14. March 2026

After a strong start, the price of gold slipped twice to around $5,060 during this trading week. Now, it appears that gold prices might manage to stay just above $5,100 heading into the weekend, continuing the persistent sideways movement of the past five weeks.

A similar picture is emerging in the silver market. However, silver continues to lag behind the development of the gold price and even recorded a temporary decline of over 9% during the week. Events in the precious metals markets are, however, overshadowed by the further escalating Iran war, the sharply rising oil price, and the looming energy and global economic crisis.

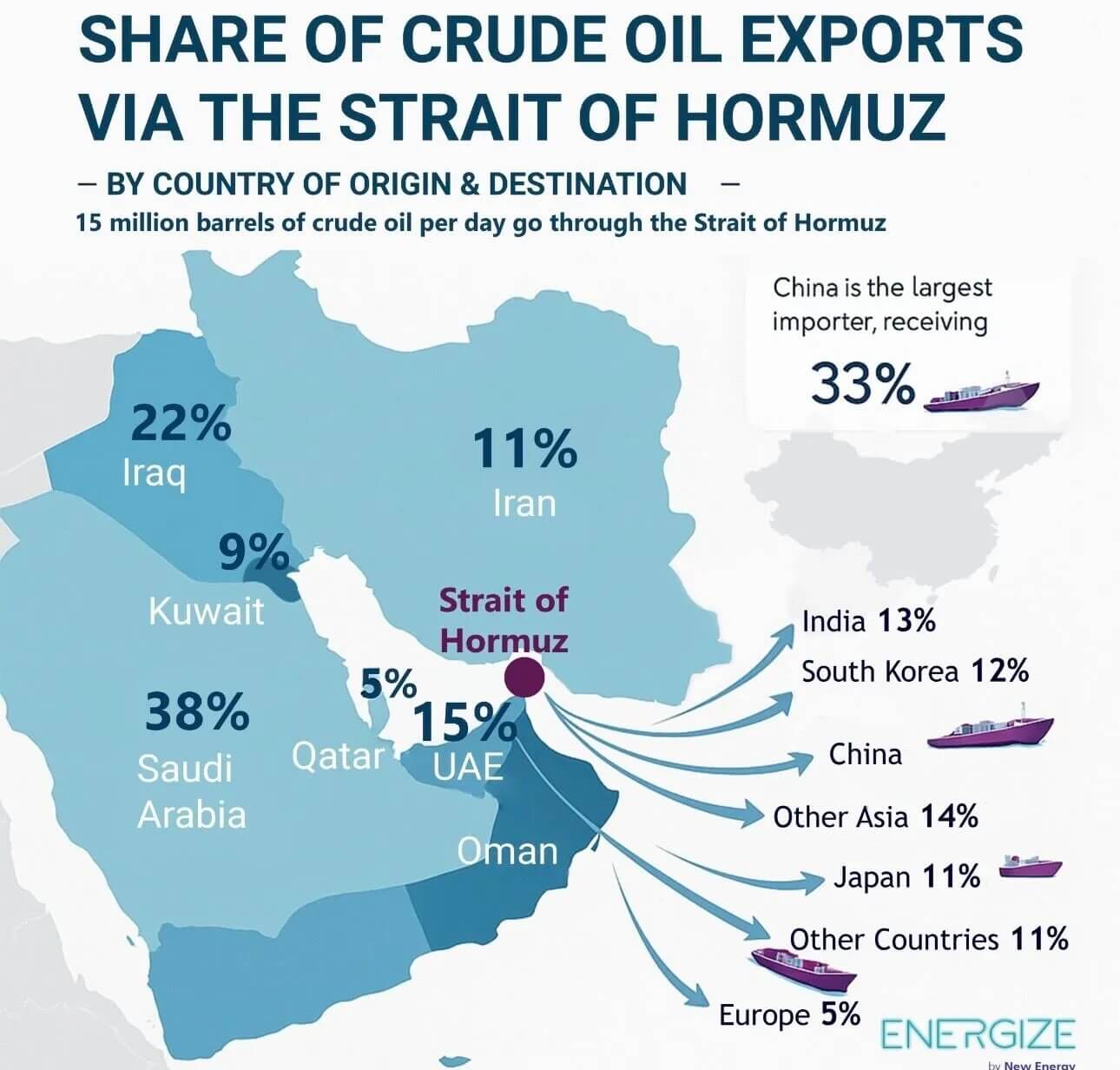

Share of crude oil exports via the Strait of Hormuz, as of March 11, 2026. © Giacomo Prandelli

Share of crude oil exports via the Strait of Hormuz, as of March 11, 2026. © Giacomo Prandelli

The closure of the Strait of Hormuz has already triggered a global cascade and exposed the fragile interdependencies of the modern economy. As a bottleneck for 20% of global oil and LNG trade, a zero-flow scenario would cause a deficit of 17.5 million barrels per day, which would be only marginally mitigated by limited pipeline diversions such as Saudi Arabia’s Petroline. This already drove oil prices to $120 last Monday in an initial panic attack. Our oil price target mentioned three weeks ago was thus reached in no time!

