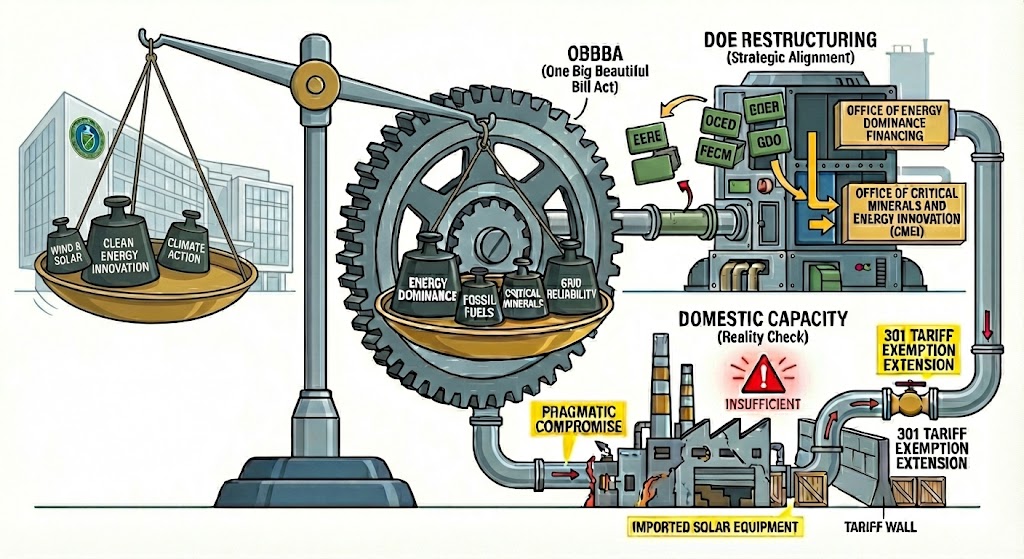

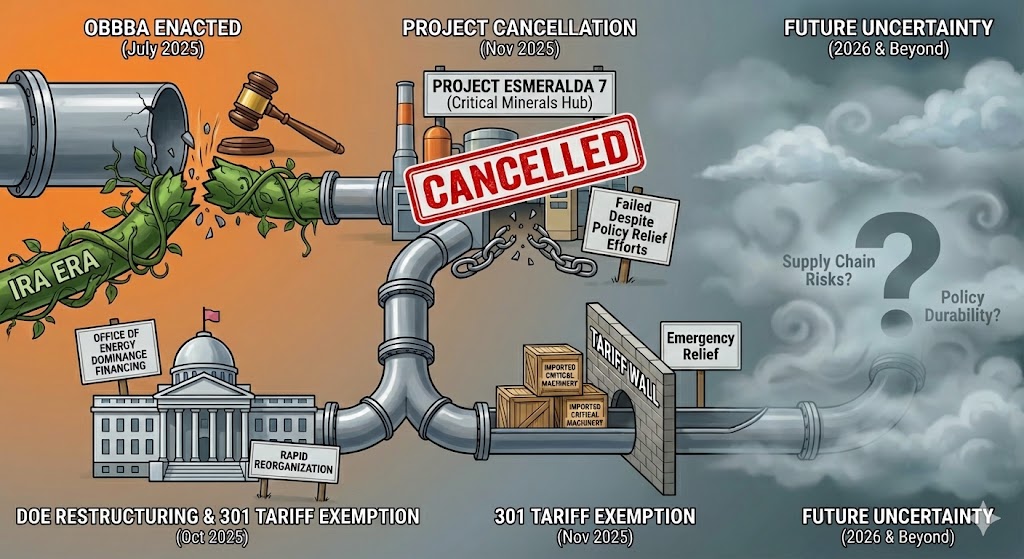

The enactment of the One Big Beautiful Bill Act (OBBBA) represents more than just a legislative update; it signifies a seismic shift in the underlying logic of U.S. energy policy. We are witnessing a definitive pivot from the Inflation Reduction Act (IRA) era, which emphasized emissions reduction above all else to a new doctrine of 'Energy Dominance'.

However, OBBBA is merely the 'operating system' for this new order. Its true impact is revealed through the coordinated actions that have followed its passage: the aggressive cancellation of renewable projects, the structural dismantling of the Department of Energy (DOE), and the pragmatic manipulation of trade tariffs. These elements form a 'strategic triad' designed to operationalize OBBBA's mandate.

1.0 The Strategic Driver: OBBBA as the New Constitution

Source: Internet

Source: Internet

At its core, OBBBA formally abandons the 'decarbonization-first' approach, enshrining 'energy dominance' as the nation's primary objective. This shift is codified in the amendment of Section 1706 of the DOE's Loan Guarantee Program and the aggressive sunsetting of renewable incentives. The act strips away previous requirements for greenhouse gas emission reductions, replacing them with criteria centered strictly on grid reliability, energy capacity, and supply security.

