[SMM Steel Import and Export Special Topic] Outward Leap Under Domestic Demand Restructuring: A Panoramic Analysis of the Deep-Seated Logic Behind China's Steel Export Surge in 2025(Prat2)

- Capacity Spillover Along the Silk Road Reshapes Export Landscape

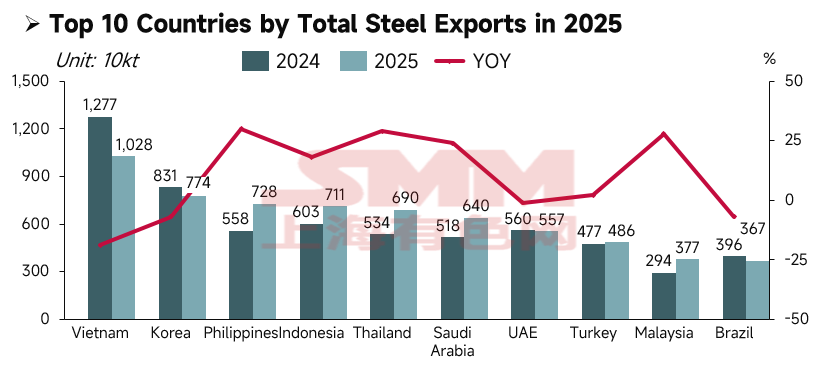

Among the top 10 countries by total steel exports from China in 2025, although exports to Vietnam declined, the volume still firmly held the top spot among export destinations. The reason for the decline is a familiar one—anti-dumping measures imposed by Vietnam on Chinese HRC in 2025. Notably, according to an SMM survey, Vietnam's anti-circumvention findings on wide steel coil from China are also expected to be finalized in February–March 2026, and the market currently views the likelihood of anti-circumvention implementation as high, with exporters already seeing a significant drop in orders. Therefore, it is reasonably predicted that subsequent HRC exports from China to Vietnam will decline sharply. However, considering Vietnam's domestic large-scale infrastructure projects, such as canals, hotels, and special economic zones, which still create rigid demand for construction rebar and wire rod, Vietnam is expected to remain one of China's major export destinations over the next 3–5 years. Similarly, other ASEAN countries such as the Philippines (7.28 million mt), Indonesia (7.11 million mt), and Thailand (6.9 million mt) are also in a phase of rapid urbanization. Due to the relatively high cost of steel production via electric furnaces in their local markets, these countries still rely on cost-effective ordinary steel from China. Particularly in the Philippines, where trade barriers are currently relatively low, it remains a major market for China's cold-rolled and galvanized steel exports in the short term, with total volume expected to have further upside potential.

Data Source: General Administration of Customs、SMM

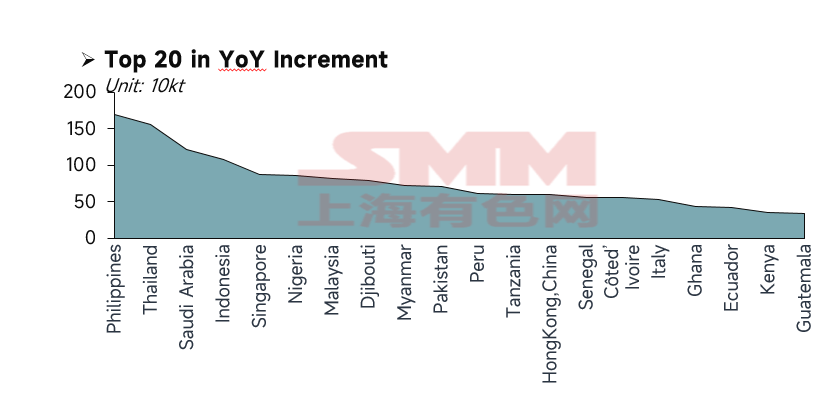

Looking back at the countries with the highest YoY increments and growth rates in China's exports from 2024 to 2025, emerging bright spots in the Middle East, such as Saudi Arabia, stand out. In the first three quarters of 2025, China's steel export value to Saudi Arabia surged by 41% YoY, the most significant growth rate among China's major export destination markets. This was driven by new city construction and energy transition projects under Saudi Arabia's "Vision 2030," which spurred substantial consumption of steel pipes and long products for infrastructure. Meanwhile, Africa and Latin America have become new blue oceans. In addition to the local construction reasons mentioned earlier, "reverse diversion" due to trade frictions also played a role. For example, impacts from the EU's Carbon Border Adjustment Mechanism (CBAM) and high US tariffs have forced Chinese steel to withdraw from high-barrier markets like North America and flow into these regions with relatively lower trade resistance.