Although US President Trump initially managed to dampen fears of persistent supply bottlenecks caused by the blockade of the Strait of Hormuz and calm the markets, he did so with questionable promises and the easing of US oil sanctions against Russia. However, the continuation of the fighting and the strength of the Iranian counterattacks made it increasingly clear during the week that this conflict will not be over in a few days, but will continue to escalate. Shortly before the weekend, the oil price is trading at around $100 again, reflecting the ongoing geopolitical uncertainty.

The markets remain volatile and nervous. Oil prices of over $100 per barrel, amplified by skyrocketing freight rates and insurance surcharges, mark the transition from efficiency to scarcity. This creates strong inflationary pressure waves for the oil, energy, and financial markets. In the medium to long term, these should lead to an appreciation of gold and silver as a hedge against currency devaluation and systemic crises, while stocks in energy-dependent or energy-intensive sectors will collapse. Rising interest rates and a strong US dollar, in turn, have a deflationary effect on the overall economy.

Cascade effects on global supply chains

In this early phase of disruption, the failure of maritime logistics is already escalating into bottlenecks in the chemical and mining industries. The loss of sour crude oil leads to a sulfur deficit, which paralyzes sulfuric acid production and thus blocks copper and cobalt extraction in Africa and Chile. This exacerbates existing supply bottlenecks for transformers and switchgear and hits grid infrastructure hard, while refineries struggle to find alternatives.

In the next phase, the impact is likely to spread to the semiconductor industry and data centers. Taiwan’s dependence on LNG is already leading to initial power rationing and could paralyze TSMC factories and lead to wafer failures. Credit spreads are exploding in the capital markets, while foreign exchange reserves in emerging markets are coming under pressure. The announced government interventions, such as the release of strategic oil reserves, will likely have only a minor effect.

In the medium term, social unrest and geopolitical upheavals are likely. Trade routes are expected to become increasingly militarized, while the rise of the “Petroyuan” is already foreseeable. At the same time, fertilizer shortages, rising food prices, and failed industrial substitutions could worsen the situation. As a result, many countries are likely to rely on autarky, tariffs, and economic blocs where resource security is more important than efficiency. Due to the tight supply situation, oil prices should remain permanently high.

Gold and silver more important than ever

Overall, the closure of the Strait of Hormuz could change the global order from integrated trade to “armed scarcity.” For investors, gold and silver are therefore becoming even more important as a hedge.

In the short to medium term, precious metals are nevertheless in a correction. In a panic phase and a liquidity crisis on the financial markets, this could temporarily lead to significantly lower gold and silver prices.

Since the new all-time high of $5,594 on January 29, the gold price has been in a correction or consolidation. The initially extremely volatile price action has generally calmed down further over the last ten days. Nevertheless, depending on the news situation, the gold price can still rise or fall by $100 to $200 from a standing start and within a few hours.

The all-time high of $5,594 is offset by a correction low of $4,402. In addition, there is a series of higher lows and, at $5,419, a lower high. This means the gold price is once again moving into a triangle consolidation. The daily stochastics are heading towards the oversold zone, while the rapidly rising 50-day moving average ($4,947) is approaching the current price action as an important support level.

Bottom line, the expected dance around the round $5,000 mark continues, which still attests to a certain strength in the gold price. During the week, however, the precious metal appeared increasingly sluggish. If the bulls fail to defend the support at around $5,055 again, a rapid setback towards $4,910 looms. Given the tense market situation, we consider a defensive stance appropriate – we are currently consistently positioned for “risk-off.”

Conclusion: Gold – Consolidation continues despite the crisis

The closure of the Strait of Hormuz due to the escalated Iran war triggered a global cascade that drove the oil price up to $120 and terrified the financial markets. The sharp recovery in the stock markets in the meantime and the deep setback in the oil market are only understandable to us from a short-term sentiment perspective and the put/call ratio.

Too many market participants had hedged too much too quickly or bet on a rising oil price. The tentative signals of de-escalation from Iran and Trump’s reassurances then led to short covering and a reversal in the oil market. However, we fear that the West continues to deny the depth and bitter consequences of a Middle East war. We expect the oil price to be back above $100 soon and even rise to $150 in the coming weeks.

Not surprisingly, the stock markets, along with precious metals, are showing some weakness again at the end of the trading week. Gold appears increasingly sluggish, while the strong oil price once again dominates the markets! Overall, the gold price is still consolidating the brilliant rise of the last few months and the last two years. If bottlenecks in the chemical and semiconductor industries increase, fertilizer and thus food crises loom. In such an environment, we see precious metal prices moving sideways or slightly lower. Industrial metals and agricultural products, on the other hand, are likely to see significant price increases.

If the gold price can defend the support around $5,055, the bulls will remain in control overall. Below this mark, however, there is a risk of a rapid slide towards $4,910 and lower. There is also still an open price gap just below $4,350!

Overall, we remain on a “risk-off” course and are awaiting further developments with a high liquidity position.

As of: March 13, 2026

Written by:

Florian Grummes

Technical Analyst, Precious Metals Expert

Source: https://goldinvest.de/en/gold-consolidation-continues-despite-the-crisis/

![Platinum Prices Fell Sharply, and Spot Trading Recovered [SMM Daily Review]](https://imgqn.smm.cn/usercenter/gpWpd20251217171734.jpeg)

![Silver Prices Remained in the Doldrums, Spot Market Demand Weakened and Premiums Were Lowered [SMM Daily Review]](https://imgqn.smm.cn/usercenter/qopTu20251217171736.jpg)