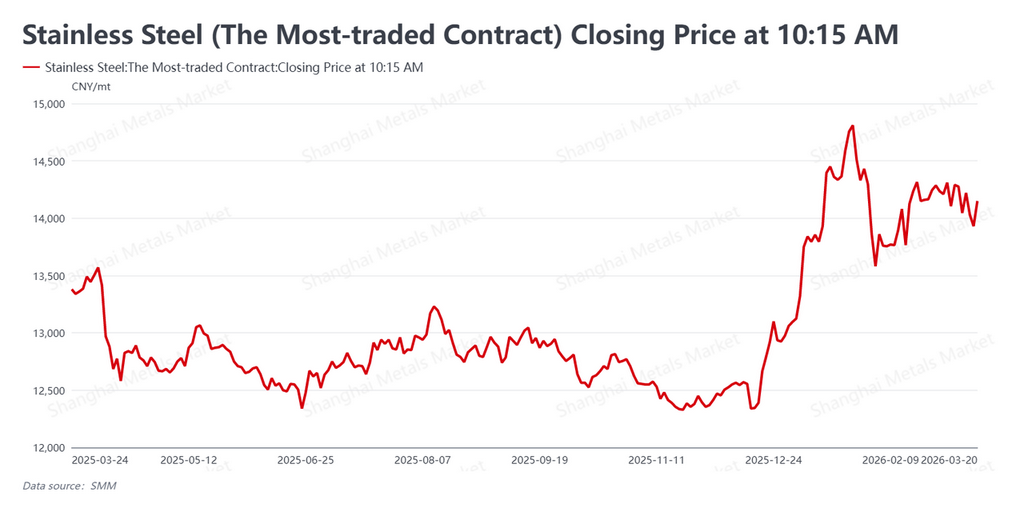

According to SMM data, during the second half of the traditional "Golden March" peak consumption season (March 16 - March 20, 2026), the most-traded stainless steel futures contract (SS2605) trended lower from its highs under the dual pressure of macroeconomic headwinds and tepid actual demand. By the close on March 20, the contract retreated to 14,150 yuan/mt (approx. $2,051/mt), down 125 yuan/mt (approx. $18/mt) from last Friday's close of 14,275 yuan/mt (approx. $2,069/mt). The market's core feature this week was the marginal weakening of previous bullish factors: international macro signals tilted hawkish, raw material upward momentum stalled, and the substantive recovery of end-user demand during the peak season remained lackluster, prompting a rational pullback in futures prices after hitting resistance.

Macro-Economy: Divergence Between Global Hawkishness and Chinese Resilience

On the macroeconomic front, a significant divergence emerged between global and Chinese economic data and policy directions. Internationally, the U.S. Federal Reserve ushered in a "Super Central Bank Week," deciding to hold its benchmark interest rate steady at 3.5%-3.75%. Influenced by developments in the Middle East and sticky inflation, the Fed's latest dot plot—despite maintaining expectations for one rate cut this year and next—revealed a distinctly hawkish tilt. Market bets on rate cuts for the entire year were slashed to less than 11 basis points. The dashed hopes for loose dollar liquidity weighed on the overall valuation of the base metals sector.

In China, the National Bureau of Statistics released January-February economic data showing a stable start to the year. Value-added industrial output grew by 6.3% year-on-year, and total retail sales of consumer goods increased by 2.8%, though real estate development investment still fell by 11.1% YoY. This structural divergence indicates a certain resilience in Chinese manufacturing, but the drag from the property sector continues to cap the upward elasticity of end-user consumption.

Fundamentals: Destocking Continues, But Spot Market Feels Lukewarm

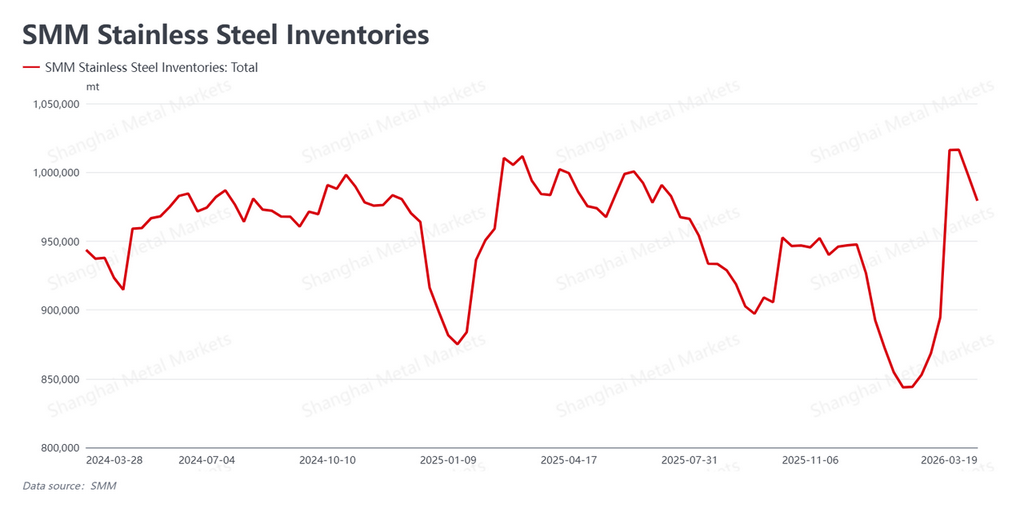

Fundamentally, social inventories maintained a destocking trend, but the spot market still lacked vigor. The latest SMM data shows social inventories falling further to 979,300 mt this week, a decrease of 18,800 mt from last week's 998,100 mt. The continuous decline in inventories sent a positive industry signal, stabilizing market sentiment to some extent.

