In 2025, the sulphur market experienced wild swings under the dual impact of multiple supply-side contractions and the rapid release of new energy demand, with prices rising by more than 200% for the full year. Looking ahead to 2026, the tight supply-demand landscape is expected to persist.

Multiple Supply-Side Contractions

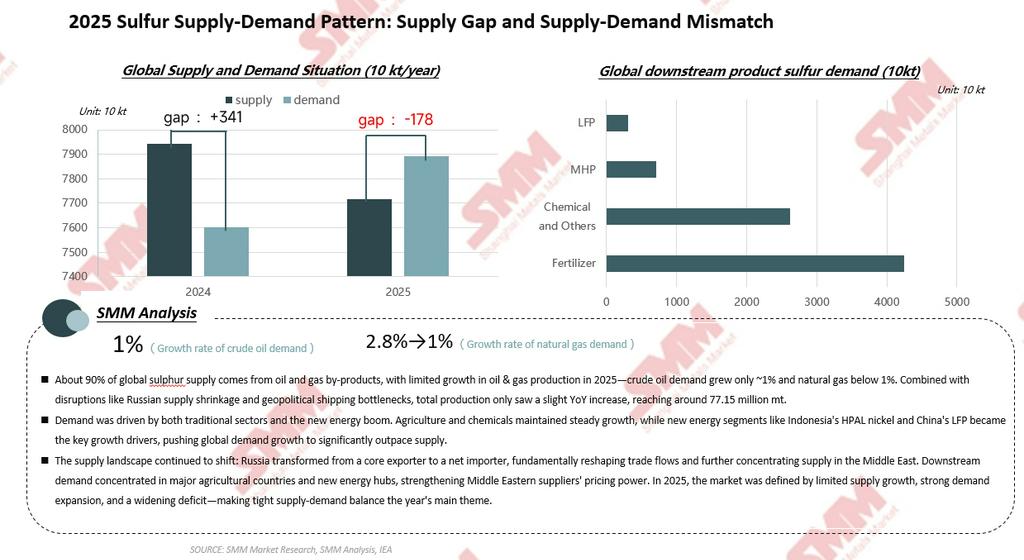

As elemental sulphur, over 90% of global sulphur supply came from crude oil and natural gas recovery, making it a by-product passively generated during petroleum refining and natural gas purification due to environmental protection requirements. In 2025, the global sulphur supply side was constrained by multiple factors.

