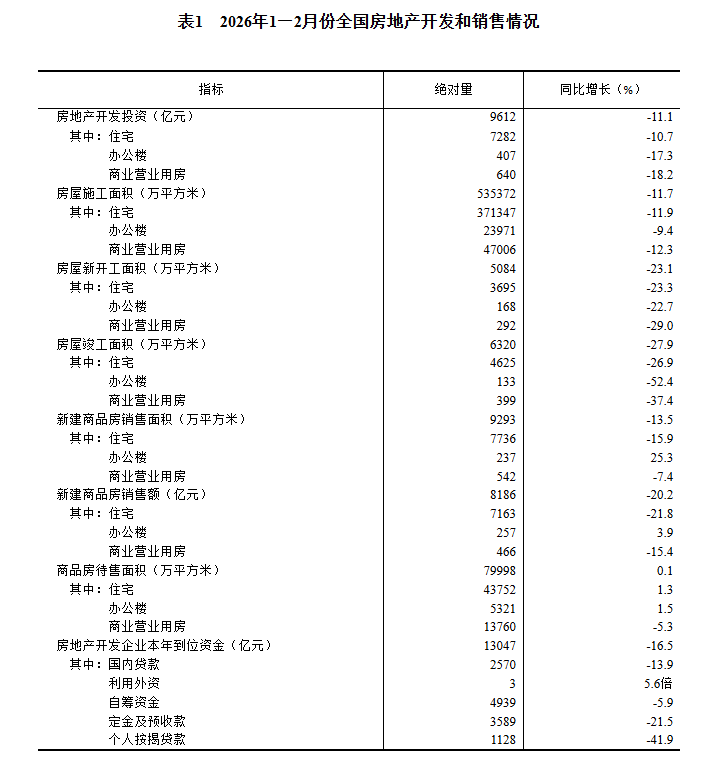

Data from the National Bureau of Statistics (NBS) showed that in January-February, China’s real estate development investment totaled 961.2 billion yuan, down 11.1% YoY, with the decline narrowing by 6.1 percentage points from the full-year level of the previous year; of which, residential investment was 728.2 billion yuan, down 10.7%, with the decline narrowing by 5.6 percentage points. In January-February, the floor space of buildings under construction by real estate development enterprises nationwide was 5.3537 billion m², down 11.7% YoY. Of this total, residential floor space under construction was 3.7135 billion m², down 11.9%. The floor space of buildings newly started was 50.84 million m², down 23.1%. Of this total, residential floor space newly started was 36.95 million m², down 23.3%. The floor space of buildings completed was 63.2 million m², down 27.9%. Of this total, residential floor space completed was 46.25 million m², down 26.9%.