However, the spot market still felt cold. Overall quotes remained stable, and end-user procurement strictly followed a just-in-time purchasing model, failing to exhibit the across-the-board boom expected during a peak season and leading to a strong wait-and-see sentiment. Currently, although the destocking trend is preserved, constrained by high absolute inventory levels and the anticipated supply increment from March steel mill resumptions, traders are maintaining a steady pace of shipments without resorting to aggressive panic selling.

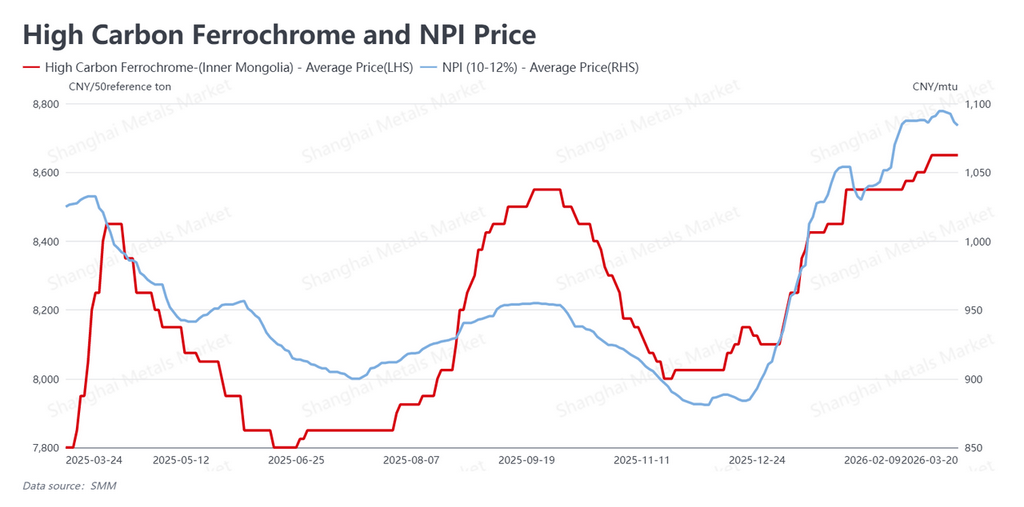

Costs: High-Level Loosening Pauses Cost-Driven Logic

The cost side also showed signs of loosening from its highs. As of March 20, high-grade nickel pig iron (NPI) quotes ended their previous unilateral rally, edging down to 1,084 yuan/mtu (approx. $157/mtu), while high-carbon ferrochrome prices held steady at 8,650 yuan/50 mt (approx. $1,254/50 mt).

With the pullback in futures prices and the sustained caution of steel mills regarding high-priced raw materials, NPI faced resistance in breaching the 1,100 yuan mark. The stabilization of raw material prices at high levels, coupled with slight price concessions, has temporarily alleviated the upward pressure on steel mills' cost centers, bringing the previously strong "cost-driven" logic to a temporary halt.

Outlook and Strategy

In conclusion, the stainless steel market this week entered a "deep water" zone where peak season expectations are repeatedly tested against reality. The Fed's hawkish stance pressured macro sentiment, while the "tepid" state of just-in-time end-user demand left fundamentals lacking intrinsic upward momentum. However, two consecutive weeks of steady destocking and stable spot quotes have effectively limited the depth of the market's correction.

Looking ahead to next week, the market will continue to seek a balance between "high inventories + supply increments" and "continuous destocking + just-in-time demand floor." The key focus will be whether the destocking slope reverses due to concentrated arrivals at steel mills. In the short term, the most-traded SS contract is expected to shift into a broad range-bound trend.

![[NPI Daily Review] As Nickel Prices Recovered, Low-Priced Sell-Offs Disappeared, and the Transaction Center of High-Grade NPI Stabilized](https://imgqn.smm.cn/usercenter/NHXhQ20251217171733.jpg)

![[SMM Nickel Sulphate Daily Review] March 21, Market Transactions Were Sluggish, and Nickel Salt Prices Remained Stable](https://imgqn.smm.cn/usercenter/Btmsv20251217171733.jpg)

![[SMM Nickel Midday Review] On March 23, nickel prices rose slightly as Trump demanded that Iran reopen the Strait of Hormuz within 48 hours](https://imgqn.smm.cn/usercenter/LNpBh20251217171732.jpeg)