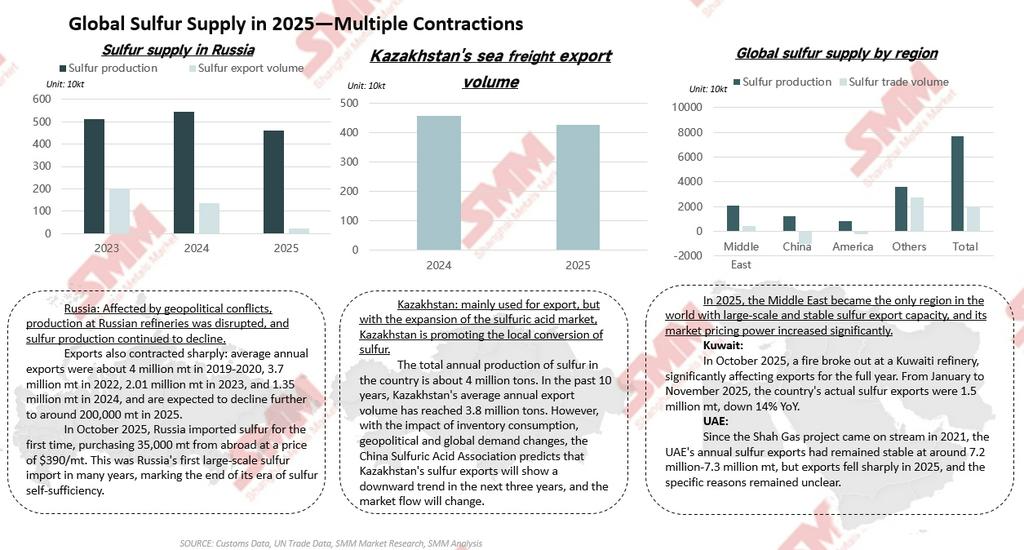

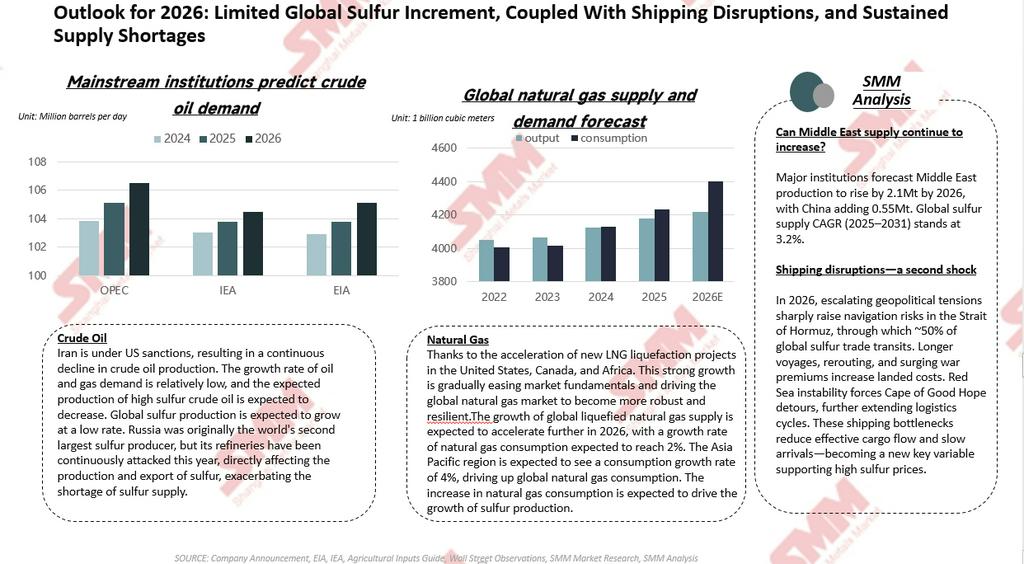

Affected by geopolitical conflicts, Russia's sulphur exports declined year by year. By October 2025, Russia began importing sulphur, shifting from a previous exporter to a net importer, and is expected to import about 1 million mt annually, further exacerbating the global sulphur supply-demand imbalance. In Kazakhstan, according to MCS and UN Comtrade data, its sulphur exports had already exceeded domestic production in 2024, accounting for about 25% of global sulphur trade volume. However, to promote local conversion, Kazakhstan's sulphur exports are expected to trend downward over the next three years. Against this backdrop, the Middle East became the only region globally with the capacity for large-scale and stable sulphur exports. However, structural adjustments also emerged within the Middle East. In 2025, total exports from Kuwait and the UAE declined, while Qatar's trade flows shifted, with resources originally flowing to the Americas diverted instead to Europe and the Asia-Pacific region.

According to SMM estimates, the above factors resulted in a global sulphur supply gap of 1.78 million mt in 2025.

