SMM February 5 News:

Key Points:: This week (January 30 - February 5, 2026), Tesla's dry electrode process scaling represents a revolutionary breakthrough in manufacturing, while Lightyear Engine's "launch to mass production" is a bold declaration on the product side. Both point to the core challenges of industrialisation—engineering and cost. Meanwhile, deepening strategic cooperation along the supply chain, validation of new application scenarios, and continuous capital support are accelerating the formation of a multi-dimensional industrial ecosystem driven by material innovation, process renewal, and application traction.

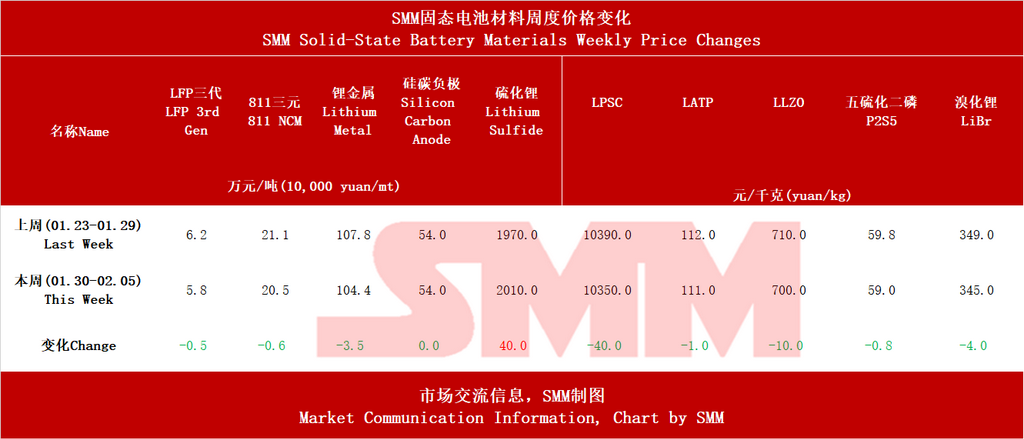

Preface: Weekly price situation, prices of common materials used in solid-state batteries and traditional lithium batteries have declined to varying degrees due to the rise in lithium chemical prices, while silicon carbon anode prices remain stable; in terms of electrolytes, battery-grade lithium sulphide prices have risen, with active cargo pick-up downstream, and other electrolyte materials and raw materials have seen minor fluctuations.

Weekly Solid-State Battery Industry Observation (1.29-2.03, 2026): Acceleration of Mass Production, Initial Signs of Ecosystem Competition

Core Summary:

I. Material Perspective: Intensified Competition in Electrolyte Industrialisation, Diverse Developments in Anode Technology

The material system, especially electrolytes and anodes, remains the core battlefield for determining the performance and cost of solid-state batteries.

1. Electrolytes: Sulfide Route Enters Pilot Sprint, Multiple Forces Increase Layout

Steady Progress by Domestic Enterprises: Leading electrolyte manufacturer Tinci confirmed that its sulfide electrolyte is in the pilot stage, indicating that traditional liquid system giants are extending into the solid-state field with their experience in chemical synthesis and large-scale production, making their progress highly noteworthy.

Overseas Giants Move Towards Mass Production: Japanese material giant Idemitsu Kosan made a final investment decision and initiated construction of a solid-state electrolyte pilot plant, marking a critical step from laboratory to large-scale production. Japan's deep accumulation in sulfide electrolytes is rapidly transforming into industrial advantages, which will have a profound impact on the global supply chain landscape.

Deepening Supply Chain Collaboration: SEMCORP and Gotion High-tech's strategic cooperation explicitly covers key materials such as "solid-state electrolytes." The deep integration between a traditional separator leader and a battery company aims to integrate material R&D and cell design capabilities, jointly tackling core issues like the electrolyte-electrode interface, and accelerating solution implementation.

2. Anodes: Silicon-Based Materials Ready for Industrialisation, Suitability for Solid-State Batteries Reaches Consensus

Anode company Shenzhen XFH clearly stated that its silicon carbon/silicon oxide anode technology has met the basic conditions for industrialisation, targeting applications in solid-state/semi-solid-state batteries. This indicates that after years of R&D, high-energy-density silicon-based anodes are no longer just a laboratory concept but are entering the pre-industrial phase of capacity building and customer introduction.

II. Battery and Manufacturing Perspective: From Process Revolution to Product Declaration, Diversification of Mass Production Paths

Significant events in battery manufacturing and products highlight diverse paths to mass production.

1. Manufacturing Process Revolution: Tesla Achieves Scale Production of Dry Electrodes

Event Essence: Musk announced the achievement of scale production of the dry electrode process, fundamentally disrupting traditional wet coating processes. Its core value lies in significantly simplifying procedures, reducing costs, increasing energy density, and perfectly matching next-generation high-activity electrode materials (such as silicon-based anodes and lithium metal anodes).

Industry Impact: This breakthrough not only benefits Tesla in cost reduction and efficiency improvement but also forces the entire lithium battery industry to accelerate process innovation. Despite challenges such as consistency control and patent barriers, the successful scale verification demonstrates the feasibility of the technology, pointing the industry towards a clear direction for cost reduction and efficiency improvement. Qingyan Nake's dry electrode equipment export to Japanese automakers further validates the global appeal of this process route.

