Recently, the brass billet industry has been facing the dual test of elevated raw material costs and diverging market demand. According to SMM, affected by the continued rise in recycled brass raw materials prices, the industry's overall operating rate edged up slightly, but enterprises' willingness to stockpile declined markedly, and wait-and-see sentiment remained strong in the market.

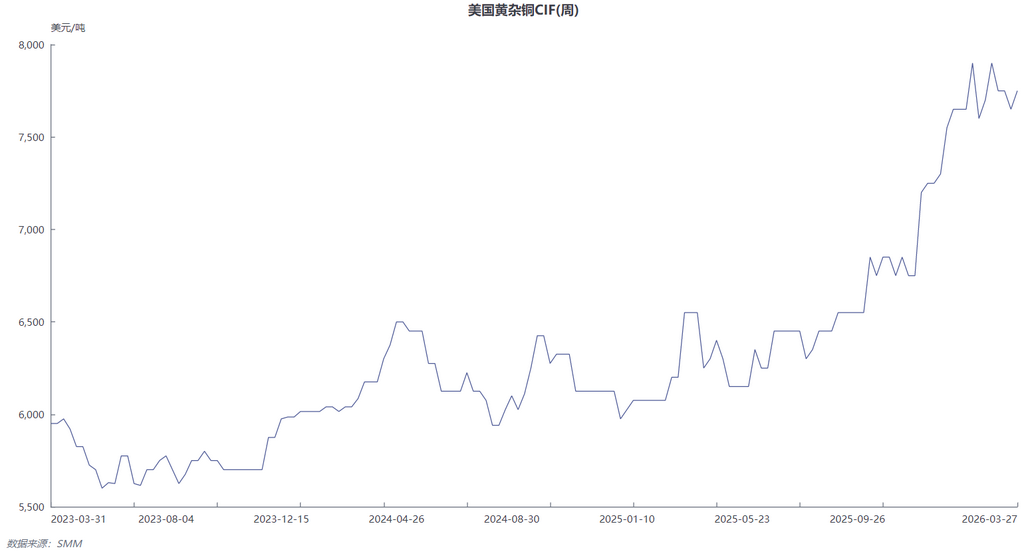

Raw Material Prices Stay High, Enterprise Cost Pressure Becomes Prominent: As of the week of March 27, the weekly CIF China quote for US brass scrap had risen to $7,750/mt. Recycled brass raw materials prices stayed high, and overall spot circulation in the market remained tight. High raw material costs made brass billet enterprises more cautious in their procurement strategies, with stockpiling willingness weakening significantly. Some enterprises told SMM that current secondary brass prices were no longer economical, and that “directly purchasing copper and zinc for blended production is actually more cost-effective.” This phenomenon reflected that under high copper prices, the logic of raw material substitution was gradually changing enterprises' purchasing behavior.

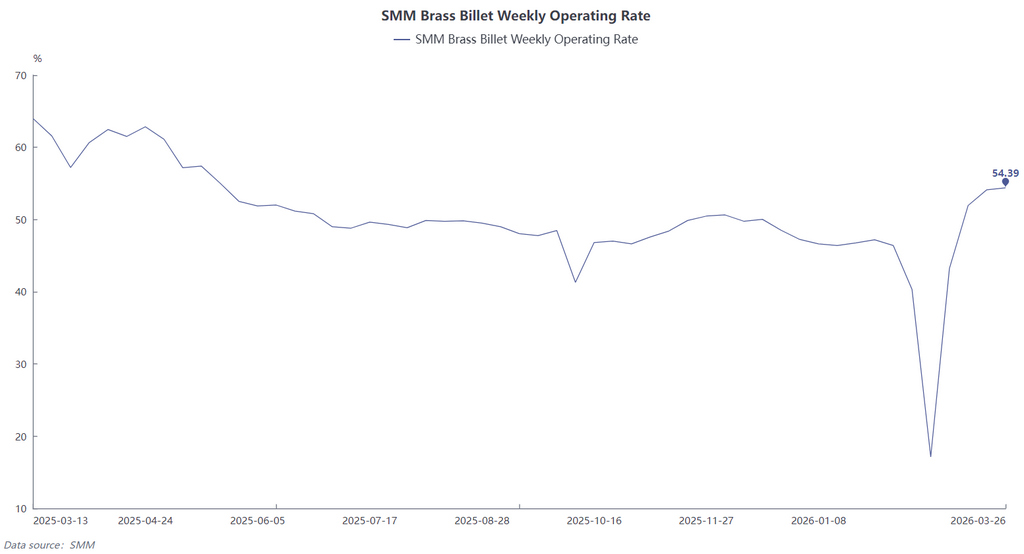

Operating Rate Increased Slightly, but Demand Divergence Was Clear: Despite significant pressure from the cost side, overall industry operations remained mild. Data showed that as of March 26, the operating rate of China's brass billet industry stood at 54.39%, up 0.26 percentage points MoM. This slight increase was mainly supported by demand from some downstream segments.

From the segmented market perspective, demand in the refrigeration valve fittings sector remained steady and improving, becoming the core driver supporting current brass billet enterprises' production schedules. By contrast, orders in traditional general-use sectors such as hardware and plumbing were relatively stable, with most enterprises mainly executing previous contracts and generally taking a cautious attitude toward new orders, reflecting wait-and-see sentiment toward subsequent market trends.

Impact From Substitute Materials Intensified, High-End Segment Became the “Last Fortress”: It is worth noting that against the backdrop of persistently high copper prices, the trend of material substitution in downstream industries has been strengthening. Substitutes such as stainless steel, alloy materials, and plastics have squeezed copper semis across multiple application fields. This was especially evident in the low-end sanitary ware segment, where cost sensitivity is relatively high and the substitution trend has already become quite clear. Industry sources said that at present, “perhaps only the high-end segment still uses copper semis relatively firmly,” while the substitution process in low-end segments was accelerating.

Overall, the brass billet industry is currently operating in a pattern of “high costs, weak order intake, and strong divergence.” On the one hand, tight recycled raw materials supply and persistently high prices continued to squeeze enterprise profit margins. On the other hand, downstream demand remained uneven, with weak growth in traditional sectors, while the accelerated penetration of substitute materials further narrowed the application scenarios for copper semis. With no clear correction yet in copper prices, brass billet enterprises are expected to maintain cautious raw material procurement strategies, leaving limited room for a substantial increase in the industry's operating rate. The market is expected to remain in a volatile operating trend amid the tug-of-war between costs and demand.

![Downstream Bearish on Copper Prices, Intraday Purchase Willingness Flat [SMM Secondary Copper Daily Review]](https://imgqn.smm.cn/usercenter/KtfdC20251217171713.jpeg)