SMM February 24 News:

In 2025, China's smelting and refining capacity grew, while the TC for copper concentrates continued to deteriorate. Against this backdrop, smelters were compelled to adjust their raw material mix, with copper scrap, blister copper, and anode plates becoming key substitutes and supplements.

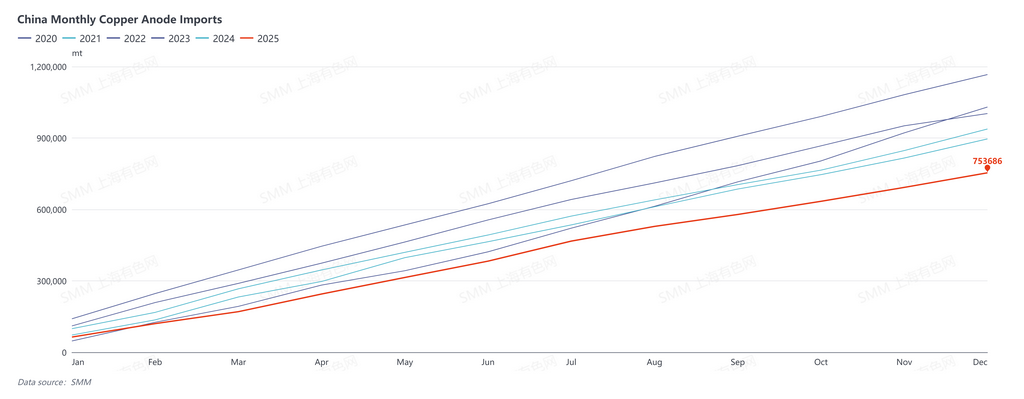

Due to factors such as stagnant capacity among global copper anode suppliers and expanding demand for copper anode other countries, China's full-year copper anode imports in 2025 fell significantly YoY, hitting a nine-year low since 2017. According to data from the General Administration of Customs, cumulative copper anode imports (HS code: 74020000) from January to December 2025 totaled 753,700 mt, down 15.88% YoY.

The growth in China's domestic demand for copper anode diverged from the sharp decline in imports, a gap being filled by increased China's domestic supply and imported copper scrap.

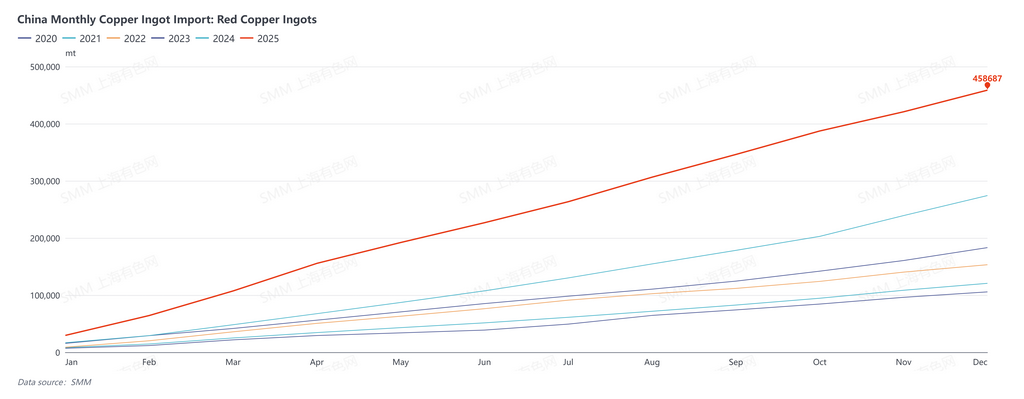

China's copper scrap imports from January to December 2025 reached 2.3427 million mt in physical content, up 4% YoY. Imports of scrap copper ingots (red/purple copper ingots) saw significant growth during the same period, with cumulative imports (HS code: 74031900) reaching 458,700 mt, up 67% YoY, indicating more imported scrap copper flowed into the smelting sector.

