SMM reported on July 16:

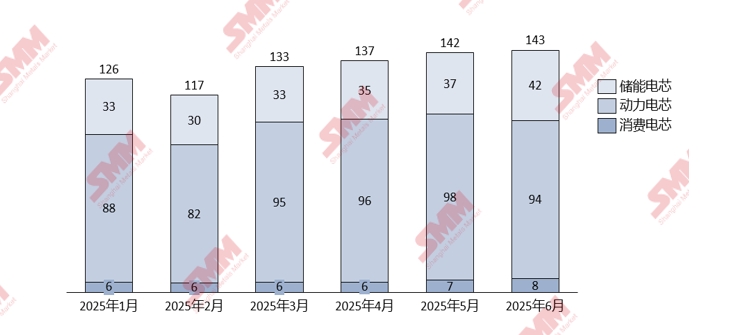

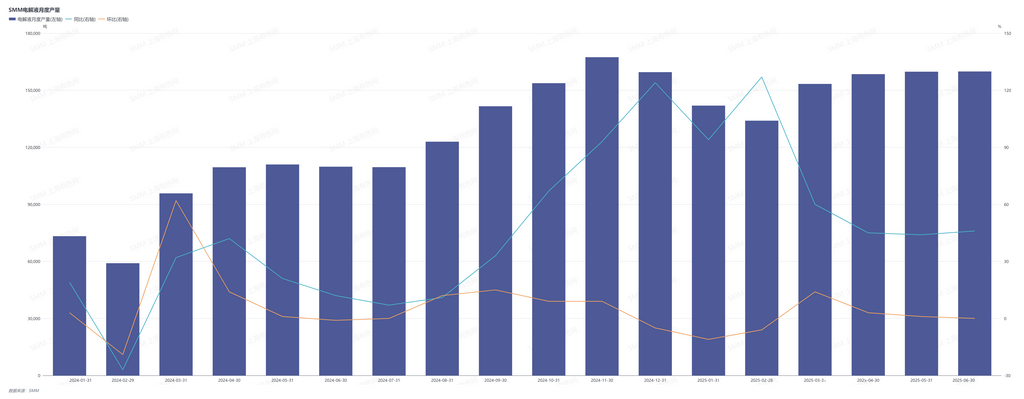

According to SMM statistics, over the past six months, the total production of electrolyte reached 907,480 mt, representing a 62.5% YoY increase compared to the 558,390 mt produced in H1 2024. In terms of production, the electrolyte market exhibits a high degree of correlation with the battery cell market. Looking at specific data, in January-February 2025, affected by the traditional consumption off-season during the Chinese New Year holiday, terminal demand for NEVs and ESS contracted, leading downstream battery cell enterprises to adjust their production schedules. This directly resulted in a decline in electrolyte orders and a simultaneous downward trend in production. After the holiday, as the terminal market gradually resumed operations, downstream demand showed signs of recovery and warming. In March, battery cell production increased by 14.3% MoM, and electrolyte, as a supporting material, also achieved a 14.4% MoM increase in production. However, after entering Q2, the market demand recovery did not meet expectations. From April to June, affected by the slowdown in the recovery pace of the terminal consumer market, battery cell enterprises' production schedules slowed down, and the MoM increase in production narrowed significantly. This change directly transmitted to the upstream electrolyte sector, causing electrolyte production to continue growing but at a significantly slower pace than in March, and the overall production activity of the industry decreased.

In terms of prices, the weak demand side has significantly suppressed cost transmission throughout the industry chain. Due to the slower-than-expected recovery in downstream demand, the electrolyte raw material market exhibited an oversupply situation, with prices of solvents, additives, and other raw materials continuing to decline to low levels. Meanwhile, the continuous downward trend in the price of lithium carbonate, a core raw material, further drove the accelerated pullback in the prices of key solutes such as LiPF6, significantly weakening the cost support for electrolyte production. Under the combined influence of multiple factors, the market price of electrolyte has been in a long-term low-level operation.

Chart- SMM's Monthly Production of Lithium Batteries in China from January to June 2025 (Unit: GWh)

Chart- SMM's Monthly Production of Electrolyte in China from January 2024 to June 2025

Overall, in H1 2025, the electrolyte market exhibited a "slow increase in volume, pressure on prices" operation trend. From the production perspective, after the Chinese New Year holiday, with the resumption of work and production by downstream battery cell enterprises, electrolyte production has shown a month-by-month recovery trend since March. However, due to the slower-than-expected recovery pace of terminal demand, the production increase was lower than the industry's initial expectations at the beginning of the year, remaining within a mild growth range.In terms of prices, the electrolyte market prices continued to be under pressure and decline in H1. The core driving factors came from the dual suppression of the cost side and the supply and demand side. On the cost side, the prices of core raw materials such as lithium carbonate and LiPF6 continued to decline due to overcapacity, and the prices of materials such as solvents and additives also fell due to weak demand, directly pulling down the production cost of electrolyte. On the supply and demand side, the industry's early expansion projects concentrated on releasing capacity, while the growth rate of downstream demand failed to match the increase in supply, resulting in an oversupply situation in the market and further exacerbating the downward pressure on prices.

Looking ahead to H2, although the growth in overseas ESS demand and the approaching peak season for end-use consumption will provide some support to market demand, leading to an increase in electrolyte production, the current issue of overcapacity in the electrolyte industry is prominent. The combination of existing and new capacity will make it difficult to reverse the redundant market supply situation in the short term, thus having a weak impact on boosting prices. Meanwhile, enterprises will continue to face intense market competition pressure. Top-tier enterprises, leveraging their scale effects and customer binding advantages, are expected to seize more market share through cost control. However, small and medium-sized enterprises may face further narrowing of their survival space under the dual pressures of price competition and insufficient capacity utilization rates. Against this backdrop, enterprises need to closely track fluctuations in raw material prices and changes in downstream demand, dynamically adjust production plans, and enhance operational flexibility and risk resistance capabilities to cope with the complex and ever-changing market environment.

Note: If there are any supplements or corrections to the details mentioned in this article, please feel free to contact us at any time. The contact information is as follows:

Tel: 021-20707858, Hu Xuejie. Thank you!

SMM New Energy Research Team

Wang Cong, Tel: 021-51666838

Ma Rui, Tel: 021-51595780

Feng Disheng, Tel: 021-51666714

Lv Yanlin, Tel: 021-20707875

Zhang Haohan, Tel: 021-51666752

Zhou Zhicheng, Tel: 021-51666711

Wang Zihan, Tel: 021-51666914

Wang Jie, Tel: 021-51595902

Xu Yang, Tel: 021-51666760

Xu Mengqi, Tel: 021-20707868

Hu Xuejie, Tel: 021-20707858

![[Lithium Battery: Brunp Recycling Wins 2026 European Inventor Award]](https://imgqn.smm.cn/usercenter/EPIrk20251217171726.jpg)

![[Lithium Battery: Tinci Materials Shifts 400 Million Yuan In Fundraising To Electrolyte Project]](https://imgqn.smm.cn/usercenter/Bwmed20251217171726.jpg)