Following the Chinese New Year holiday, the electrolytic copper market has entered its traditional post-holiday resumption validation period. The Yangtze River Delta region, as the national core for copper processing and consumption, serves as a bellwether for assessing supply-demand dynamics through the operating rates and raw material procurement pace of its leading enterprises. Our survey indicates that the region is currently characterized by "excessively high inventory accumulation, a divergence in resumption rates, and cautiously recovering procurement sentiment," leading to a downward revision of market expectations for the start of the peak season in March.

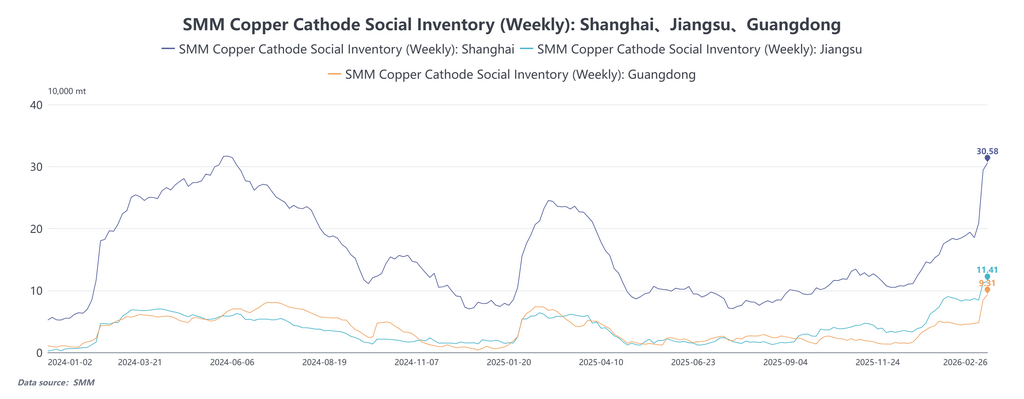

According to SMM research, as of February 26, 2026, social inventories of electrolytic copper stood at 531,700 metric tons, an increase of 178,100 metric tons from February 12. This pace of inventory buildup significantly exceeds levels seen in previous years. The Yangtze River Delta region contributed the bulk of this increase: inventories in Shanghai rose to 305,800 metric tons, while Jiangsu Province reached 93,100 metric tons, up by 97,500 metric tons and 45,200 metric tons respectively from February 12. This round of inventory accumulation is characterized as "passive delivery into warehouses." As the first trading day after the holiday (February 25) coincided with the last trading day for the SHFE 2602 contract, smelters concentrated their deliverable cargoes into exchange-designated warehouses just before the holiday. This led to an increase of 80,400 metric tons in SHFE copper warrants, bringing the total to 277,100 metric tons, a portion temporarily locked in the form of warrants. Concurrently, with the narrowing of import losses and the emergence of a profit window before the holiday, arrivals of imported copper in March are expected to increase, putting dual pressure on domestic social inventories from both domestic production and imported supply.

Based on operational feedback from enterprises, downstream processing sectors in the Yangtze River Delta exhibit significant contrasting dynamics:

The battery materials sector maintains robust performance. Copper foil producers either had short production stoppages or operated continuously during the holiday. Downstream battery manufacturers are running at high utilization rates, with some reporting that their March production schedules already display peak-season characteristics. This sustains rigid demand for purchasing electrolytic copper.

In contrast, the resumption of operations in the traditional cable and copper processing sectors is sluggish. Performance in traditional copper-consuming segments like wire and cable, copper rod, and copper tube is relatively weak. In the first week after the holiday, leading cable companies saw a decline in new orders. Apart from high copper prices dampening downstream acceptance, the fact that end-user projects have not yet fully commenced is a major constraint. According to enterprise feedback, construction and infrastructure projects typically resume gradually after the Lantern Festival (which falls after the standard holiday), and the market is currently in a lull for new orders. Copper rod processors generally have high finished goods inventory, and some orders from before the holiday are still pending delivery. Consequently, their procurement of electrolytic copper primarily focuses on consuming existing inventory and making ad-hoc spot purchases based on immediate needs, showing a weak willingness to stock up on raw materials.

Overall, downstream consumption in the region currently presents a pattern of rigid demand from the battery sector versus pending demand from the cable sector. The transmission of genuine end-user consumption to the electrolytic copper procurement stage will still require time.

According to information obtained by SMM through communication with enterprises:

Enterprise 1: Normal operations resumed on the 6th day of the first lunar month. The downstream battery industry is operating at a high utilization rate; current copper foil production has increased from 20% to approximately 50% compared to previous levels. However, the wire and cable sector has seen relatively few new orders recently. The main reasons are persistently high copper prices, and, consistent with previous years, end-user projects typically do not fully commence until after the Lantern Festival, leading to a temporary lag in demand transmission.

