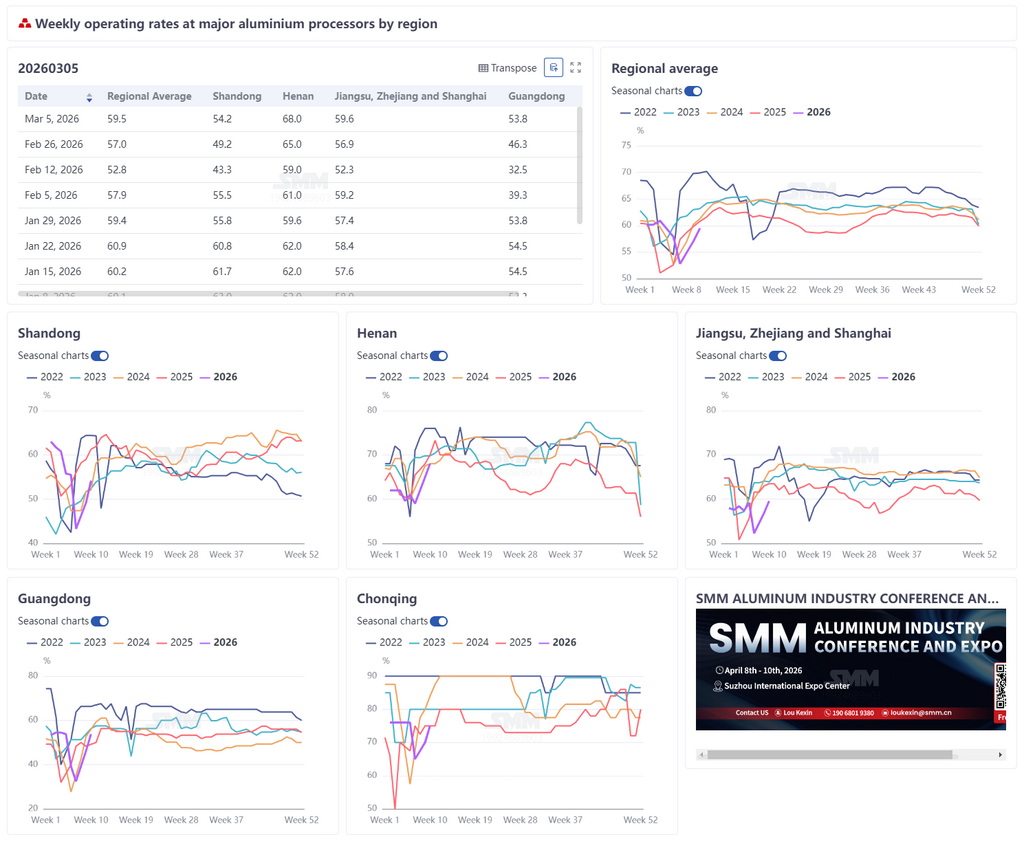

March 5, 2026:

