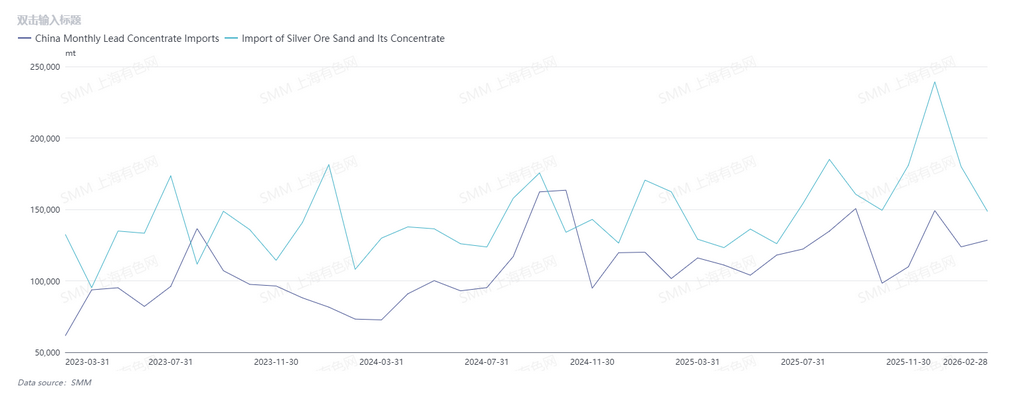

According to customs data, lead concentrate imports in February 2026 were 124,580 mt in physical content, up 3.8% MoM and up 26.4% YoY; cumulative imports in January-February reached 252,241 mt in physical content, up 14% YoY on a cumulative basis. Over the same period, silver concentrate imports were about 148,600 mt in physical content, down 17% MoM and down 8% YoY; cumulative imports in January-February were 328,600 mt in physical content, down 1.27% YoY on a cumulative basis.

By country, the main sources of lead concentrate imports in February were Peru, Russia, and Turkey; in January, they were Russia, Australia, and Peru.

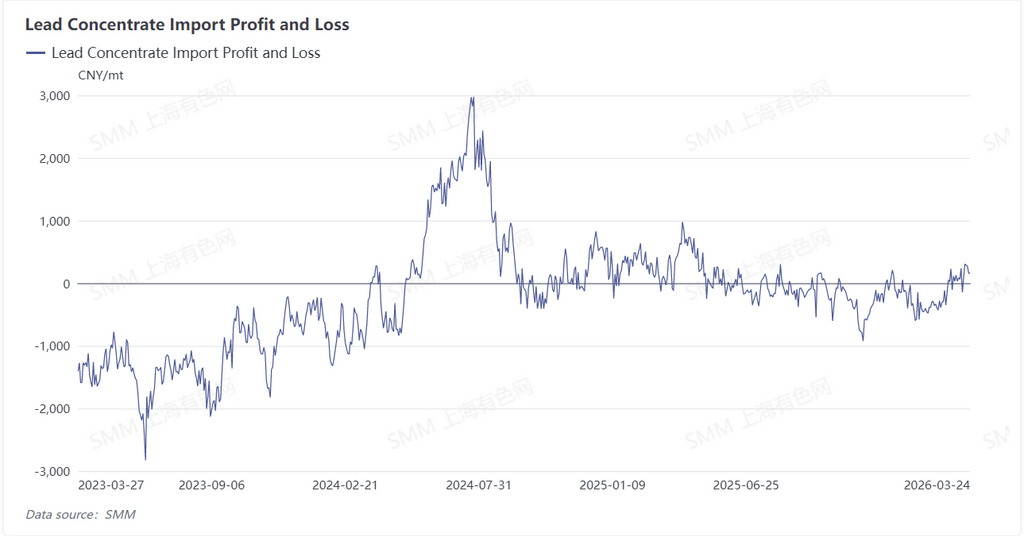

In terms of import profit margin and procurement strategy, the import window for lead concentrates had not yet opened at the beginning of 2026, and imports were still at a slight loss. However, amid concerns over raw material supply in H1 and inventory shortages caused by declining lead grade in imported ore, smelters generally advanced winter stockpiling, driving a sharp YoY increase in lead concentrate imports. After wild swings in silver prices in Q1, the market entered the doldrums, and with declining by-product earnings, smelters showed markedly weaker willingness to secure raw material at the cost of lower TCs.

Lead concentrate supply in March eased slightly compared to the same period last year, while smelters' willingness to operate declined, making extremely low-priced deals hard to see. It is understood that prices for lead concentrates arriving in the forward market remained broadly stable, while TCs for some low- and medium-silver polymetallic ores were raised slightly; after negotiations, some smelters were able to raise TCs of imported lead concentrates to -$120 to -$130/dmt. In late March, primary lead smelters in China gradually raised output, and lead concentrate supply was hard to call ample. Although imported ore TCs had already shown signs of a slight increase in April, TCs in China are expected to remain stable, with smelters actively negotiating while watching cautiously. If precious metal prices continue to decline, TCs that were previously lowered due to smelting demand may rebound.