Menurut Xinhua News Agency, seiring eskalasi konflik AS-Iran, Korps Garda Revolusi Islam Iran mengumumkan penutupan Selat Hormuz pada malam 28 Februari. Banyak pemilik tanker dan pedagang telah menangguhkan transportasi melalui selat tersebut. Ini adalah pertama kalinya dalam beberapa tahun terakhir jalur transportasi energi dan kimia global inti menghadapi penangguhan substansial. Sebagai "tenggorokan" perdagangan belerang global, gangguan ini akan langsung memutus saluran ekspor belerang Timur Tengah dan menciptakan reaksi berantai yang mempengaruhi produksi MHP Indonesia dan industri pupuk fosfat China, keduanya sangat bergantung pada sumber daya Timur Tengah.

I. Selat Hormuz: Jalur "Pembuluh Nadi" Ekspor Belerang Timur Tengah Terputus, Kapasitas Rute Alternatif Terbatas

Selat Hormuz adalah jalur lalu lintas mutlak untuk perdagangan belerang global, dan penutupannya akan memiliki dampak "tingkat magnitudo" terhadap ekspor belerang Timur Tengah.

1. Perdagangan Belerang Global Sangat Bergantung Pada Jalur Ini

Dalam perdagangan belerang laut global, 50% muatan (sekitar 20 juta ton per tahun) berasal dari wilayah Teluk Persia di Timur Tengah dan harus melewati Selat Hormuz untuk mencapai pasar global. Negara-negara ekspor utama termasuk Arab Saudi, UAE, Qatar, Kuwait, dan Iran.

2. Semua Pelabuhan Ekspor Utama Tertutup

Pelabuhan ekspor belerang inti di Timur Tengah—Ruwais di UAE, Jubail dan Ras al-Khair di Arab Saudi, Ras Laffan di Qatar, Al Zour dan Shuaiba di Kuwait, serta Bandar Imam Khomeini di Iran—semuanya perlu mengangkut belerang mereka melalui Teluk Persia dan kemudian melalui Selat Hormuz ke Samudera Hindia. Penutupan selat berarti belerang dari pelabuhan-pelabuhan tersebut tidak dapat dimuat dan diekspor.

3. Kapasitas Rute Alternatif Sangat Terbatas

Meskipun ada pilihan untuk menghindari Selat Hormuz, operasionalnya sulit dilakukan secara besar-besaran:

Pelabuhan Fujairah, UAE: Terletak di luar selat di Teluk Oman, tetapi jauh dari area produksi utama di Teluk Persia, dengan biaya transportasi darat yang tinggi dan kapasitas terbatas, dan sulit untuk memprioritaskan belerang curah selama krisis.

Pelabuhan Laut Merah Arab Saudi: Sulfur dapat diangkut darat ke Pelabuhan Yanbu, tetapi pengangkutan jarak jauh darat menghadapi tantangan ekonomi dan operasional yang signifikan.

II. MHP Indonesia: Sulfur Timur Tengah sebagai Sumber Bahan Pendukung Inti, Gangguan Logistik Akan Langsung Meningkatkan Biaya Produksi

Sebagai situs produksi utama untuk bahan nikel-kobalt energi baru global (MHP), proyek HPAL Indonesia sangat bergantung pada sulfur dari Timur Tengah. Gangguan ini akan langsung mempengaruhi biaya produksi dan stabilitas pasokan MHP.

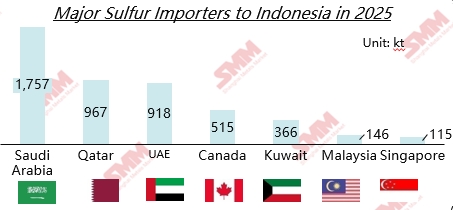

1. Konsentrasi Impor Sulfur yang Tinggi di Indonesia

Menurut data bea cukai Indonesia, lebih dari 75% impor sulfur Indonesia pada tahun 2025 berasal dari Timur Tengah. Struktur pasokan yang sangat terkonsentrasi ini berarti bahwa setelah penutupan Selat Hormuz, sumber bahan baku inti untuk proyek MHP Indonesia akan dipotong secara tepat.

2. Permintaan Rigid untuk Produksi MHP

Berdasarkan rata-rata industri, produksi 1 ton MHP membutuhkan sekitar 11,7 ton sulfur. Meskipun tanah longsor baru-baru ini di kawasan industri Indonesia telah mengganggu beberapa proyek, menyebabkan operasi dengan beban rendah dan permintaan hilir yang tidak pasti, proyek MHP lainnya yang ada dan baru masih memiliki permintaan rigid yang signifikan untuk sulfur.

