SMM February 6:

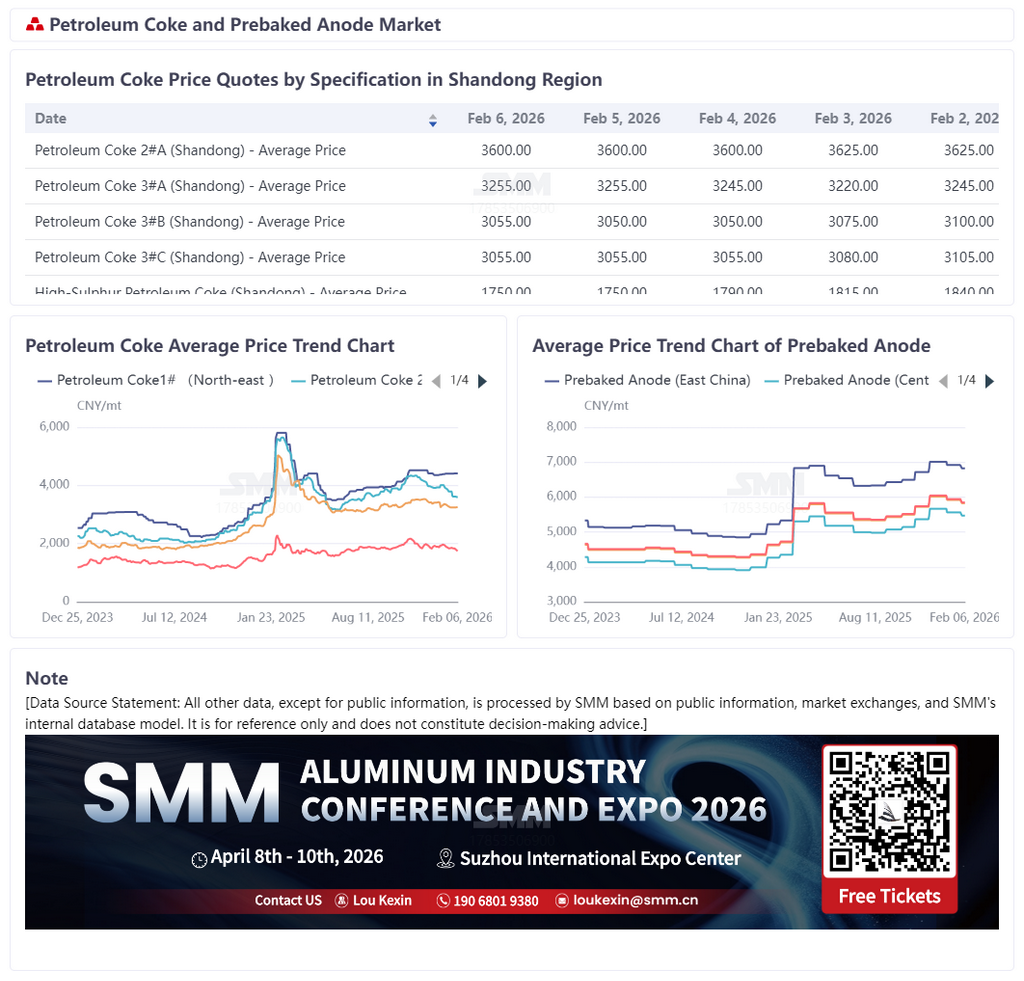

Prebaked Anode Market: Domestic and Export Prices Fall Together, Weak Cost Side Drags Down Future Market

In February 2026, prebaked anode prices mainly declined. In the domestic market, a Shandong aluminum enterprise set its February 2026 procurement benchmark price at 5,229 yuan/mt, down 2% MoM. In the export market, according to SMM surveys, prebaked anode export order prices in February mainly fell, with declines concentrated in the range of $10-20/mt.

Raw material side, since February, due to downstream aluminum carbon and anode material enterprises mainly restocking based on rigid demand, purchasing enthusiasm has been relatively moderate. Petroleum coke prices were generally stable with slight fall. Although post-holiday restocking provided some support, affected by supply-demand and cost factors, petroleum coke prices in February are expected to continue structural differentiation and an overall trend in the doldrums. In the coal tar pitch market, support from the cost side high-temperature coal tar loosened, and coal tar pitch prices mainly operated in the doldrums. Overall, the prebaked anode cost side was in the doldrums, and prebaked anode prices next month are expected to be slightly under pressure.

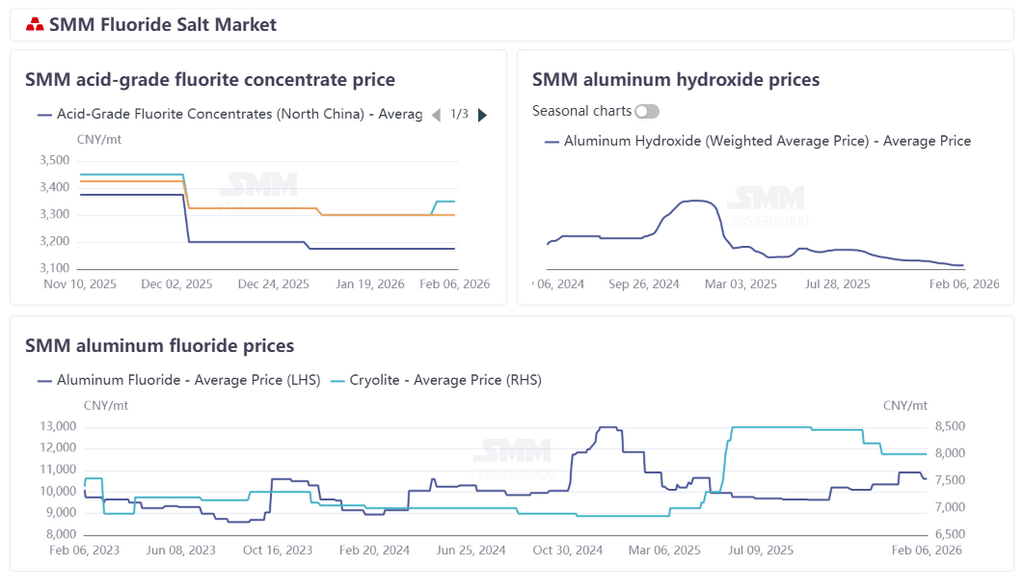

Aluminum Fluoride Market: Tender Pricing Decline Drives Prices Down, Weak Supply-Demand Constrains Future Recovery

The downstream aluminum benchmark enterprise's February 2026 tender pricing saw a decline, finally settling in the range of 10,480-10,550 yuan/mt, driving aluminum fluoride prices to generally follow with declines of 200-380 yuan/mt. Overall, the aluminum fluoride fundamentals failed to provide effective support for prices. Loosening costs combined with a weak supply-demand situation caused prices in February to fall under pressure.

The supporting effect from the raw material side significantly weakened, further constraining market trends. The support from raw materials such as fluorite and sulphuric acid was limited. The core intermediate hydrofluoric acid market experienced weak supply-demand around the Chinese New Year, with an unclear pace for post-holiday operating rate and demand recovery, greatly weakening the cost transmission effect. On the supply side, although the current industry operating rate has declined somewhat, spot inventory remains sufficient. Post-holiday production resumptions by enterprises will further release capacity, increasing supply pressure. On the demand side, only slight recovery was achieved relying on rigid demand restocking by aluminum enterprises, lacking substantial incremental support. Under multiple constraints, aluminum fluoride prices next month are highly likely to continue their weak trend.