I. Completion of Real Estate Development Investment

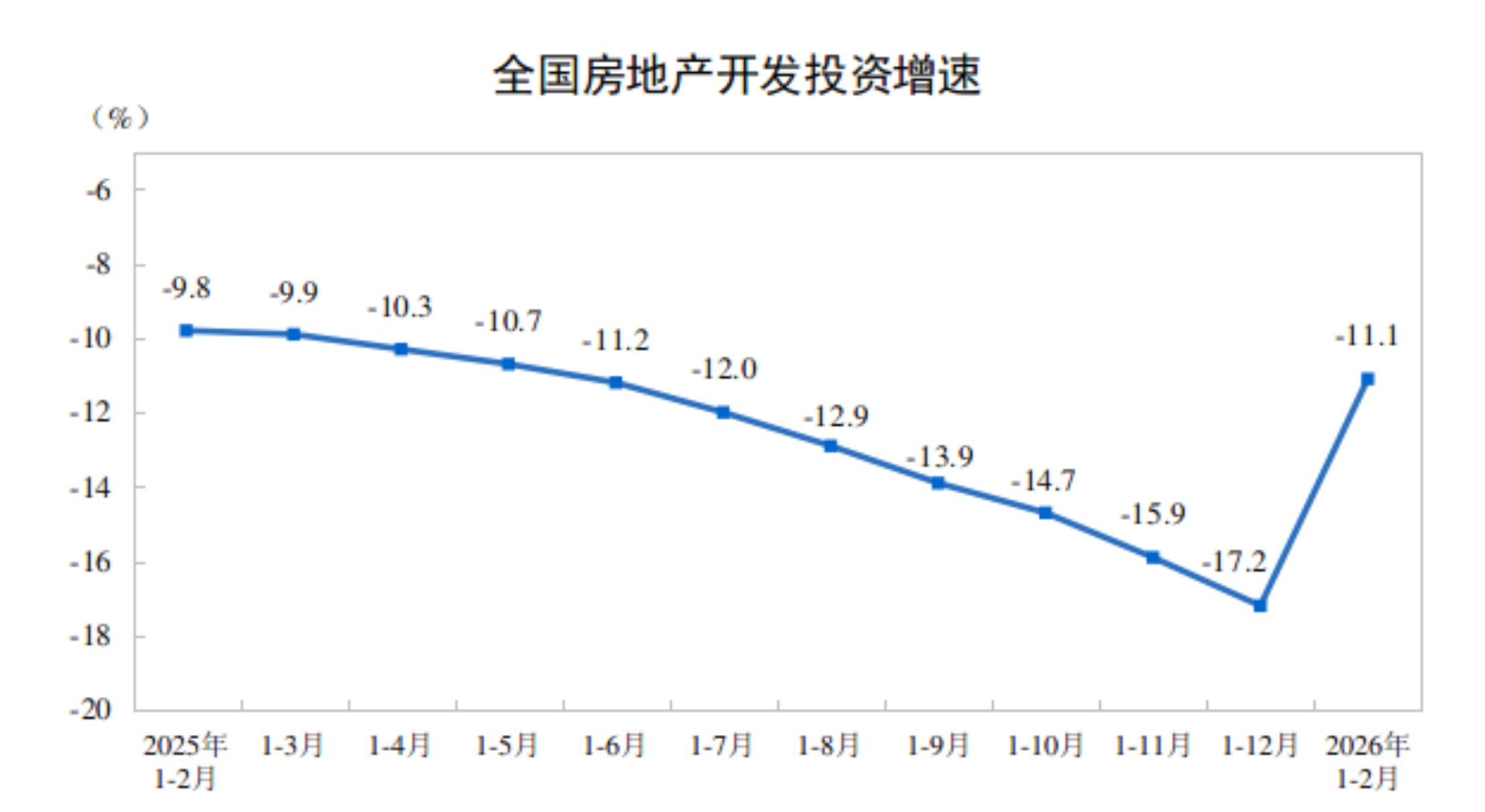

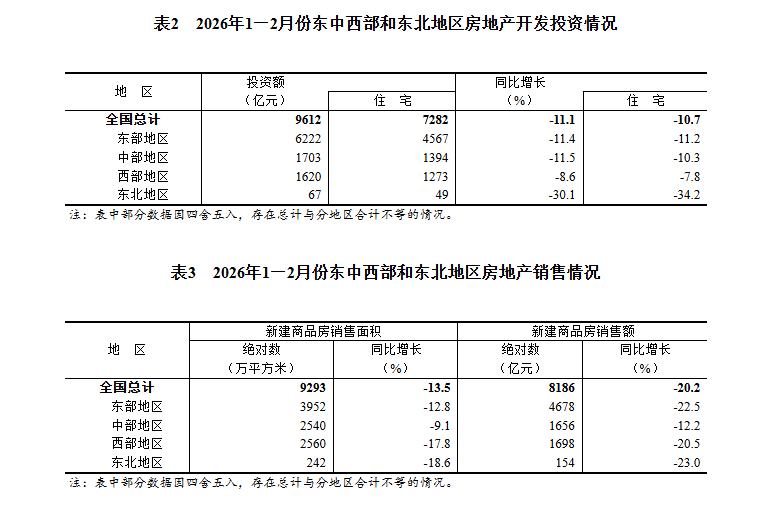

In January-February, China’s real estate development investment totaled 961.2 billion yuan, down 11.1% YoY (calculated on a comparable basis; see Note 5 for details), with the decline narrowing by 6.1 percentage points from the full-year level of the previous year; of which, residential investment was 728.2 billion yuan, down 10.7%, with the decline narrowing by 5.6 percentage points.

In January-February, the floor space of buildings under construction by real estate development enterprises was 5.3537 billion m², down 11.7% YoY. Of this total, residential floor space under construction was 3.7135 billion m², down 11.9%. The floor space of buildings newly started was 50.84 million m², down 23.1%. Of this total, residential floor space newly started was 36.95 million m², down 23.3%. The floor space of buildings completed was 63.2 million m², down 27.9%. Of this total, residential floor space completed was 46.25 million m², down 26.9%.