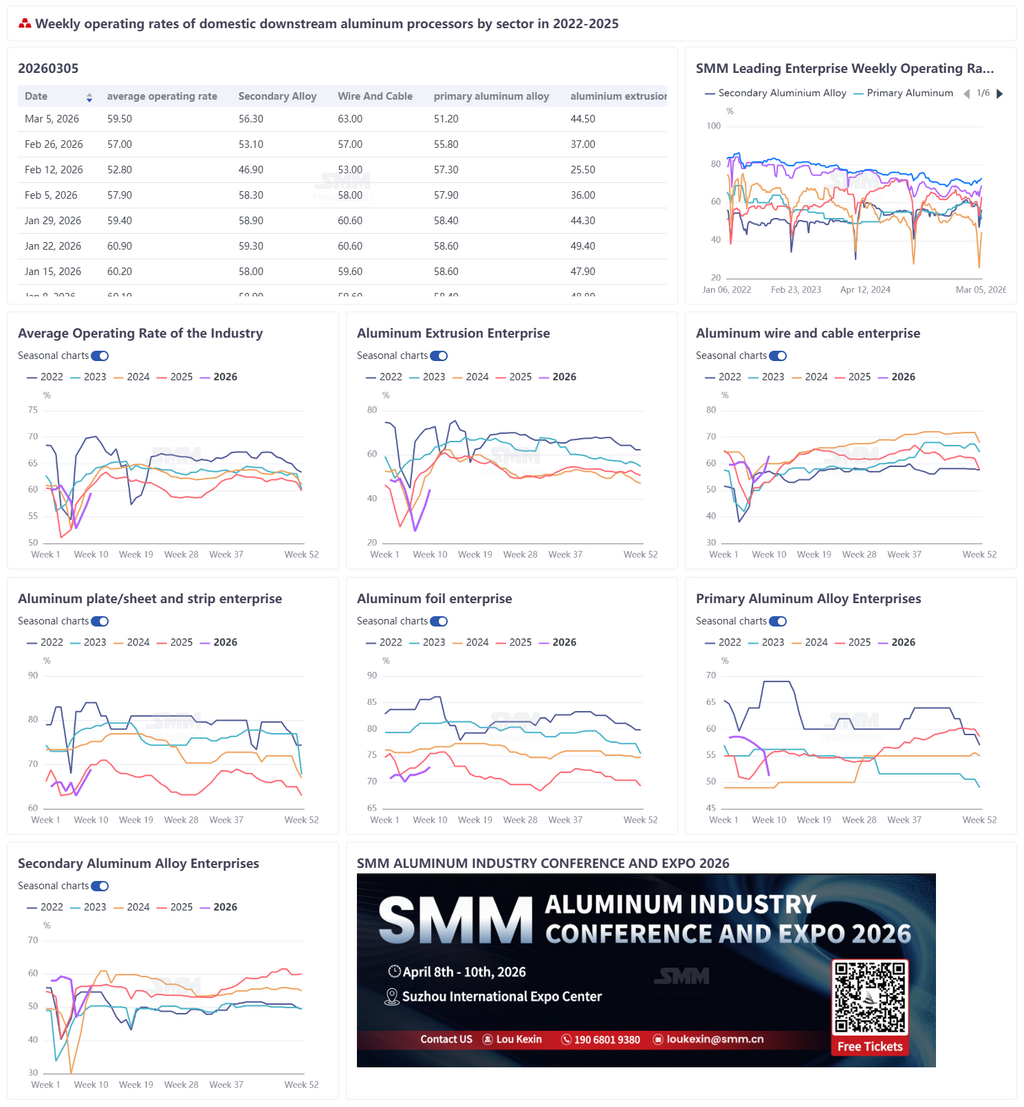

This week, the weekly operating rate of leading downstream aluminum processing enterprises in China rebounded by 2.5 percentage points WoW to 59.5%. Overall, post-holiday work resumption progressed steadily, but performance diverged markedly across segments due to high aluminum prices and uneven demand recovery. The operating rate of primary aluminum alloy was 51.2%, down 4.6 percentage points WoW; elevated inventories, enterprise destocking, and production line upgrades weighed on operations, while high aluminum prices curbed purchasing and transactions were sluggish. The operating rate of leading aluminum plate/sheet and strip enterprises was 69.0%, up 2 percentage points WoW; improving demand for can stock, autos, and batteries boosted operations, but construction-side work resumption was relatively slow, creating a tug-of-war between high aluminum prices and peak-season demand. The operating rate of aluminum wire and cable climbed rapidly to 63%, up sharply by 6 percentage points, with a notable acceleration in work resumption amid the power grid peak season and saturated UHV orders. The operating rate of aluminum extrusion was 44.5%, rebounding by 7.5 percentage points; industrial extrusion was supported by PV and autos, while construction extrusion remained weak. The operating rate of leading aluminum foil enterprises was 72.9%, up 0.8 percentage points WoW; demand for food, pharmaceutical foil, and air-conditioner foil improved, and policies and orders supported operations. The operating rate of leading secondary aluminum enterprises was 56.3%, rebounding by 3.1 percentage points WoW; work resumption advanced steadily, but demand was average and transactions were relatively cautious. SMM expected that, in the short term, industry operating rates would gradually recover along with downstream work resumption, but the dampening effect of high aluminum prices on consumption should not be underestimated. Overall, the market showed a differentiated recovery and a fluctuate upward trend; going forward, close attention should be paid to the pace of end-use work resumption, inventory digestion, and order releases.

Primary aluminum alloy: This week, the operating rate of the primary aluminum alloy industry was 51.2%, down 4.6 percentage points WoW. The pullback in operating rates was mainly driven by two factors: first, downstream demand had remained weak since the Chinese New Year, while enterprises generally maintained their production pace to ensure liquid aluminum conversion, leading to the accumulation of finished product inventories to high levels; this week, some enterprises focused on destocking and moderately reduced operating loads. Second, one enterprise temporarily suspended production for production line upgrades, which also suppressed the overall industry operating rate. Meanwhile, as aluminum prices continued to rise recently, fear of high prices intensified downstream and purchase willingness became more cautious; market transactions were mostly centered on long-term contract, and spot cargo trading was relatively sluggish. Looking ahead to next week, as post-holiday demand gradually recovers—especially with procurement in end-use sectors such as automotive wheel hubs expected to warm up slowly—the industry operating rate was expected to see a slight rebound. The recovery pace was slower than in previous years, and overall market transactions were relatively sluggish. Meanwhile, some enterprises relied on the consumption of earlier inventories, further suppressing spot purchasing willingness. Looking ahead to next week, the industry operating rate was expected to remain at the current level, and the market was still expected to stay in the doldrums. Going forward, attention should be paid to the pace of downstream work resumption and inventory digestion.