3. Mekanisme Transmisi Biaya yang Diperkuat

Dampak biaya langsung: SMM memperkirakan bahwa pada Januari 2026, sulfur mencapai 41% dari biaya produksi MHP. Jika harga sulfur terus meningkat karena gangguan pasokan, biaya sulfur dalam MHP juga akan meningkat, menekan margin keuntungan proyek.

Biaya pembelian yang melonjak: Pembeli Indonesia akan dipaksa untuk bersaing dengan pembeli global untuk pasokan non-Timur Tengah yang terbatas. Selain itu, premi asuransi yang meningkat dan biaya pengiriman yang lebih tinggi akibat rute alternatif akan semakin mendorong biaya tiba.

III. Dampak Harga yang Diperluas: Depleksi Cepat Stok Sulfur China Akan Lebih Lanjut Mendorong Harga Naik

Sebagai importir sulfur terbesar di dunia, China memiliki ketergantungan struktural pada sumber daya Timur Tengah. Gangguan ini akan langsung mempengaruhi pasokan sulfur domestik dan produksi pupuk fosfat hilir, semakin mendorong kenaikan harga sulfur.

1. Ketergantungan Impor Sangat Tinggi

Ketergantungan eksternal Tiongkok terhadap belerang telah lama berada di kisaran 50%-53%. Data bea cukai menunjukkan bahwa pada tahun 2025, Timur Tengah menyumbang 56,2% impor belerang Tiongkok, yang berarti lebih dari setengah logistik impor belerang akan terpengaruh.

2. Permintaan Rigid untuk Persiapan Pupuk Musim Semi

Saat ini, merupakan periode kritis untuk persiapan pupuk musim semi, di mana ada permintaan rigid untuk belerang dalam produksi pupuk fosfat. Perusahaan diammonium fosfat hulu mempertahankan tingkat operasi yang tinggi, dengan permintaan pengisian ulang dilepaskan, dan lelang umumnya ditutup dengan harga premium, menunjukkan niat kuat pedagang untuk menahan harga.

3. Penurunan Stok Dipercepat, Pasokan Alternatif Terbatas

Data keuangan iFinD menunjukkan bahwa per tanggal 28 Februari, total stok pelabuhan belerang Tiongkok adalah 1,7398 juta ton. Dengan konsumsi rata-rata bulanan 1,4-1,5 juta ton selama musim cangkul, stok saat ini hanya dapat mendukung 1,2-1,5 bulan. Jika mempertimbangkan stok pabrik dan barang dalam perjalanan, waktu dukungan diperpanjang menjadi 1,5-2 bulan. Jika blokade selat berlanjut, stok akan cepat habis selama puncak musim cangkul Maret-April. Meskipun Tiongkok dapat mencari sumber alternatif dari Amerika Utara, Laut Hitam, dan Asia Tengah, jarak transportasi yang lebih jauh, biaya angkut yang lebih tinggi, dan batasan kontrak akan membatasi kecepatan pengisian ulang.

Ⅳ. Peringatan Risiko Hulu

1. Bahan Baterai Kendaraan Listrik (NEV):Sebagai bahan baku inti untuk prekursor katoda ternary, peningkatan biaya MHP akan ditransfer sepanjang rantai industri ke bahan katoda dan sel baterai, akhirnya mempengaruhi biaya manufaktur NEV.

2. Pupuk Fosfat: 56% impor belerang Tiongkok menghadapi risiko gangguan pasokan. Stok pelabuhan domestik akan cepat habis selama puncak persiapan pertanian musim semi, dengan harga belerang diperkirakan akan melampaui rekor tertinggi sebelumnya dan ditransfer ke harga pupuk fosfat hulu, akhirnya mendorong naiknya biaya produksi pertanian.

3. Durasi Adalah Variabel Inti:

Jika penutupan bersifat jangka pendek (1-2 bulan): Dampaknya akan terfokus pada fluktuasi harga, yang dapat ditangani perusahaan melalui penyesuaian stok dan substitusi bahan baku.

Jika penghentian berlangsung jangka panjang (lebih dari 3 bulan): Hal ini akan menyebabkan kesenjangan pasokan yang terus membesar. Beberapa perusahaan yang bergantung pada perjanjian jangka panjang dengan Timur Tengah mungkin mengalami kekurangan bahan baku, penurunan beban fasilitas, atau bahkan penghentian. Rantai industri belerang global dan sektor hilirnya akan mengalami restrukturisasi yang mendalam.

![[Analisis SMM] Keinginan Membeli di Hilir Lemah; Utang Produk Antara Lesu Minggu Ini](https://imgqn.smm.cn/usercenter/NHXhQ20251217171733.jpg)