New Energy Demand Became the Core Growth Driver

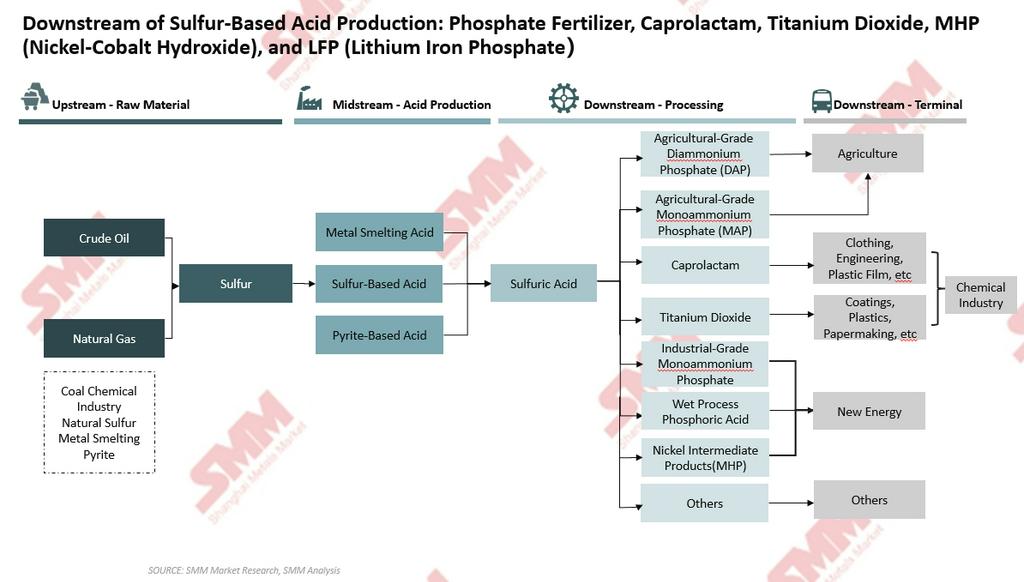

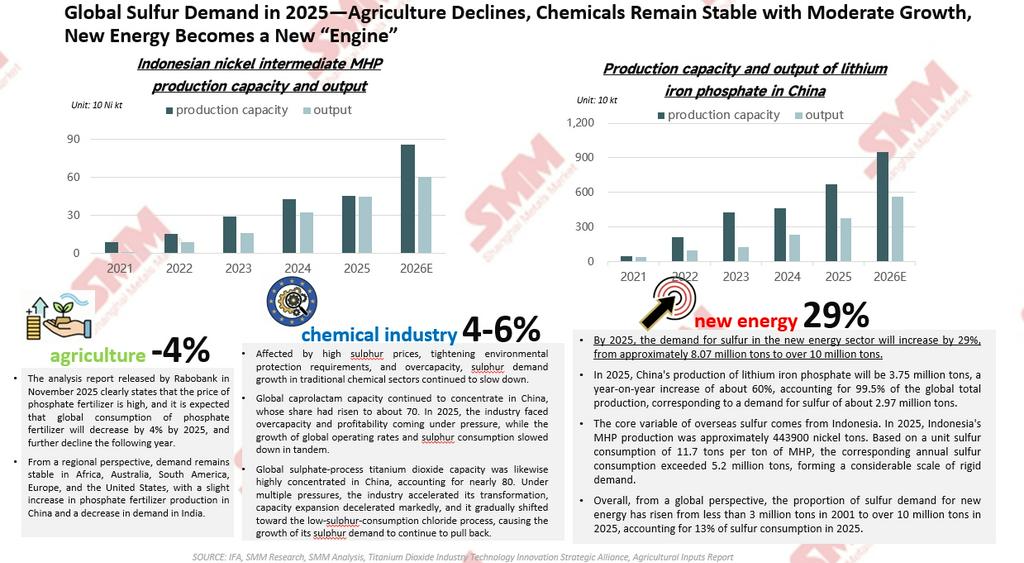

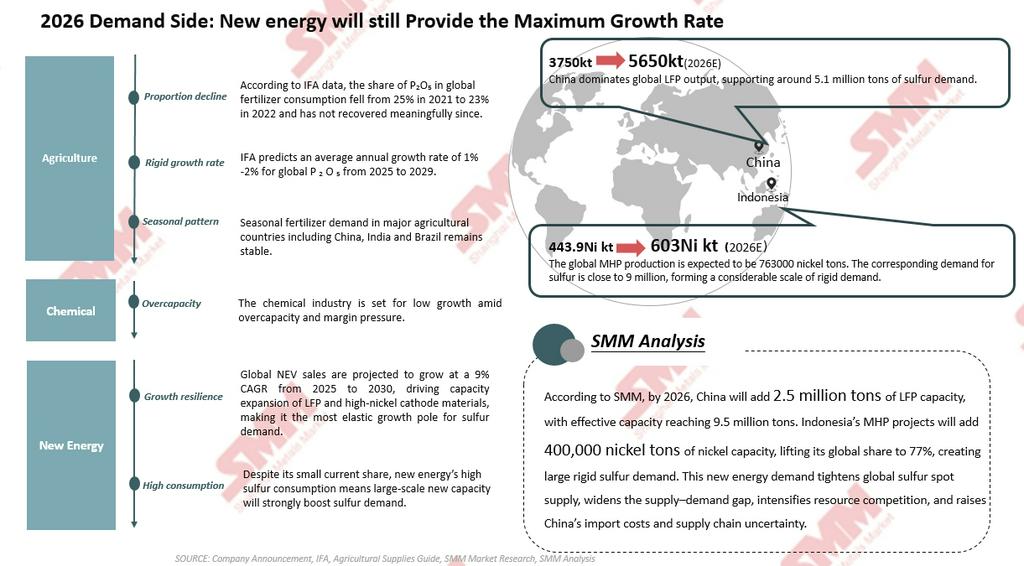

Demand structure, over 90% of sulphur was used to produce sulphuric acid, whose downstream sectors covered fertilizers, chemicals, and new energy. In 2025, the fertilizer industry still accounted for more than half of sulphur consumption, but production is expected to decline somewhat under the impact of high prices; in the chemical sector, global operating rates for caprolactam and titanium dioxide slowed down, while the titanium dioxide industry gradually shifted toward the chloride process, which consumes less sulphur.