Aluminum plate/sheet and strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises rose by 2 percentage points WoW to 69.0%. On the operations side, with March officially beginning, the industry gradually entered the traditional peak season. In terms of orders, demand for products such as can stock, autos, and batteries continued to recover, prompting some enterprises to raise operating rates. In addition, the Two Sessions policy initiative to “deeply implement the special action to boost consumption” was gaining traction, supporting expectations for consumption growth in sectors such as autos and home appliances. However, the pace of work resumption in downstream construction was relatively slow and was expected to be largely completed by mid-March; it would still take time for orders related to curtain wall panels and the like to recover. Finished product inventories rose in the short term as leading enterprises basically did not halt production during the Chinese New Year; shipments were now being arranged gradually as logistics recovered, and inventories were expected to return to normal standing levels in mid-to-late March. On the other hand, aluminum prices surged by 1,710 yuan/mt mid-week, and wait-and-see sentiment among downstream clients intensified, suppressing the release of some peak-season orders. In the short term, the recovery in peak-season demand and high aluminum prices formed a two-way tug-of-war, and the operating rate of leading aluminum plate/sheet and strip enterprises was expected to fluctuate upward.

Aluminum wire and cable: After the Lantern Festival, the weekly operating rate of China’s aluminum wire and cable industry climbed rapidly to 63%, up sharply by 6 percentage points WoW, with a notable acceleration in work resumption. Driven by the start of the power grid cargo pick-up peak season and strong order demand, the industry quickly transitioned from the Chinese New Year off-season to a peak-season pace; UHV and overhead line orders remained saturated, and the capacity utilization rate rose significantly. Some enterprises launched outsourced production to ensure delivery pace as cargo pick-up demand surged. With ample orders on hand, leading aluminum wire and cable enterprises had favorable Q1 cargo pick-up expectations and full production schedules. Supported by orders, the industry operating rate was expected to fluctuate at highs, with capacity utilization rate likely to rise further; industry prosperity was expected to extend into Q2, injecting steady growth momentum into the aluminum wire and cable market.

Aluminum extrusion: This week, the domestic extrusion operating rate came in at 44.5%, rebounding by 7.5 percentage points WoW. After the Lantern Festival, enterprises resumed production one after another; as workers gradually returned to their posts, the industry basically returned to normal pre-holiday production levels. By product, construction extrusion remained generally weak; only some large extrusion plants in South China reported that order backlogs during the Chinese New Year provided some support to this week’s construction extrusion operations. For industrial extrusion, PV- and auto-related orders were relatively stable, serving as the main support for enterprise operations; a leading PV frame enterprise said the high operating trend was expected to continue until mid-March. Looking ahead to next week, aluminum prices had risen recently amid fluctuations in the international situation, and enterprises reported fewer new orders recently, with no clear improvement in end-use demand. High aluminum prices would further suppress end-use consumption; in the short term, the extrusion market was expected to be generally stable with slight fall, and operating rates were expected to run generally stable with slight fall.

Aluminum foil: This week, the operating rate of leading aluminum foil enterprises rose by 0.8 percentage points WoW to 72.9%. On the operations side, as the traditional peak season began in March, overall industry operations were stable. On the order side, demand for food packaging foil and pharmaceutical foil maintained peak-season momentum, and demand for air-conditioner foil also began to recover. In addition, adjustments to the export tax rebate policy for batteries lifted short-term demand for battery foil, brazing sheet foil, and related products. With ample overall orders on hand, leading enterprises effectively supported a steady rise in operating rates; although indirectly affected by aluminum price fluctuations, overall demand resilience remained strong. Looking ahead to next week, as peak-season demand continued to be released, together with policy benefits and order support, the operating rate of leading aluminum foil enterprises was expected to continue rising.

Secondary aluminum: This week, the operating rate of leading secondary aluminum enterprises rebounded by 3.1 percentage points WoW to 56.3%, with post-holiday work resumption and production resumptions progressing steadily. As enterprises that had previously suspended production completed furnace drying and equipment commissioning, production gradually recovered, lifting the overall industry operating level further. However, some enterprises had not yet fully returned to pre-holiday levels, and the overall pace of supply release was relatively mild. Current end-use demand recovery was average; coupled with consecutive price increases, downstream purchasing sentiment became more cautious, with restocking mainly based on small, rigid-demand orders. Overall transaction volume increases were limited, and the boost to production growth was relatively weak. After March, as work resumption and production resumptions across the industry chain continued to deepen, the production pace of secondary aluminum enterprises was expected to recover further; the industry operating rate was expected to continue rebounding steadily and gradually move closer to normal pre-holiday levels. In the short term, key attention should be paid to the strength of end-use consumption recovery and raw material circulation.