2. Accelerated Product Implementation: From Two-Wheelers to Automotive Standards, Multi-Point Breakthroughs in Application Scenarios

High-Profile Launch: Lightyear Engine released an all-solid-state battery and declared "launch to mass production," first entering markets such as automotive start-stop systems and high-end electric motorcycles, where cost sensitivity is relatively low but requirements for lifespan and safety are high. This is a "high-profile, scenario-first" business model aimed at quickly establishing brand and technological benchmarks.

Pragmatic Gradual Validation: GAC Group plans to conduct small-batch vehicle tests with all-solid-state batteries in 2026, and Sunwoda expects to achieve mass production of all-solid-state batteries by 2027. This represents a reliable path of "steady validation and gradual introduction" by mainstream automakers and battery giants, complementing the aggressive strategies of startups.

Scenario-Based Demand Validation: Zhongxin DeGuo secured a 100 million yuan order from the food delivery rider market, with its solid-state cells passing rigorous tests (needle penetration, wide temperature range, long cycle life), proving that in semi-solid or solid-state technology paths, battery safety has reached or even exceeded the extreme requirements of specific commercial scenarios. This is a significant direct pull from market demand on technological products.

III. Cooperation and Ecosystem Perspective: Vertical Integration and Horizontal Crossover Become Mainstream

Supply chain cooperation models are deepening, and an ecosystem competition pattern is emerging.

1. Vertical Deep Binding: The strategic cooperation between SEMCORP (materials) and Gotion High-tech (batteries) is a typical example. Both parties will extend from collaborative material R&D to co-building zero-carbon factories and smart charging piles, indicating that competition has evolved from single products to integrated solutions encompassing "materials-battery-scenario."

2. Horizontal Cross-Border Empowerment: Guangdong Construction Engineering's joint bid win for a 3D solid-state lithium battery production base project shows that large construction engineering companies are deeply involved in solid-state battery line construction, reflecting that industrial investment has entered a substantial "heavy asset" capacity building phase.

IV. Capital Perspective: Continuous Active Financing Supports Long-Term Technological Development

The capital market continues to provide ammunition for solid-state battery innovation. SEVC POWER completed a new round of financing, with investors including professional investment institutions. This indicates that despite the long road to industrialisation, companies with core technological innovation capabilities can still attract capital, supporting the "long run" of R&D and capacity building.

V. Overseas Perspective: Continued Efforts by Japan and the US, Intensifying Global Competition

Overseas industry dynamics show clear acceleration signals.

Japan: Idemitsu Kosan's construction of a pilot plant is a key move from technological leadership to industrial leadership in sulfide solid-state electrolytes, aiming to consolidate its core position in the global supply chain.

US: Tesla's dry electrode breakthrough is another example of the US leading global battery manufacturing process innovation, demonstrating its ability to disrupt existing industrial landscapes through engineering innovation.

Comprehensive Analysis Conclusion: The Industry Enters a Critical Phase of "Climbing Over Hurdles," Ecosystem Competition Begins

This week's dense industry activities outline the new stage characteristics of solid-state battery development:

1. Mass Production Capability Becomes the New Focus: Whether it's Tesla's process breakthrough or various product launches and vehicle installation plans, the core issue has shifted from "whether it can be done" to "whether it can be stably and cost-effectively produced in large quantities." Engineering, yield, and cost control capabilities have become key metrics for distinguishing corporate competitiveness.

2. Scenario-Driven "Pioneer Markets" Are Forming: High-end electric motorcycles, special vehicles (food delivery), automotive start-stop systems, and consumer electronics, which have extreme requirements for performance, safety, or lifespan, will become the pioneer markets for the initial commercialization and "blood-making" function of solid-state/semi-solid-state batteries. Success in these scenarios will accumulate data, experience, and reputation for the largest power battery market.

3. Supply Chain Competition Evolves into Ecosystem Competition: Relationships between enterprises are no longer simple supplier relationships but form interest communities through strategic cooperation (e.g., SEMCORP-Gotion) involving joint R&D, capacity collaboration, and market expansion. Future competition will be between different ecological alliances.

4. Deepening Global Competition Landscape: China and the US are aggressively innovating in manufacturing processes and system integration, while Japan has a solid foundation and steady pace in core materials. China, with its complete industrial chain, active market applications, and rapid engineering capabilities, shows unique advantages in industrialization speed, but still needs breakthroughs in the originality of upstream core materials.

SMM Solid-State Battery Zone:

https://new-energy.smm.cn/new_energy/151036

According to SMM forecasts, all-solid-state battery shipments will reach 13.5 GWh by 2028, while semi-solid-state battery shipments will reach 160 GWh. Global lithium-ion battery demand is projected to reach approximately 2,800 GWh by 2030, with the EV sector's lithium-ion battery demand showing a CAGR of around 11% from 2024 to 2030, ESS lithium-ion battery demand at a CAGR of about 27%, and consumer electronics lithium battery demand at a CAGR of roughly 10%. Global solid-state battery penetration is estimated at about 0.1% in 2025, with all-solid-state battery penetration expected to reach around 4% by 2030, and global solid-state battery penetration potentially approaching 10% by 2035.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!

![[CATL's Wu Kai: Sodium-ion mass production this year, lithium-air next]](https://imgqn.smm.cn/usercenter/MaxcL20251217171730.jpg)