II. Sales of Newly Built Commercial Buildings and Pending Sale Status

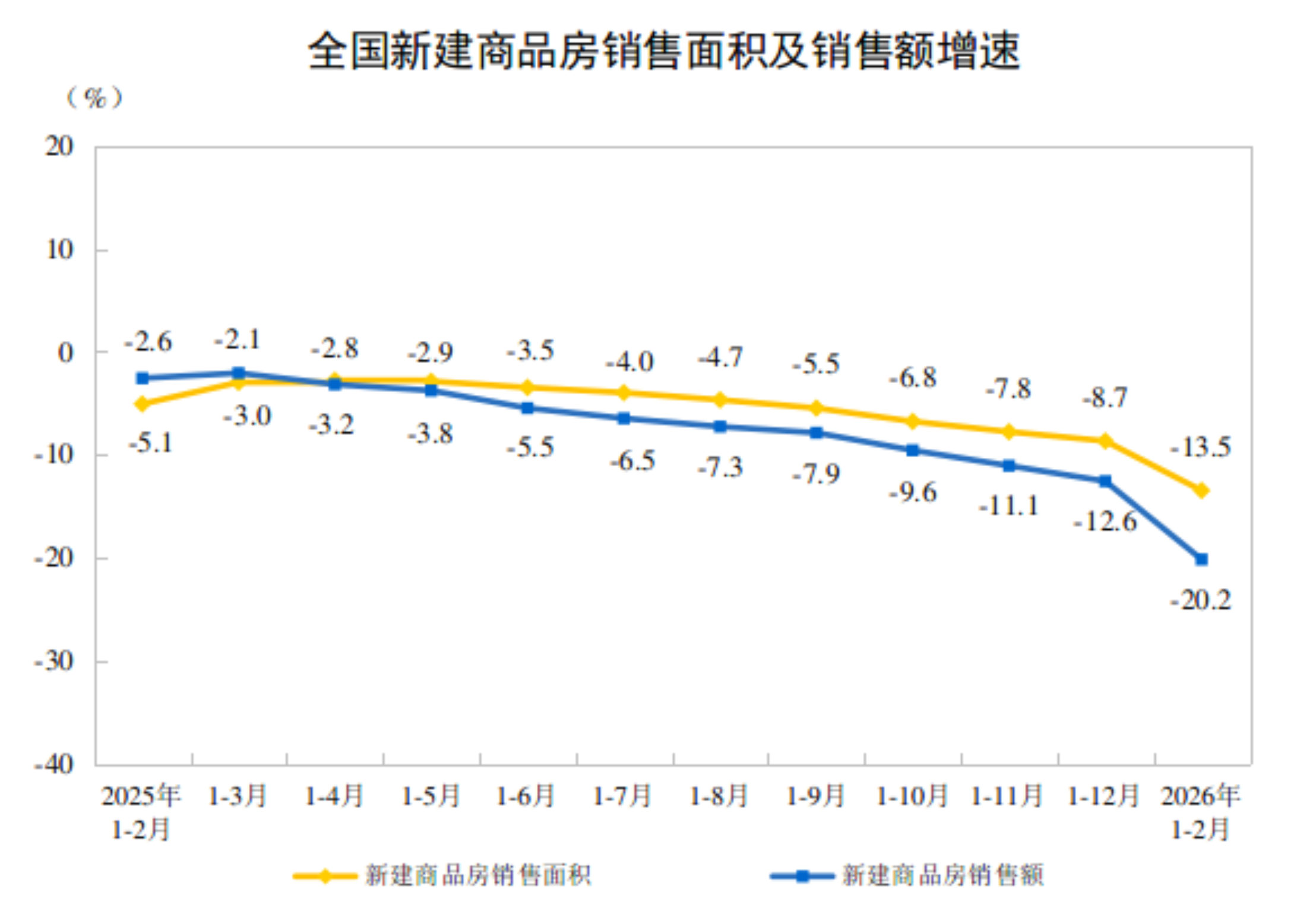

In January-February, the floor space of newly built commercial buildings sold was 92.93 million m², down 13.5% YoY, with the decline widening by 4.8 percentage points from the full-year level of the previous year; of which, residential sales floor space fell 15.9%. Sales of newly built commercial buildings amounted to 818.6 billion yuan, down 20.2%, with the decline widening by 7.6 percentage points; of which, residential sales value fell 21.8%.

At month-end February, the floor space of commercial buildings pending sale was 799.98 million m², up 0.1% YoY, with the growth rate pulling back by 1.5 percentage points from year-end 2025. Of this total, the floor space pending sale for less than three years was 606.16 million m², down 1.6%.