The new energy sector became the core growth engine on the demand side. In 2025, sulphur demand from the global new energy sector was up 29% YoY, rising from about 8 million mt to more than 10 million mt. Among this, LFP production reached 3.77 million mt and MHP (mixed hydroxide precipitate) production stood at 443,900 mt Ni, with combined sulphur consumption reaching 10.43 million mt. The rapid release of new energy demand became the key variable affecting the sulphur supply-demand balance, showing the distinctive feature of “small share, big impact.”

International Sulphur Prices Rose by More Than 200% for the Full Year

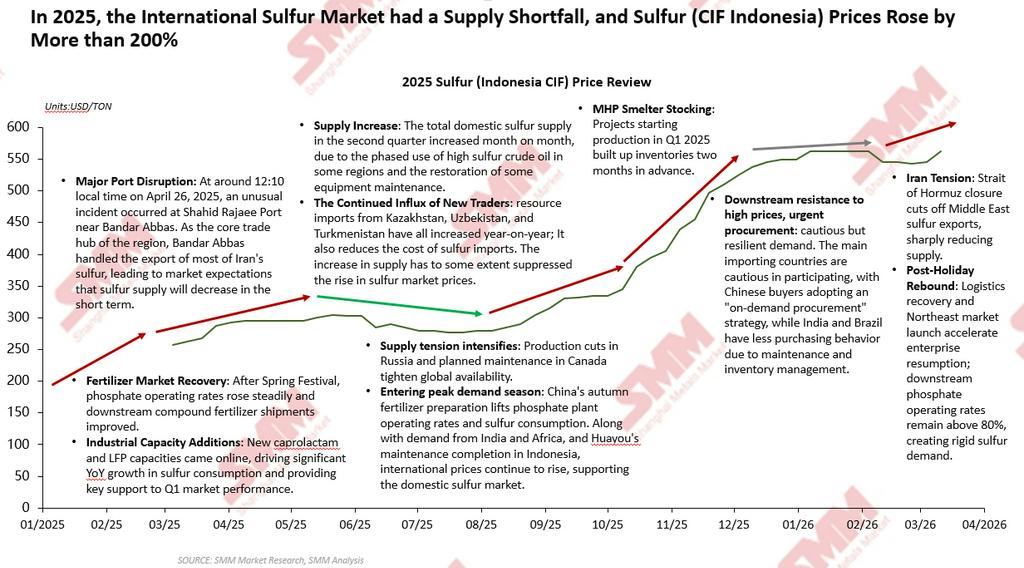

Using the Indonesia CIF sulphur price in the SMM database as a reference, sulphur prices rose from less than $200/mt at the beginning of 2025 to more than $560/mt by year-end, up more than 200%.