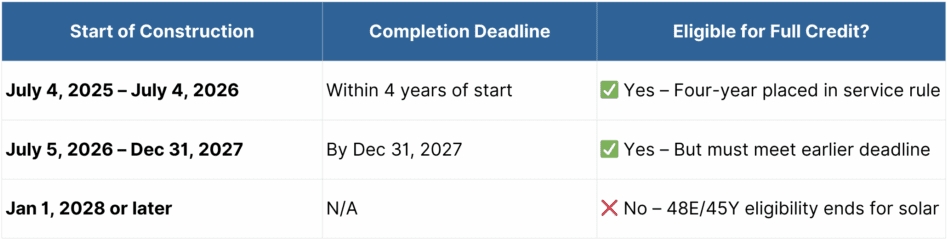

This pivot is operationalized through a rigid phase-out of solar tax credits. While projects starting construction before July 2026 retain standard timelines, those starting between July 5, 2026, and December 31, 2027, face a compressed deadline, requiring completion by the end of 2027 to qualify. Most critically, the act establishes a hard stop: projects starting construction on or after January 1, 2028, are completely ineligible for 48E/45Y credits. This redefinition drastically expands the playing field, making fossil fuel infrastructure upgrades and critical minerals processing the primary beneficiaries of federal support, while effectively placing an expiration date on solar investment. Simultaneously, through strengthened Foreign Entity of Concern (FEOC) restrictions, OBBBA mandates a decoupling from Chinese supply chains, establishing the legal framework for the executive actions that followed.

2.0 The Manifestation: Esmeralda 7 and the Anti-Solar Stance

The real-world consequences of OBBBA were felt almost immediately. In October 2025, the Trump administration cancelled the massive 6.2 GW Esmeralda 7 Solar Project in Nevada. While the official cancellation order cited farmland preservation, the decision stands as the first clear proof of concept for OBBBA's implementation. It aligns precisely with the directives of the newly formed 'National Energy Dominance Council', which prioritizes oil, gas, and coal projects. In this new strategic framework, fossil fuels are equated with 'low-cost, reliable energy'. By contrast, solar energy is increasingly categorized as unreliable due to its inherent intermittency. Consequently, its strategic status in the hierarchy of national energy deployment is being continuously downgraded. The Esmeralda 7 decision serves as a definitive signal of this new reality.

3.0 The Execution Engine: A Structural 'Lobotomy' of the DOE

To fully institutionalize OBBBA's agenda, the administration launched a radical restructuring of the Department of Energy (DOE) in November 2025. This was not a mere reorganization; it was a systematic dismantling of the 'Green State'.

Four major offices, which includes the Office of Energy Efficiency and Renewable Energy (EERE), the Office of Clean Energy Demonstrations (OCED), the Office of Fossil Energy and Carbon Management (FECM), and the Grid Deployment Office (GDO) were dissolved. These pillars of American innovation have been folded into a single, vaguely defined 'Critical Minerals and Energy Innovation Office' with no clear funding structure. Functionally, this restructuring reduces the DOE from a driver of innovation to a passive administrator. It is akin to merging a hospital, a CDC, and a healthcare authority into a simple pharmacy. The new entity retains only basic procurement capabilities, while the core public-interest functions such as long-term R&D, carbon management, and grid modernization have been hollowed out.

4.0 The Tactical Safety Valve: Section 301 Exemptions

Despite the ideological hostility toward renewables, OBBBA's implementers face a practical constraint: the surging electricity demand from AI and data centers requires immediate power capacity. This necessitates a pragmatic tactical adjustment. The U.S. Trade Representative's decision to extend Section 301 tariff exemptions for solar manufacturing equipment (such as silicon ingot furnaces and PECVD tools) until November 2026 is a direct response to this reality. It represents a 'bifurcated' protectionist strategy: maintaining tariffs on downstream modules (to block Chinese finished goods) while exempting upstream equipment (to allow U.S. factories to be built). This move acts as a 'safety valve'. It ensures that domestic manufacturing can scale up to meet OBBBA's grid reliability targets without triggering an immediate supply collapse, even as long-term support for solar technology is withdrawn.

All in all, these events are not isolated events. They are the integrated components of a strategy to reverse the energy transition. In the short term, we may witness a continued explosion in installation volumes as developers rush to maximize remaining incentives. However, this frenzy masks a deeper fragility. For the long-term trajectory of the solar industry, the outlook is shrouded in a dense fog of uncertainty. By dismantling the innovation engines within the DOE and downgrading solar's strategic status, the U.S. is creating a structural disadvantage. The message is clear: the era of federal partnership for green energy is over; the era of 'Energy Dominance' has begun.

Written by: Ryan Tey

![[Notice on Adjusting the Consumption Tax Policy on Some Batteries]](https://imgqn.smm.cn/usercenter/EaYRd20251217171743.jpg)

![[Solar: Germany’s rooftop PV auction remains undersubscribed]](https://imgqn.smm.cn/usercenter/jests20251217171741.jpg)

![[SMM PV Flash]](https://imgqn.smm.cn/usercenter/zMauQ20251217171742.jpg)