> From 2021 to 2024, driven by the booming manufacturing sector and the "surge" in the steel export market, China's hot-rolled coil industry rapidly rose.

In 2021, with the official implementation of the "three red lines" policy in real estate, the property sector entered a comprehensive downturn. Steel mill profitability in construction materials deteriorated, prompting mills to gradually shift their focus to sheets & plates, led by hot-rolled coils. At the same time, the manufacturing sector gradually took over as the center of economic growth. China's manufacturing investment experienced high fluctuations from 2021 to 2024, with major industries such as automotive and home appliances setting sail—production and sales continued to climb. According to National Bureau of Statistics data, China's automotive production reached 31.26 million units in 2024, up 39% from 2021, while the combined output of four major home appliances reached 695.24 million units in the same year, an increase of 37% compared to 2021.

While China's domestic manufacturing industry was developing at a high speed, benefiting from the competitive prices of Chinese steel, a well-developed and stable supply chain system for downstream manufacturing and processing, both direct and indirect steel exports also ushered in new opportunities...

Despite the high base in 2024, according to data from the General Administration of Customs, China's total steel exports reached 119.019 million mt in 2025, up 7.5% YoY. Based on the SMM indirect steel export model, China's indirect steel exports totaled 149.6407 million mt in 2025, an increase of 19.01% YoY. Looking solely at the full year of 2024, China's hot-rolled coil (HRC) exports reached 29.88 million mt, up 30% YoY, accounting for nearly one-third of China's total steel exports! However, influenced by changes in global supply and demand and escalating trade barriers, this proportion dropped to around 21% in 2025, with some volume shifting to coated products.

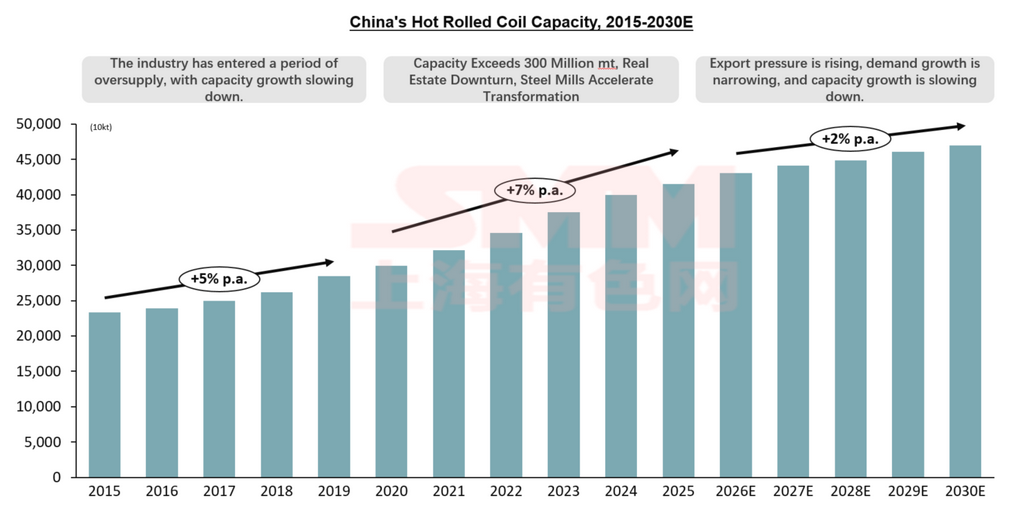

From 2021 to 2024, on one hand, core steel demand shifted from real estate to high-end manufacturing; on the other hand, direct and indirect steel exports strengthened. From a demand perspective, this provided strong support for the sheets & plates industry chain related to HRC and cold-rolled & coated products. Consequently, China's HRC capacity and production grew rapidly during the 2021-2024 period, with HRC capacity advancing from 300 million mt to 400 million mt.

> Capacity Enters the "400 Million mt" Era, HRC Capacity Growth in China May Gradually Slow Down, 2028-2030

From 2021 to 2025, driven by shifts in core demand structure and upgrades in export trade, domestic HRC capacity entered a new peak period of commissioning. According to SMM statistics, by the end of 2025, China's HRC capacity reached approximately 410 million mt, up 4% compared with the same period in 2024 and nearly 39% higher than the "300 million mt" level in 2020.

Data source: SMM

According to SMM statistics, from 2026 to 2030, China still has nearly 55 million mt of capacity under construction or planning. It is estimated that approximately 15.9 million mt of capacity will be commissioned in 2026, and around 10.6 million mt of capacity is expected to be released into the market in 2027.

Given that many projects remain pending, the peak period for new hot-rolled coil capacity commissioning is likely to occur from 2026 to 2027. Close attention should be paid to the approval and implementation progress of these projects in the subsequent period.

> In the Next Five Years, China Is Expected to Experience a Final Peak in Hot-Rolled Capacity Commissioning Around 2026–2027

SMM compiled hot-rolled coil projects scheduled for commissioning in domestic and overseas markets from 2026 to 2030. The construction of new projects in overseas markets is mainly concentrated in Asia, Africa, and other regions, with a round of concentrated overseas capacity release expected around 2026-2027.

Domestically, looking ahead to the next five years, considering that many new production line projects remain pending while China's hot-rolled coil overcapacity persists, the continuous capacity additions will further intensify the supply-demand imbalance. Additionally, since 2024, overseas trade sanctions on China's hot-rolled coils and cold-rolled/galvanized products have been escalating. Affected by multiple factors, 2026-2027 may become the final peak period for hot-rolled coil capacity commissioning in China.

![Risks in the Ferrous Metals Sector Began to Accumulate [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/yBlDX20251217171747.jpg)