SMM News, March 30:

Import side, cumulative refined lead imports in January-February reached 33,412 mt, surging 732.08% YoY. Of this, February imports alone were 21,072 mt, up 70.77% MoM and 1,169.62% YoY, hitting a new high for the same period in recent years; raw material supply remained ample. The core drivers were: first, the domestic-overseas price ratio fluctuated at highs, the import profit window stayed wide open, and overseas suppliers' willingness to ship rebounded sharply; second, domestic smelting suspensions during the Chinese New Year and a sharp drop in secondary lead production allowed imported lead ingots to fill the supply gap; third, concentrated shipments from overseas sources such as India and South Korea further amplified import growth.

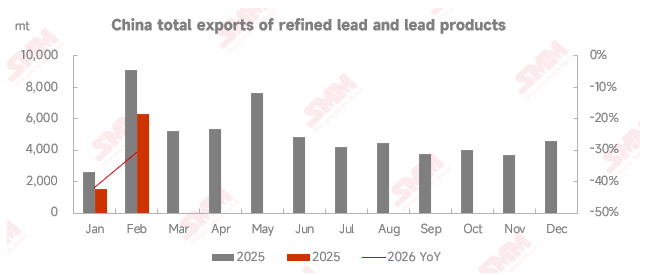

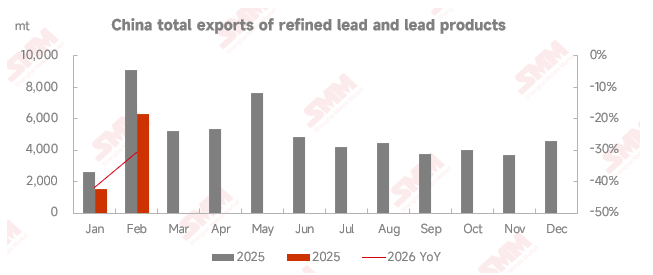

Export side, total exports of refined lead and lead materials in January-February were 7,798 mt, down 33.27% YoY. Of this, refined lead exports in February were 5,050 mt, up 981.88% MoM, mainly a short-term rebound driven by the low base during the Chinese New Year in January, but still down 40.31% YoY, indicating insufficient long-term export momentum.

In March, the import window remained open, and as the Chinese New Year holiday effect faded, overseas suppliers resumed shipments to China. In addition, orders concluded in February arrived at ports one after another in March. SMM expected refined lead and lead materials imports in March to remain considerable.

Entering April, more domestic smelters will resume operations, refined lead production will rebound rapidly, and the domestic supply gap will narrow. Meanwhile, fluctuations in LME lead prices will drive a narrowing in the price spread between domestic and overseas markets, compressing import profits and marginally weakening overseas suppliers' willingness to ship. Coupled with the high base effect in February-March, refined lead imports are expected to decline in April. On the export side, due to persistently high domestic lead smelting costs, refined lead exports will return to low levels, and the overall weak trend will be difficult to change.

![Macro Situation Changes Frequently; Fundamentals Remain Firm: Subsequent Lead Prices May Dip and Then Rebound [SMM Lead Market Weekly Forecast]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![Lead prices weaken, raw material costs stay firm, and smelter losses continue [SMM Secondary Refined Lead Weekly Review]](https://imgqn.smm.cn/usercenter/xVgcv20251217171721.jpg)

![Multiple Factors Drive Significant Decline in Primary Lead Enterprise Inventory [SMM Primary Lead Inventory Weekly Review]](https://imgqn.smm.cn/usercenter/bAjSC20251217171721.jpg)