By phase, in Q1, rigid demand from the mainstream fertilizer market supported sulphur prices; in Q2, affected by expectations of tight supply, market transaction prices continued to rise; after June, high prices attracted traders to enter the market, market supply increased in the short term, tight supply and demand somewhat eased, and prices fell slightly; starting from August, as the peak season for new energy arrived, the procurement pace of MHP smelters accelerated, sulphur demand increased, and together with declining production in Russia and maintenance at Canadian producers, the tight supply-demand landscape once again drove prices higher. By January 2026, downstream resistance to high prices had emerged, procurement in the Chinese and Indonesian markets slowed down, and purchasing activity in India and Brazil decreased due to inventory management, pushing sulphur prices into a high-level standoff stage, with a downward trend appearing in February. Recently, affected by geopolitical conflicts, shipping through the Strait of Hormuz has been disrupted, directly threatening Middle Eastern sulphur export routes, and prices have once again shown an upward trend.

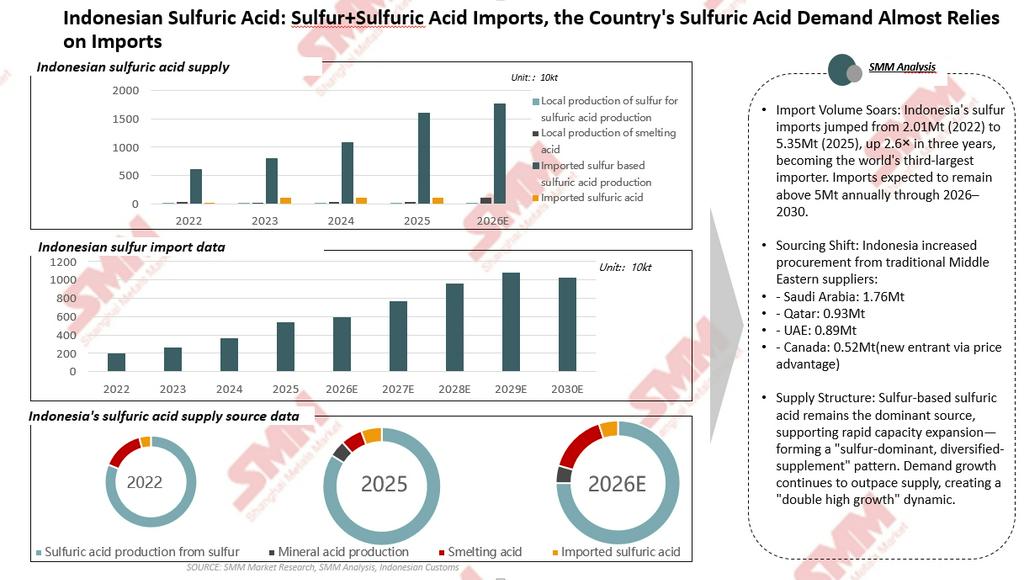

China and Indonesia: Market Characteristics of the Two Major Importing Countries

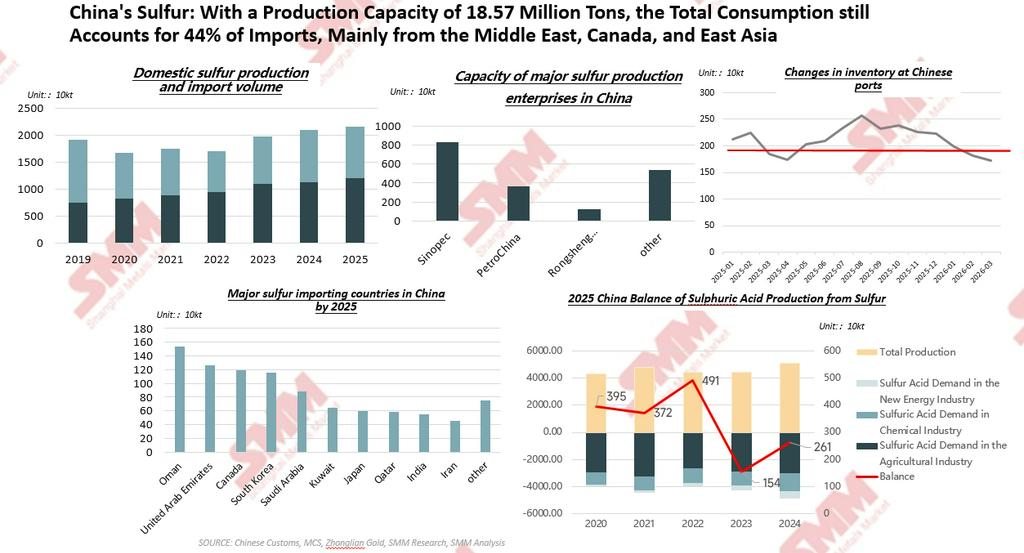

As the world’s net importer of sulphur, China’s sulphur production approached 12 million mt in 2025, but it still needed to import 9.6 million mt to meet downstream demand. Looking at historical price trends, China’s sulphur prices experienced three historical peaks: in 2008, affected by supply-side maintenance and rapid growth in the global fertilizer industry, the highest price reached 6,000 yuan/mt; in 2022, affected by the Russia-Ukraine conflict, shrinking supply triggered market panic, driving prices up to 4,000 yuan/mt; in 2025, due to supply contraction and an explosion in new energy demand, the highest price reached 4,250 yuan/mt.