III. Funding Sources of Real Estate Development Enterprises

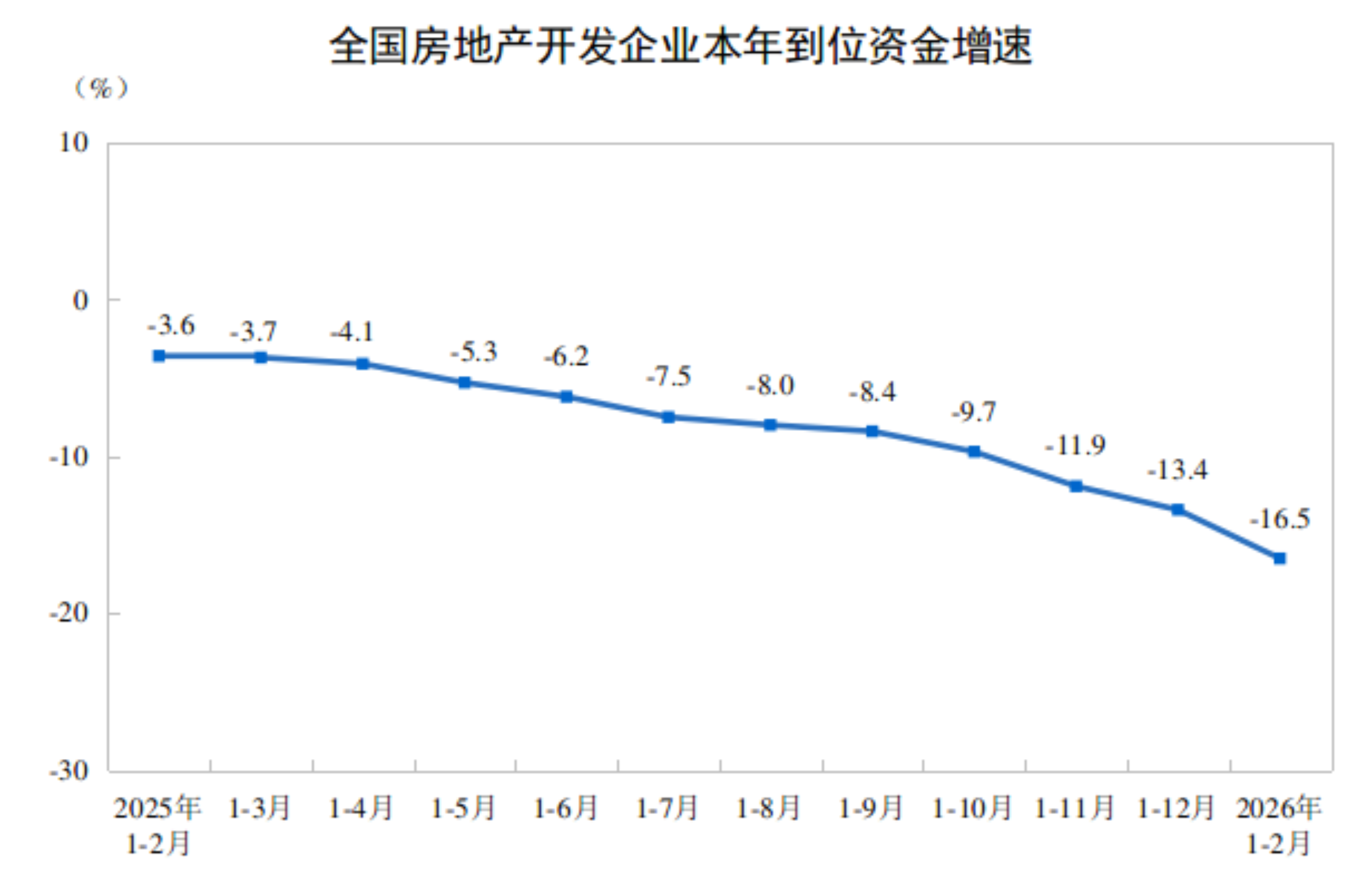

In January-February, funds in place for real estate development enterprises totaled 1,304.7 billion yuan, down 16.5% YoY. Of this total, China domestic loans stood at 257 billion yuan, down 13.9%; self-raised funds were 493.9 billion yuan, down 5.9%; deposits and advance receipts were 358.9 billion yuan, down 21.5%; and individual mortgage loans were 112.8 billion yuan, down 41.9%.

![Declining Aluminum Prices Boost Market Procurement Sentiment, Premiums Stabilize [SMM Spot Aluminum Midday Commentary]](https://imgqn.smm.cn/usercenter/ifCaw20251217171652.jpg)

![Import Window Opened Intraday, Active Morning Inquiries Pushed Up Offers [SMM Yangshan Spot Copper]](https://imgqn.smm.cn/usercenter/qcyEh20251217171709.jpg)

![Copper Prices Fell on the Last Trading Day, and Trading in the Shanghai Spot Copper Market Was Weak [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)