SMM February 28 News:

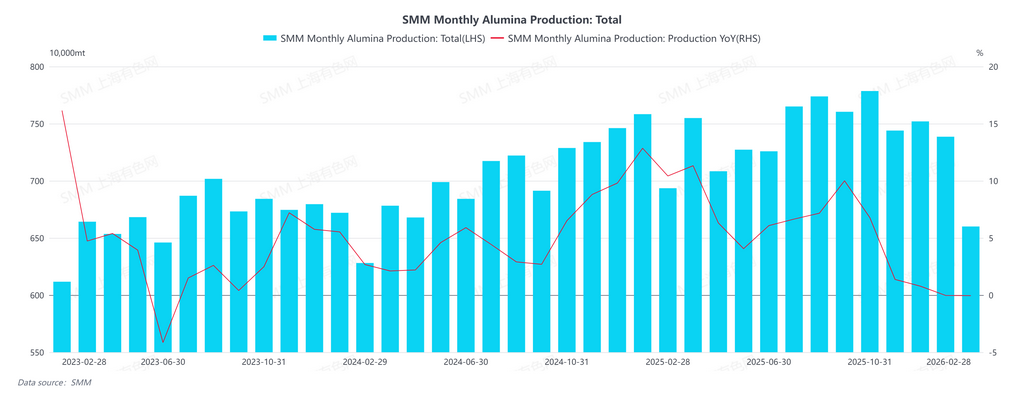

In February 2026, China's metallurgical-grade alumina output decreased by 10.6% month-on-month and also fell by 4.83% year-on-year. By the end of February, the national installed capacity stood at approximately 110.32 million mt, while operating capacity decreased by 1.06% month-on-month and 4.83% year-on-year, indicating a continued downward trend for the industry.

The main reasons for the output decline this month were, on one hand, the concentrated implementation of maintenance and production cuts by enterprises, and on the other hand, the fewer natural days in February, which further impacted production schedules. Around the middle of the month, a company in the northern region implemented large-scale production cuts, coupled with equipment maintenance and production line upgrades by some enterprises. Simultaneously, some southern companies reduced operating loads, leading to a slight contraction in overall monthly output.

Looking ahead to March, the overall oversupply situation in the alumina market is unlikely to change in the short term. Although the earlier maintenance and production cuts have led to a decrease in enterprise inventories and slightly eased overall shipment pressure, operational pressure within the industry persists. In March, some enterprises may continue to carry out maintenance and production line upgrades, and the industry will enter a phase of gradual destocking. However, the gradual release of new production capacity in the Guangxi region will offset some of the reductions, and overall operating capacity is expected to show a slow downward trend. Overall, it is projected that operating capacity in March will be approximately 85.11 million mt, and the market will still face oversupply pressure.

![SHFE Aluminum Edged Up After Halting Its Decline, Spot Aluminum Stabilized and Improved [SMM South China Spot Aluminum Daily Review]](https://imgqn.smm.cn/usercenter/tkWbz20251217171654.jpg)