Indonesia, by contrast, underwent a dramatic transformation in its demand structure. As a country whose sulphur demand heavily relies on imports, Indonesia’s sulphur imports rose to 5.35 million mt in 2025, and it also imported 1.088 million mt of sulphuric acid, of which about 75% of sulphur originated from the Middle East. In terms of downstream applications, over the past four years, the share of metal processing in Indonesia’s sulphuric acid demand increased from 51 to 84, with MHP accounting for the vast majority, while demand in the fertilizer and chemical sectors fell from 45 to 15. Indonesia’s sulphuric acid market was characterized by a relatively low base, rapid growth, and a continuously rising share of MHP.

2026 Outlook: Tight Supply-Demand Pattern to Continue

Looking ahead to 2026, incremental global sulfur supply is expected to remain limited. On the crude oil side, high-sulfur crude oil production is expected to grow slowly under the impact of geopolitical conflicts, and may even decline due to the Iran situation at the end of February; the risk of disrupted shipping affecting sulfur supply continues to persist. On the natural gas side, the acceleration of new LNG liquefaction projects in the US, Canada, and Africa may provide incremental supplementary sulfur supply.

Demand side, agriculture is expected to see slow growth in 2026, while the chemical industry will likely expand steadily, continuing to provide stable support for sulfur demand. Sulfur demand from the new energy sector is expected to maintain rapid growth, with total demand likely to exceed 14 million mt, up 34. Among this, China’s LFP production is expected to reach 5.65 million mt, corresponding to about 5.1 million mt of sulfur demand; global MHP production is expected to reach 763,000 mt Ni, bringing nearly 9 million mt of sulfur demand.