Enterprise 2: The company reached full production capacity immediately after resuming work on the 6th day of the first lunar month, requiring approximately 1,000 tons of electrolytic copper daily. Raw material inventory is maintained at a reasonable level, adopting a cautious procurement strategy of daily spot purchases. However, finished goods inventory is higher than before the holiday, with some pre-holiday orders still pending delivery. Regarding downstream orders, pre-holiday withdrawals were relatively concentrated, while the performance of new orders after the holiday is weak, as some downstream customers have yet to restart operations.

Enterprise 3: Production workshops ran continuously during the Chinese New Year. Recently, production has remained stable, with orders from key clients holding steady. Raw material inventory is kept at a low level, and electrolytic copper purchases are made based on order volume. However, the volume of recent spot purchases has decreased compared to the previous period.

Enterprise 4: Recently, there has been a decrease in new downstream orders, resulting in sluggish market transactions. Pressure from finished goods inventory is not significant, but some pre-holiday orders are still awaiting delivery. Raw material inventory is maintained within a normal and manageable range.

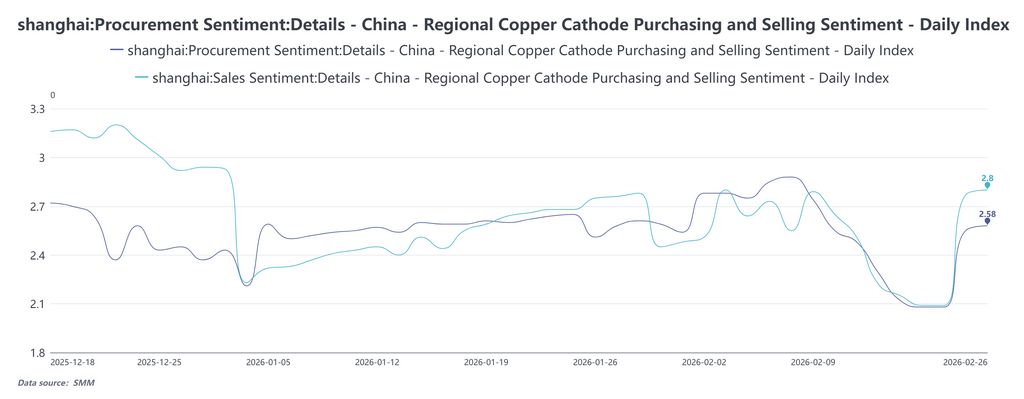

On February 24, the Purchasing Sentiment Index recorded 2.08, remaining in a weak range, indicating low enthusiasm among downstream companies for market inquiries in the first week after the holiday. Subsequently, it recovered day by day to 2.58 on February 26. Over the same period, the Shipment Sentiment Index rose from 2.09 on February 24 to 2.80 on February 26, showing a continuous upward trend and consistently remaining higher than the Purchasing Sentiment Index. Historical data can be queried in the database. This reflects that, as the resumption of work progresses, some rigid demand has begun to emerge, with certain downstream companies entering the market for inquiries. However, the absolute levels remain low, indicating limited acceptance of current copper prices among downstream users. Their stocking strategy remains predominantly "hand-to-mouth procurement." Holders, under pressure from high inventories, exhibit a strong willingness to liquidate, while market transactions are primarily circulating within the trading sphere, with genuine downstream offtake yet to pick up significantly.

Looking ahead, the unexpected inventory accumulation has already triggered a market correction to previous supply-demand expectations. In the short term, social inventories in the Yangtze River Delta region still face pressures from two fronts: first, the arrival of imported copper resources, and second, the need for time to digest high downstream finished goods inventories. Channels for inventory outflow are also obstructed, with LME inventories continuing to climb and maintaining a Contango structure, making it difficult to absorb the domestic surplus. A positive factor on the supply side lies in the concentrated maintenance window for domestic smelters during March-May in the first half of the year, with substantial impacts expected to emerge starting in April. If demand-side support materializes by then, an inventory drawdown cycle could potentially commence between late March and April. However, due to the exceptionally high post-holiday inventory starting point, even entering a destocking phase is unlikely to replicate the high BACK structure and high premiums seen during the same periods in previous years. Overall, the post-holiday resumption in the Yangtze River Delta region is characterized by high inventory levels, cautious procurement, and pending orders. The market is now awaiting the substantive return of end-user orders after the Lantern Festival. The short-term price-driving logic may shift from validation of "expected destocking" to "actual destocking."

![Domestic Trade Premiums Hold Steady and Rise, Fundamental Consumption Maintains Resilience [SMM Copper Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/qBqQv20251217171708.jpg)