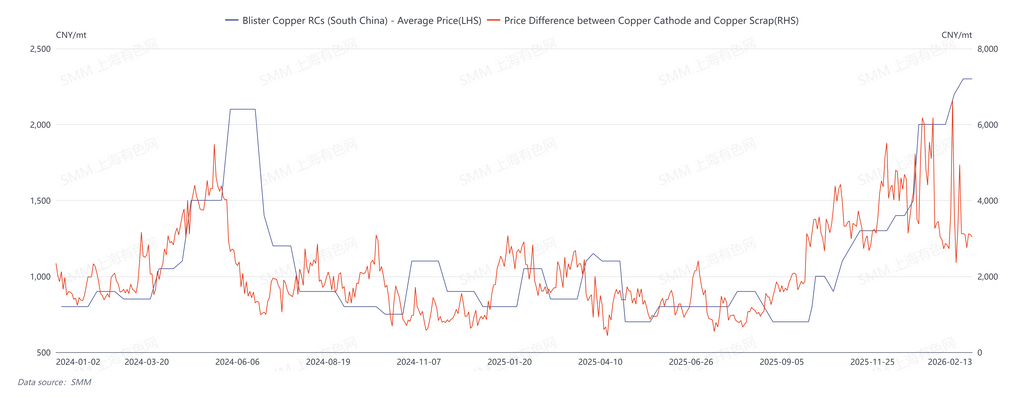

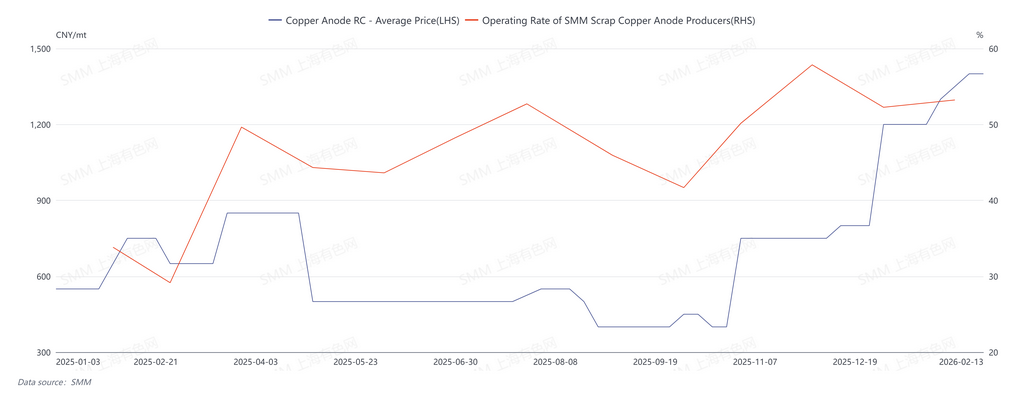

In China, despite frequent policy disruptions in the secondary copper industry throughout the year, the substantial rise in copper prices kept the price difference between primary metal and scrap consistently high. In contrast, processing demand and profits were weak, leading to an expansion of new capacity for scrap-derived copper anode domestically, with more secondary copper being channeled into smelting. Anode plate processing fees rose significantly. Coupled with the rapid climb in copper prices by the end of 2025, anode plate processing fees reached a peak before the 2026 Chinese New Year, averaging 1,400 yuan/mt, up 650 yuan/mt YoY.

SMM believes that in 2026, due to the shortage of copper concentrates, China's demand for scrap-derived copper anode will continue to grow. Although the Kamoa copper smelter in the DRC (with an annual blister copper capacity of 500,000 mt) commenced operations at the end of 2025, the 2026 blister copper RC, CIF China benchmark was finalized at $85/mt, down $10/mt from the 2025 benchmark of $95/mt. Copper anode imports in China are expected to rebound in 2026, but spot order supplements during the year will primarily come from domestic sources, with copper scrap supply remaining a critical factor.

![[SMM Analysis] China’s Sulphuric Acid Production and Sulphur/Sulphuric Acid Imports & Exports in H1 2026](https://imgqn.smm.cn/usercenter/OpmKJ20251217171712.jpg)

![[SMM Analysis] China’s Sulphuric Acid Production and Sulphur/Sulphuric Acid Imports & Exports in H1 2026 — Based on Data from National Bureau of Statistics (NBS) and Customs](https://imgqn.smm.cn/usercenter/eThpo20251217171723.jpeg)

![Copper prices surge sharply, exacerbating the off-season drag, and operating rates and order intake continue to pull back [SMM Enamelled Wire Market Weekly]](https://imgqn.smm.cn/usercenter/CaDcj20251217171711.jpg)