SMM February 5 News,

Key Points: Although the price of iron phosphate recently rose by 500 yuan per metric ton, seemingly a positive development, a cost analysis reveals a harsh reality: 409 yuan of this increase was absorbed by rising raw material costs. Prices of both iron and phosphorus sources rose across the board, driven by tight sulfur supply, while ferrous sulphate supply tightened further due to production cuts in the titanium dioxide industry. Essentially, this round of price increases represents cost pass-through, with minimal actual profit improvement for enterprises, highlighting their passive position in the industry chain.

In industry parlance: The fruits of the price increase revolution were stolen by ferrous sulphate and others!

This short article addresses a single topic: where did the increase in the price of iron phosphate go? Recently, due to market factors, the price of iron phosphate increased. The delivery-to-factory price, tax included, rose from 11,100 yuan/mt at the end of December 2025 to 11,600 yuan/mt at the end of January 2026, an increase of 500 yuan/mt.

Iron Phosphate Price Situation: The Long-Awaited 500 Yuan!

Let’s examine: The price increased, but where did the money go for iron phosphate producers? Taking the ammonium process as an example, let’s look at the cost changes.

Let’s examine: The price increased, but where did the money go for iron phosphate producers? Taking the ammonium process as an example, let’s look at the cost changes.

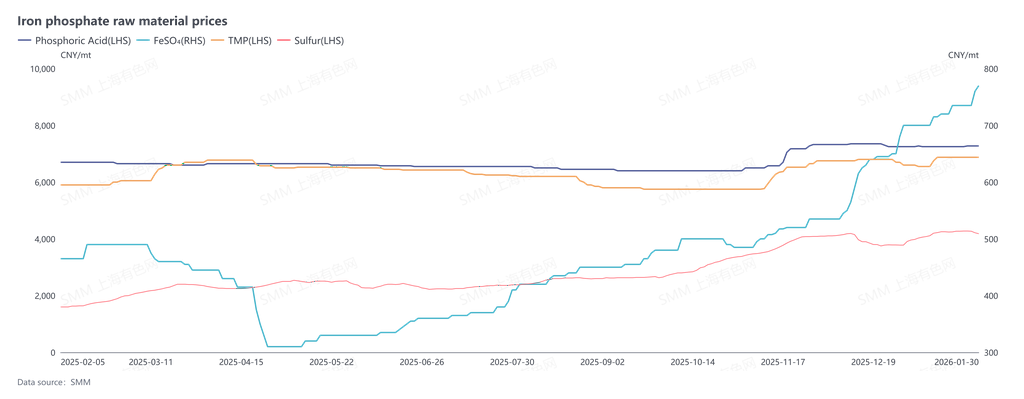

Changes in raw material prices: Costs increased by 409 yuan; the 500 yuan gained was quickly spent on raw materials.

A simple calculation of the per metric ton raw material prices and their impact on iron phosphate costs at two periods: end-December 2025 and end-January 2026.

A simple calculation of the per metric ton raw material prices and their impact on iron phosphate costs at two periods: end-December 2025 and end-January 2026.

Iron source: Ferrous sulphate increased from 650 yuan to 760 yuan, up 110 yuan, leading to a cost increase of 264 yuan.

Phosphorus source: Phosphoric acid rose from 7,250 yuan to 7,275 yuan, up 25 yuan; industrial-grade MAP increased from 6,700 yuan to 6,875 yuan, up 175 yuan. Combined cost increase: 145 yuan.

Overall cost of iron phosphate increased by 409 yuan per metric ton.

Where are the root causes?

One root cause of cost increase: Sulfur, from 3,780 yuan to 4,215 yuan, up 435 yuan. This affected processing costs for phosphorus sources and the cost of ferrous sulphate.

Another root cause: Ferrous sulphate. Rising sulfur prices drove up sulfuric acid prices, increasing processing costs in the titanium dioxide industry. Coupled with insufficient operating rates in the titanium dioxide sector, the production of by-product ferrous sulphate was impacted.

In 2026, the global sulfur market experienced tight supply. The core issue lies in continuously expanding demand, while supply growth from refineries significantly lagged behind demand growth, resulting in a persistent supply-demand gap.

This macro trend had a chain reaction on downstream industries. The phosphorus chemical industry primarily uses sulfuric acid to extract phosphorus resources from ore; rising sulfur prices increased the cost of processing each metric ton of phosphate ore.

As a by-product of titanium dioxide production, ferrous sulphate output was constrained by two main factors: First, weak end-use demand—the main consumption sector for titanium dioxide, the real estate industry, continued to decline, while exports weakened due to competition from new international capacity. Second, cost and process changes—high sulfur prices significantly increased costs for the traditional sulfuric acid process, prompting a shift in industry capacity structure toward the chloride process, which does not co-produce ferrous sulphate. Driven by these dual factors, overall titanium dioxide production declined, leading to a corresponding decrease in by-product ferrous sulphate output.

Conclusion: The profit distribution from the iron phosphate price increase was uneven; the major portion was eroded by simultaneous increases in upstream raw material costs, with only a small fraction translating into actual profit improvement for iron phosphate producers.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!

![Cobalt product prices mostly fell; refined cobalt dropped 16,500 yuan; the market still awaits downstream demand recovery [Weekly Observation]](https://imgqn.smm.cn/usercenter/wZUBk20251217171729.jpg)

![[SMM Analysis] Same race track, different racing styles: The distinct survival logics of leading NEV manufacturers](https://imgqn.smm.cn/usercenter/EPIrk20251217171726.jpg)