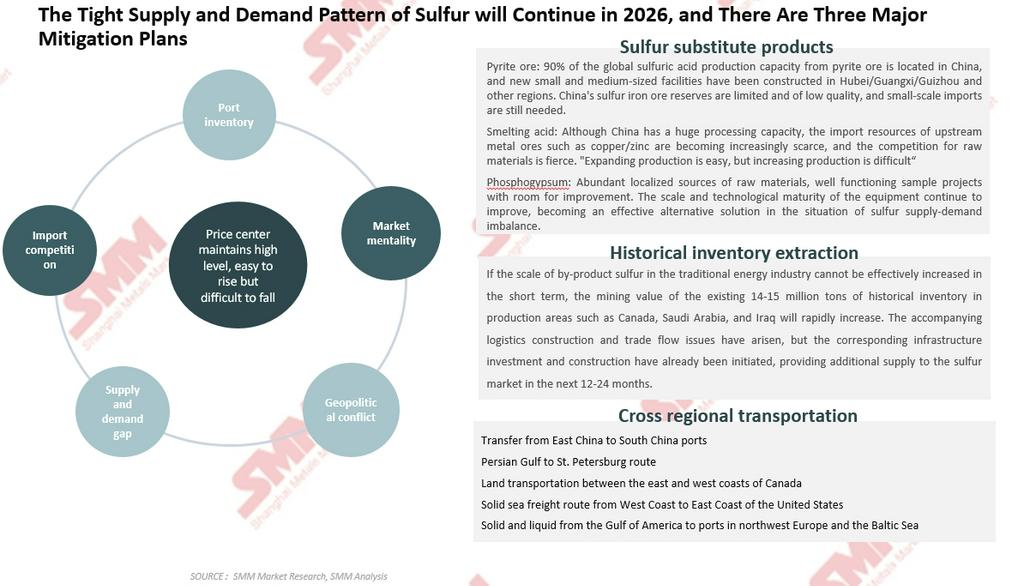

Overall, the tight sulfur supply and demand pattern in 2026 is unlikely to be fundamentally reversed. Potential easing solutions mainly include the use of substitute products such as pyrite, smelting acid, and phosphogypsum, the extraction of historical inventory, and interregional transfers, but their actual effects still require further market validation. Over the long cycle, the sulfur market is showing a pattern of “stable agriculture, expanding chemicals, and surging new energy,” with marginal demand growth represented by MHP and LFP having become a key variable affecting the supply-demand balance. Sulfur prices are expected to no longer be driven solely by seasonality in agricultural inputs and may continue to trend upward.