Data Source: General Administration of Customs、SMM

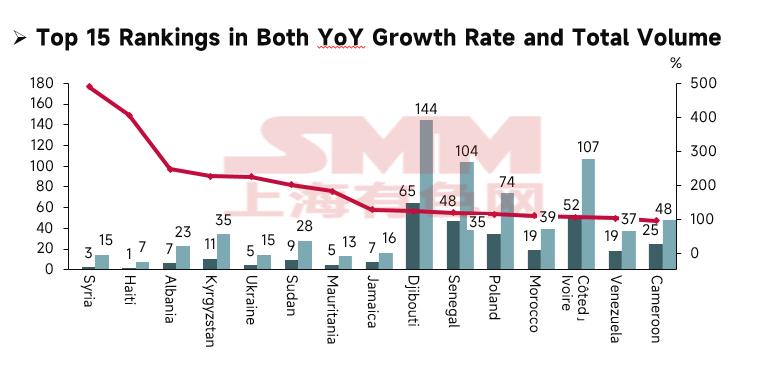

A background analysis of Djibouti and Senegal, which achieved high growth in both YoY growth rate and total volume, reveals that Djibouti serves as a "transit hub" for global trade and a gateway for infrastructure. Its growth primarily stems from its unique geographical location and strategic transformation as the "Gateway to East Africa." With recent changes in the Red Sea situation, Djibouti, as a critical node connecting Asia with Europe and Africa, has seen a surge in demand for port storage and transshipment facility construction. Senegal, on the other hand, is experiencing accelerated industrialization driven by energy discoveries. Its rapid growth is closely tied to large-scale oil and gas development and transportation infrastructure. 2024 was a pivotal year for Senegal to join the ranks of "oil and gas producers." Projects such as the Greater Tortue Ahmeyim gas field require large quantities of high-grade steel pipes, steel for drilling platforms, and storage facilities. Through this project, Senegal is moving towards a new stage of energy independence, consolidating its key role in the global energy transition.

Data Source: General Administration of Customs、SMM

- Dual-track Progress of "Quality Improvement" in Finished Products and "Volume Expansion" in Semi-finished Products

Data Source: General Administration of Customs、SMM

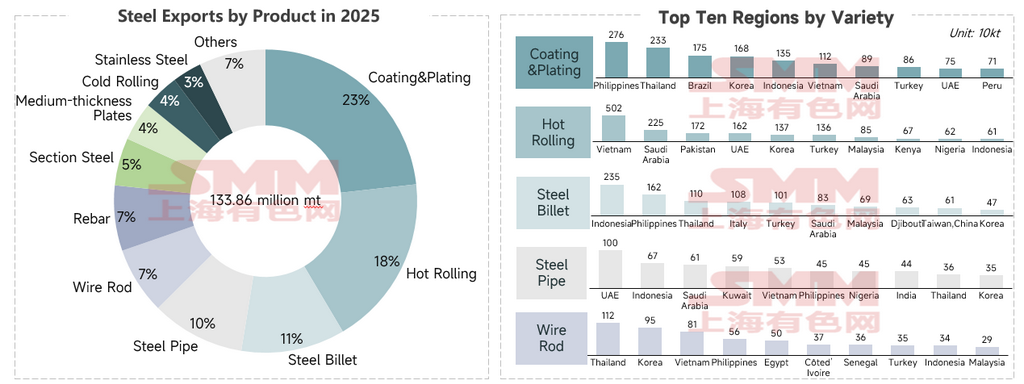

The breakdown of China's steel exports in 2025 reveals a core characteristic: extreme polarization among product categories, reflecting the dual impact of the global manufacturing center's shift and trade protection barriers.① The total export volume of coated and galvanized sheets exceeded 31.09 million mt, making it the largest single category in China's steel exports and an undeniable "ballast stone" in the export product landscape. Coated and galvanized sheets (such as galvanized sheets, color-coated sheets, etc.) are widely used in home appliances, solar panel mounting brackets, and light steel structure infrastructure, and China has developed strong industry chain completeness and scale-related cost advantages in this field. Southeast Asian countries, represented by the Philippines, heavily rely on coated and galvanized coils for their demand for roof sheets and light steel keels during urbanization. Additionally, due to their geographical location and climate, local buildings require extensive use of color-coated sheets and galvanized sheets with strong corrosion resistance and good sealing properties for roofs and wall materials to withstand strong winds and rain erosion. Moreover, these materials wear out quickly, leading not only to new construction demand but also substantial maintenance and replacement needs for existing stock.② HRC exports pulled back from 29.88 million mt in 2024 to 24.44 million mt in 2025. The year 2025 also marked the most severe period for Chinese HRC facing trade barriers. As the "primary target" of global anti-dumping investigations, policy tightening in key destinations like Vietnam and Turkey forced exporters to voluntarily reduce volumes or engage in re-exporting. In 2025 alone, HRC faced up to six anti-dumping investigations, and major export destinations such as Vietnam, Thailand, South Korea, and Brazil implemented relevant measures. Furthermore, the previous practice of exporting as alloy steel by "adding boron/chromium" was gradually blocked by multiple countries through "anti-circumvention investigations." SMM reasonably predicts that if HRC export volume is to be maintained in 2026, it will rely more on markets like Saudi Arabia, which have not initiated large-scale anti-dumping cases and have strong infrastructure demand, rather than the traditional ASEAN red ocean. ③ Steel pipes maintained steady growth, reaching 13.36 million mt, driven by oil and gas pipeline projects in the Middle East, such as Saudi Arabia and the UAE, as well as water conveyance projects in North Africa, which provided stable long-term contract orders for China's seamless and welded pipes. Regarding steel billets, relevant introductions have been provided earlier, and in-depth analysis of their core drivers will continue in upcoming features. Stay tuned to SMM Steel Industry Research...

Bonus at the end: The steel industry has its own ups and downs. SMM cordially invites you to participate in the "2026 Steel Export Varieties and Market Outlook Survey." Your feedback will serve as the core data source for our next in-depth report. Click the link below, and let’s work together to identify the most certain growth points in this "100-million-ton era"!

https://v.wjx.cn/vm/wEwxM3V.aspx

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[SMM Steel] 7.31 SMM Global Steel Daily Report](https://imgqn.smm.cn/usercenter/fvyjO20251217171715.jpg)