SMM News, March 14:

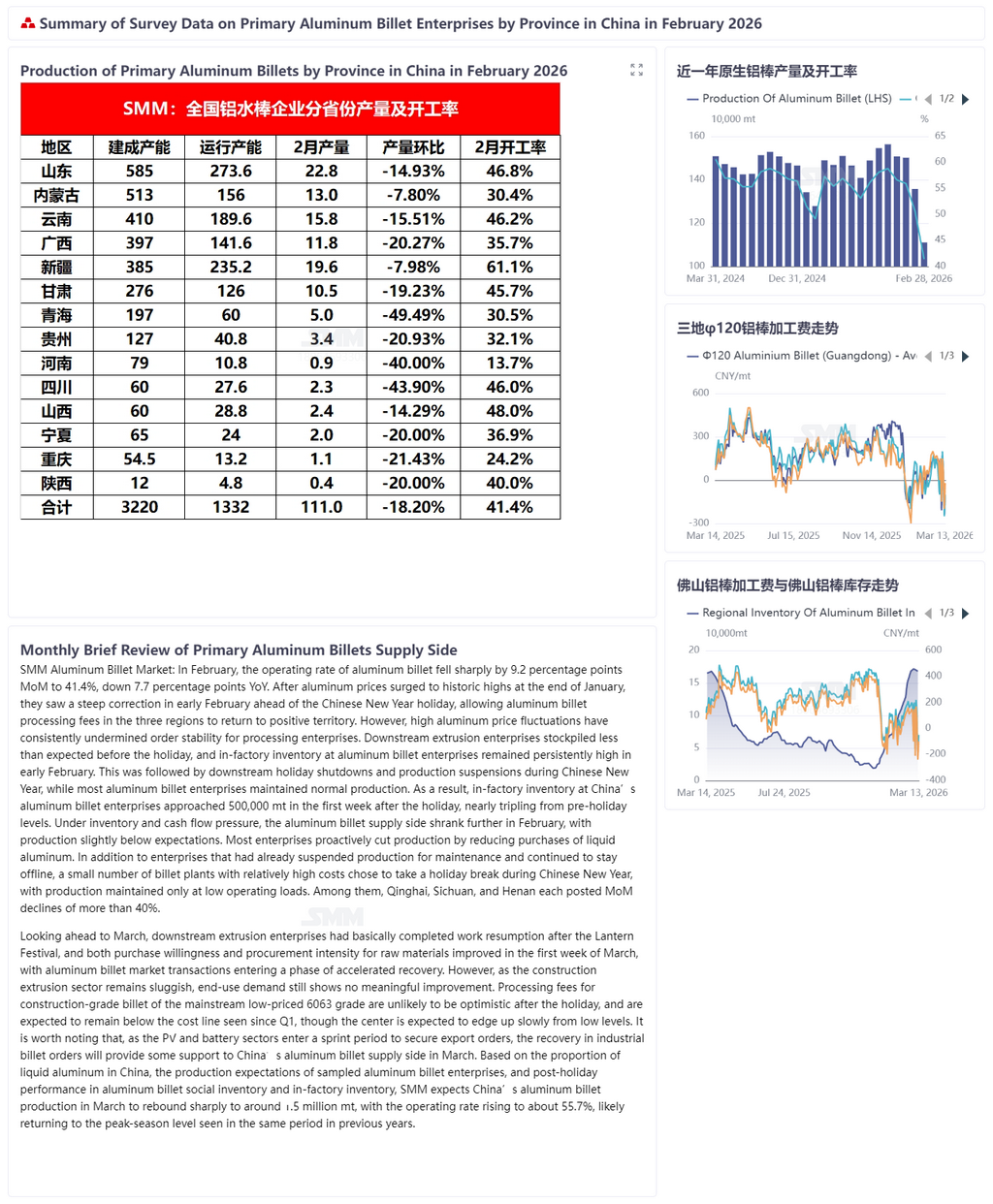

According to SMM data, the operating rate of aluminum billets fell sharply by 9.2 percentage points MoM to 41.4% in February, down 7.7 percentage points YoY. After aluminum prices surged to a record high at the end of January, they saw a sharp correction in early February ahead of the Chinese New Year holiday, allowing aluminum billet processing fees in three regions to return to positive territory. However, high aluminum price fluctuations were always unfavorable to order stability for processing enterprises. Downstream profile producers’ pre-holiday stockpiling fell short of expectations, and in-factory inventory at aluminum billet enterprises remained persistently high by early February. This was followed by downstream producers suspending operations for the Chinese New Year holiday, while most aluminum billet enterprises maintained normal production. As a result, in the first week after the holiday, in-factory inventory at China’s aluminum billet enterprises approached 500,000 mt, nearly tripling from pre-holiday levels. Under inventory and cash flow pressure, the aluminum billet supply side contracted further in February, and production came in slightly below expectations. Most enterprises proactively cut production by reducing procurement volume of liquid aluminum. In addition to enterprises that had already suspended production for maintenance continuing their shutdowns, a small number of billet plants with relatively high costs chose to take holidays during Chinese New Year, maintaining only low-load operations. Among them, Qinghai, Sichuan, and Henan each posted MoM declines of more than 40%.

Looking ahead to March, downstream profile enterprises had basically completed the resumption of work after the Lantern Festival, and both purchase willingness and procurement intensity for raw materials improved in the first week of March, with transactions in the aluminum billet market entering a phase of accelerated recovery. However, as the construction profile sector remained sluggish, end-use demand was still unlikely to see any substantive improvement. Processing fees for construction-grade billets of 6063 alloy, which remained the mainstream low-priced product in the market, were hardly optimistic. They are expected to remain below the cost line after the holiday, continuing the trend seen since Q1, though the center is expected to rise slowly from low levels. It is worth noting that as the PV and battery sectors entered a sprint period for export order grabbing, orders for industrial billets will recover, providing some support to China’s aluminum billet supply side in March. On the inventory side, with downstream operations resuming after the holiday and road transportation returning to normal, road shipments surged. Coupled with limited downstream stocking ahead of this year’s Chinese New Year, weekly in-factory inventory in the primary aluminum billet industry had fallen by more than 100,000 mt from the post-holiday high as of this week, for a cumulative decline of more than 20%. Based on the proportion of liquid aluminum in China, production expectations among sampled aluminum billet enterprises, and post-holiday performance of social inventory and in-factory inventory, SMM expects China’s aluminum billet production in March to rebound sharply to around 1.5 million mt, with the operating rate rising to about 55.7%, likely returning to the peak-season level seen in the same period in previous years.

(March production data are only forecast values. Data source statement: Except for public information, all other data are processed and derived by SMM based on public information, market communication, and SMM's internal database models, and are for reference only and do not constitute decision-making advice.)