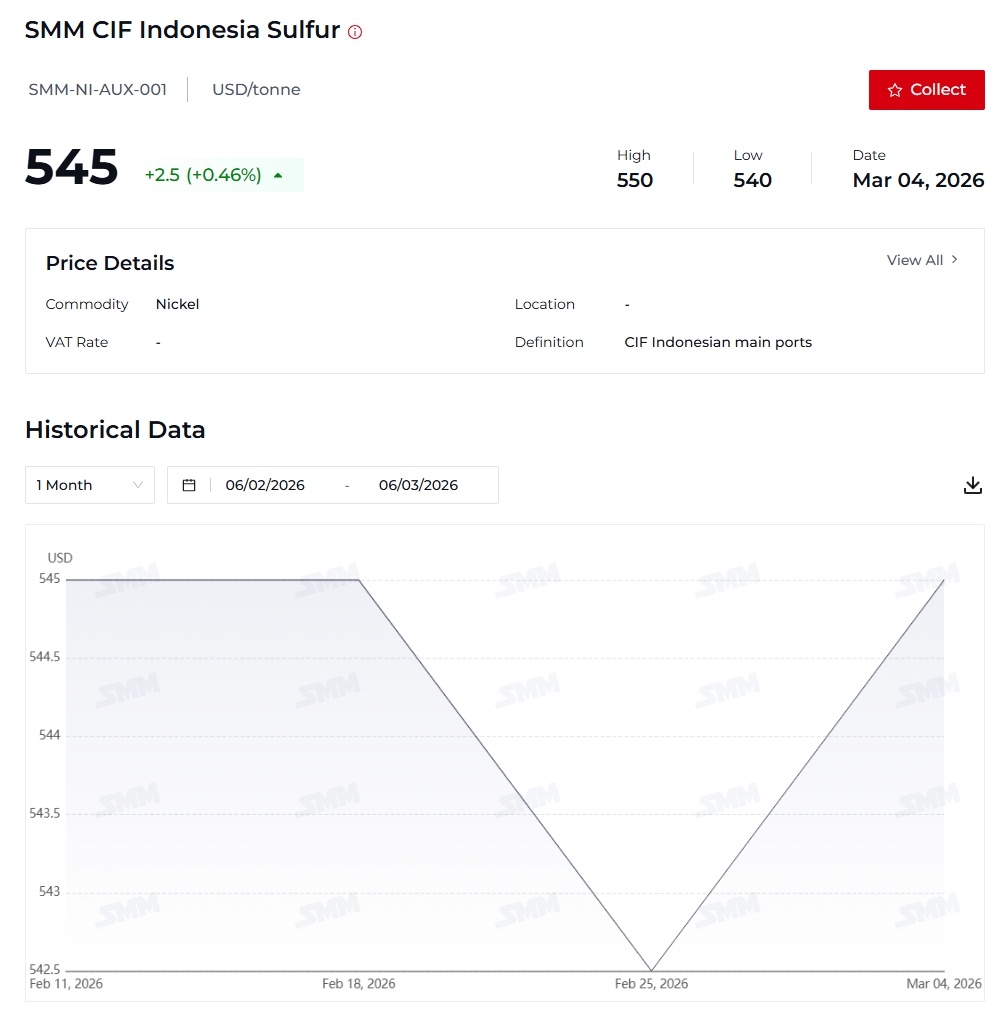

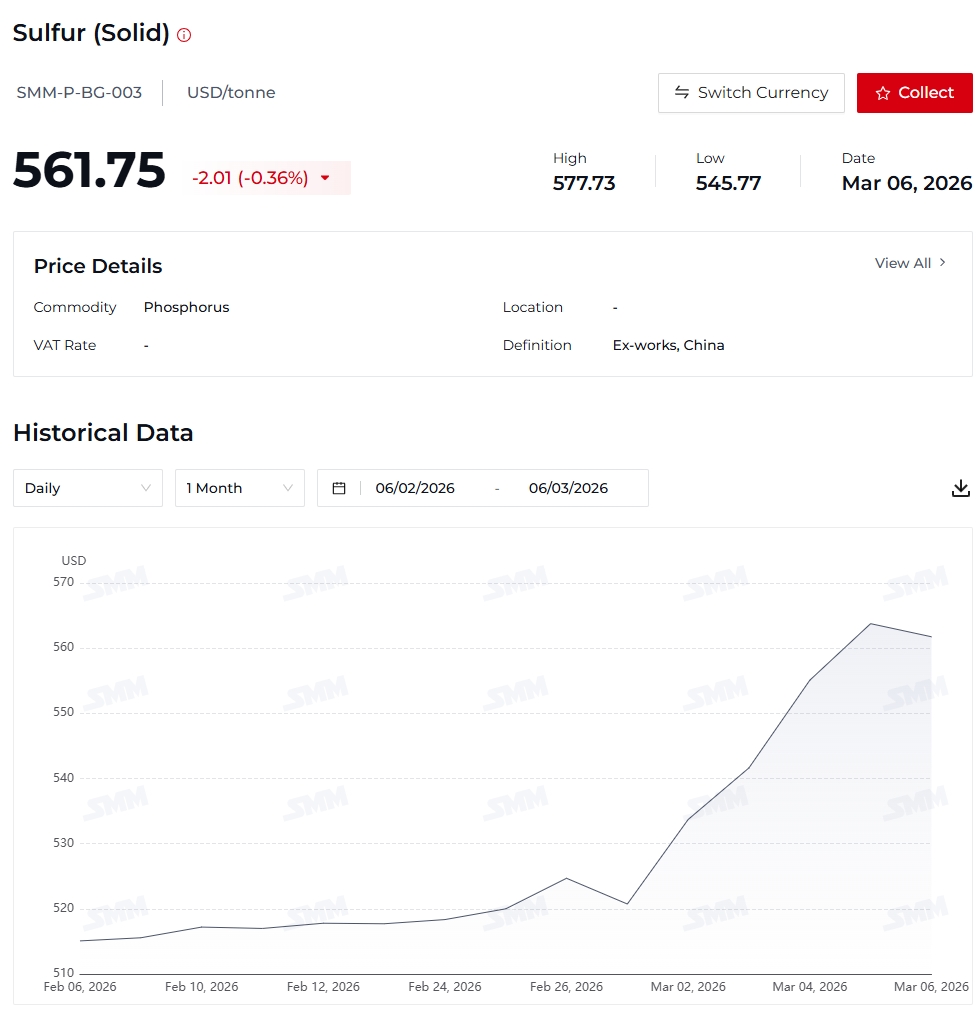

//SMM has launched SMM CIF Indonesia Sulfur and Sulfur (Solid) price assessments for market reference.

SMM CIF Indonesia Sulfur Definition:CIF Indonesian main ports; Quality: Sulfur 99.5% min, Particle; Price Origin: Indonesia.

Sulfur (Solid) price Definition: Ex-works, China; Quality: Sulfur(S) 99.00% min,conforming to GB/T 2449-2006; Price Origin: China.