production under rising energy costs: Although there is no confirmed news of mines cutting or halting production due to energy shortages, at the current LME zinc price near $3,300/mt, some small mines face significant overall cost pressure. Rising energy costs undoubtedly put pressure on mine production release. Combined with force majeure events and declining raw ore grades, overseas ore production is expected to face YoY decline risks within the year. Smelting side, overseas smelters' raw material supply is primarily based on long-term contracts, but raw material pressure is also increasing amid expectations for production cuts. Meanwhile, electricity prices have risen and cost pressure has increased. Recently, Nyrstar's Auby and Budel zinc smelters underwent maintenance, putting European smelting production under pressure. Going forward, production conditions at smelters in Japan, South Korea, India, and other regions still need monitoring.

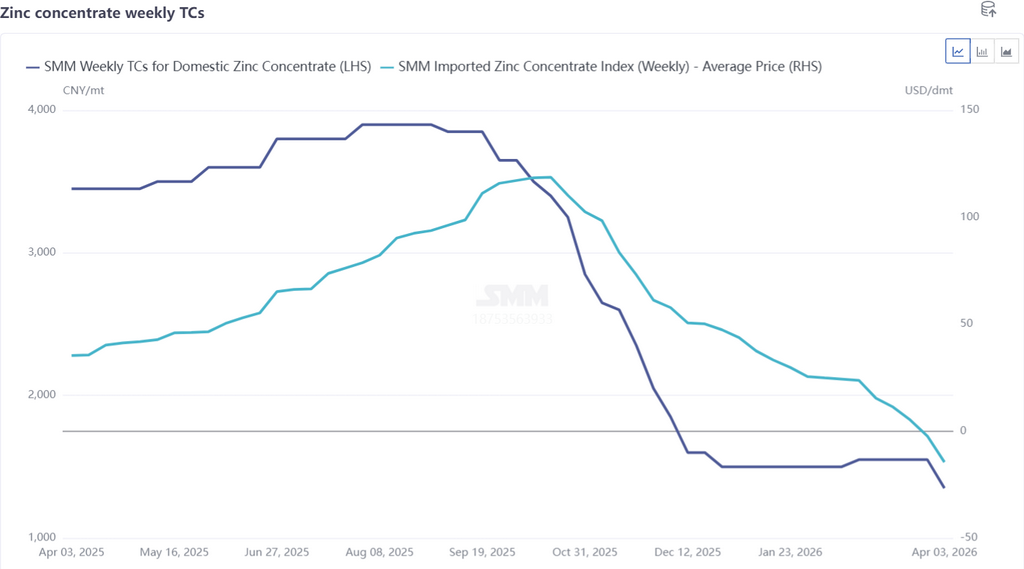

Strengthening expectations for TC declines: As of April 3, SMM's weekly imported ore TC had fallen to -$12.22/dmt. Meanwhile, supported by by-product profits, domestic smelters' April production is still expected to increase, driving strong demand for ore. Enterprises primarily rushed to purchase domestic ore, and weekly domestic ore TC was cut to 1,350 yuan/mt in metal content. Against the backdrop of tight raw materials, attention should be paid to the maintenance progress of domestic smelters. If smelters undergo concentrated maintenance and production cuts, it would strengthen the floor support for TC, while reduced supply would provide upward momentum for zinc prices.

Inventory changes: LME inventory at low levels and China's social inventory at high levels are in a tug-of-war. Currently, LME inventory stands at a low level of around 110,000 mt. Coupled with concerns over overseas smelter production cuts, cancelled warrants once surged by 300%. Although no significant destocking has been observed yet, structural risks on the LME remain a concern. In China, smelter production remained at high levels while downstream consumption fell short of expectations. Social inventory briefly destocked before turning to accumulate above 250,000 mt. If consumption does not improve further, inventory will be difficult to draw down.

Overall, given the frequent reversals in macro sentiment and the widened fluctuation range of zinc prices, fundamentals side, zinc prices have relatively strong floor support, but unilateral positioning is not advisable. Attention should be paid to potential shifts in the market's core contradictions at any time.

Data Source Disclaimer: Data other than publicly available information is derived by SMM based on public information, market communication, and SMM's internal database models, and is for reference only and does not constitute decision-making advice.