Recent volatility in the Indonesian commodities sector has been driven by mixed signals regarding new fiscal policies. Market participants are currently evaluating the implications of two distinct regulatory mechanisms: a broader windfall tax on bulk commodities like coal, nickel, and a targeted export duty. The conflation of these two policies has generated significant market uncertainty, culminating in a sharp spike in global nickel prices this week.

To understand the current market anxiety, which culminated in a sharp spike in global nickel prices this week, it is essential to unpack the timeline of these policy discussions, differentiate the fiscal mechanisms at play, and assess the likelihood of their implementation.

Background: From Broad Windfall Deliberations to Targeted Export Tariffs

The narrative surrounding new commodity taxes in Indonesia did not emerge overnight; rather, it has evolved through distinct phases of policy signaling.

The current policy discourse has evolved in phases. Initial discussions, highlighted by statements from Coordinating Minister for Economic Affairs Airlangga Hartarto on Mar 13, 2026, focused on the potential implementation of a windfall tax. This broader fiscal measure was aimed at capturing excess margins from exporters of coal, palm oil, and base metals, such as nickel, gold, and copper during periods of elevated global prices, functioning primarily as a macroeconomic revenue-generation tool.

However, the conversation shifted dramatically on March 25, 2026. According to Bloomberg, news broke that Indonesia’s President had officially approved an export tax specifically targeting coal and nickel. This headline acted as an immediate catalyst, sending LME and SHFE nickel prices spiking.

The confusion currently gripping the market stems from the conflation of these two distinct policy trajectories: the older, revenue-focused windfall tax concept championed by economic ministers, and the newly approved, strategically focused nickel export tax aimed at forcing further downstream industrialization.

Analysis & Understanding: The Precedent of the "Windfall Tax"

To accurately gauge the impact of these rumors, it is critical to understand that the concept of a "windfall tax" is not entirely unprecedented in Indonesia's regulatory framework, particularly for bulk commodities.

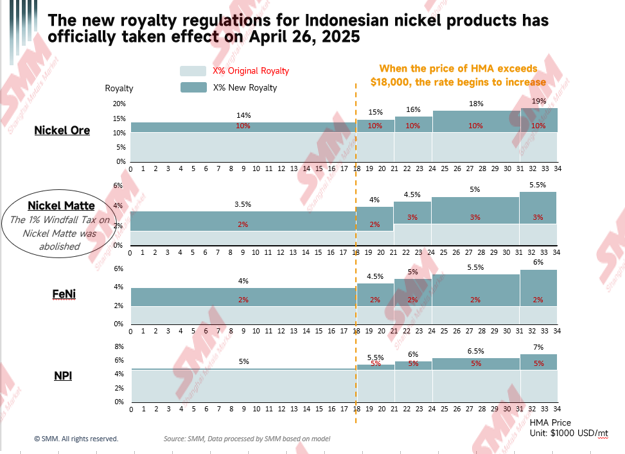

There has actually been a windfall tax structure in place previously, though often masked under the nomenclature of progressive royalties and non-tax state revenues (PNBP). For the coal sector, the government already utilizes a tiered royalty system pegged to the Harga Batubara Acuan (HBA) benchmark. As coal prices escalate into higher brackets, the royalty percentage automatically increases, effectively acting as a windfall capture mechanism.

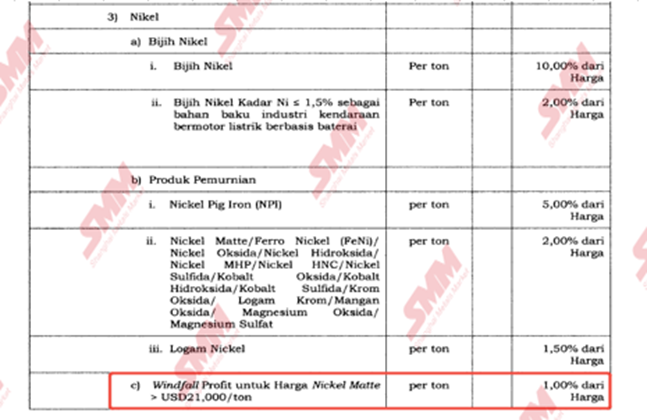

Similarly before, the nickel sector utilizes the Domestic Benchmark Price (HPM) and associated royalty structures to adjust to global price rallies. It is crucial to note that the government has previously experimented with specific windfall profit provisions for downstream products, though the regulatory stance has recently hardened. For instance, under Government Regulation (GR) No. 26/2022, a unique windfall profit incentive was applied to nickel matte: when prices exceeded $21,000 per ton, the royalty rate was actually reduced from the standard 2% to 1%.

(Old Version)

However, this accommodating policy was explicitly abolished under the recent GR No. 19/2025. The removal of this incentive underscores a definitive shift toward more aggressive state revenue capture. Consequently, the recent "windfall tax" rumors primarily concern further tightening these existing brackets or introducing a supplementary surcharge on operating margins above a specific baseline.

(New Version)

Conversely, the newly approved nickel export tax serves a different primary function. Therefore, it is completely different than the concept of windfall tax. Rather than merely earning from peak profits, an export duty on semi-processed nickel (like NPI, MHP, FeNi, and Nickel Matte) is a structural tool designed to penalize the export of lower-value products. It is the natural continuation of Indonesia’s downstreaming (hilirisasi) agenda, intended to force producers to build stainless steel and EV battery precursor plants domestically in Indonesia, rather than shipping intermediate goods to other countries.

While a windfall tax fluctuates with market prices, an export tax acts as a permanent structural cost added to the global supply chain.

Conclusion: Imminent Implementation Amidst Ongoing Deliberations

Despite definitive headlines regarding executive approval and the targeted April 1, 2026 implementation date, the exact implementation details are currently under review by the relevant ministries.

Currently, specific details, including exactly how the proposed 5%, 8%, and 11% tiers might translate from coal to specific nickel material classifications (e.g., NPI, MHP, and high-grade matte), must be urgently finalized ahead of the April deadline. The Ministry of Energy and Mineral Resources (ESDM), the Ministry of Finance, and the Coordinating Ministry for Maritime and Investment Affairs are working to balance state revenue optimization with the need to maintain the global cost-competitiveness of domestic smelters. This deliberative phase should not be interpreted as a policy reversal. According to SMM's understanding and industry checks, the implementation of these fiscal measures is highly probable. While the exact rollout of tariffs may be structured to mitigate immediate operational shocks to the domestic smelting sector, the fundamental policy direction indicates that the era of tariff-free exports for intermediate nickel products might decisively coming to an end.

![[SMM Stainless Steel Flash] Asian Stainless Steel Prices Hold Steady for Third Consecutive Week Amid Quiet Market](https://imgqn.smm.cn/usercenter/NHXhQ20251217171733.jpg)