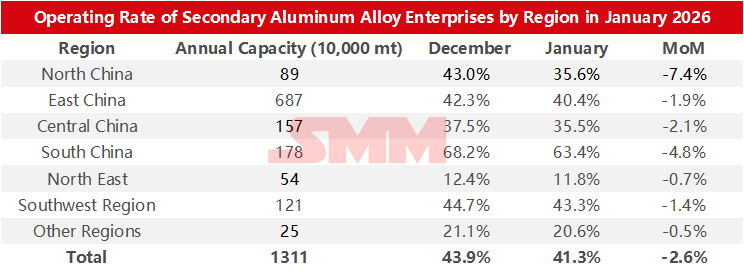

Survey Data on Operating Rates of Secondary Aluminum Alloy Enterprises by Region and Scale in January 2026:

According to the SMM survey, the operating rate of the secondary aluminum industry in January 2026 fell 2.6 percentage points MoM to 41.3%, but rose 7.2 percentage points YoY. The operating rates of enterprises across regions experienced varying degrees of pullback in January.

The operation of the secondary aluminum industry continued to be affected by multiple factors in January. On one hand, compliance checks on reverse invoicing intensified in some regions, forcing enterprises to shift their raw material procurement structure toward invoiced resources, which increased the cost of raw materials delivered to plants. With compressed profits, small and medium-sized enterprises were more inclined to respond to compliance pressure by proactively cutting production, conducting maintenance, or slowing down their procurement pace.

On the other hand, snowfall disrupted aluminum scrap recycling and cross-regional transportation. Coupled with ongoing environmental protection-driven production restrictions in parts of east China, north China, and southwest China that had not been fully lifted, the actual operating levels of enterprises were suppressed.

Demand-side constraints also emerged. January is traditionally an off-season, and with aluminum prices repeatedly hitting record highs, cost pressures on downstream die-casting enterprises increased significantly. However, end-user orders and price transmission were noticeably sluggish, forcing some enterprises to reduce production ahead of schedule and lower their pre-holiday stockpiling expectations. This led to a continued weakening in new orders for secondary aluminum plants, gradually revealing a supply-demand weakness on both sides.

From a YoY perspective, however, due to the later timing of the Chinese New Year in 2026, holiday disruptions in January were relatively limited, and the industry's overall operating performance remained significantly better than the same period last year.

Entering February, the industry will gradually enter a phased slowdown dominated by the Chinese New Year. Most enterprises will suspend production between February 5 and 13, with resumption of work concentrated after the eighth day of the first lunar month or after the Lantern Festival. The expected shutdown period is 8–20 days, with the average shutdown time about 2 days longer than last year. The extended shutdown period stems partly from intensified aluminum price fluctuations and increased profit uncertainty, and also reflects practical constraints such as widespread production cuts downstream, ongoing reverse invoicing policy restrictions, and the absence of significant relaxation in environmental protection-related controls. Overall, industry orders and the operating rate in the secondary aluminum sector are expected to drop significantly in February, and fundamental support for prices will further weaken.

![Secondary Aluminum Prices Were Expected to Face Downward Pressure and Pull Back in April[SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)

![Supported by Multiple Factors, Aluminum Fluoride Prices Rose Sharply in April [SMM Analysis]](https://imgqn.smm.cn/usercenter/DRlGu20251217171652.jpg)